Recent Search

Popular Searches

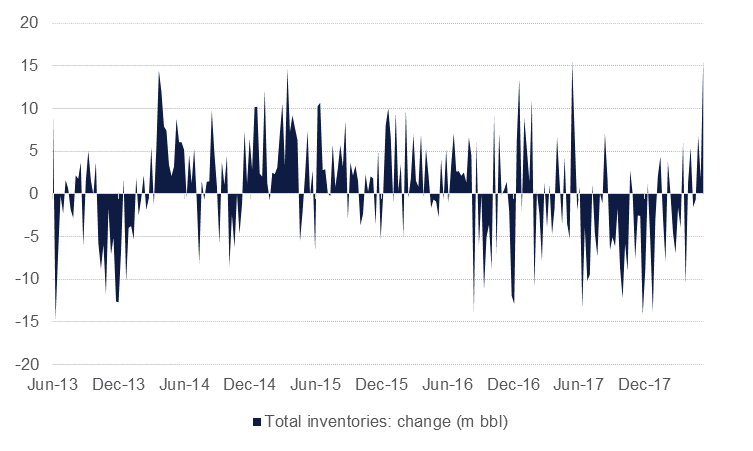

Oil data out of the US was near uniformly bearish with sizeable builds in crude stocks and products. Total commercial inventories have been quietly trending upward since the start of the year while stocks at Cushing have held relatively steady. Total petroleum product stocks rose by more than 15m bbl last week, the largest increase in 10 years. US production hit a new record high of 10.8m b/d last week, up 31k b/d w/w. Production was up 1.48m b/d year on year and has averaged growth of 1.23m b/d so far this year.

Source: EIKON, Emirates NBD Research

Source: EIKON, Emirates NBD Research

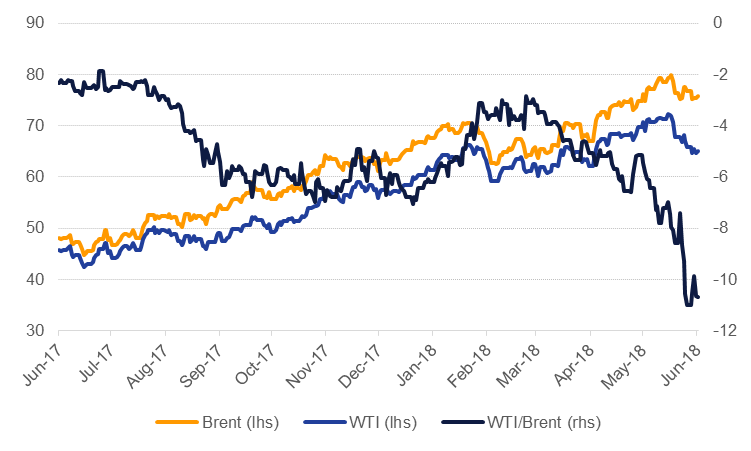

The bearish EIA report helps to affirm our view that the WTI/Brent spread will stay wide. After some marginal compression earlier this week in relation to an apparent request from the US for OPEC to increase production, the cross-Atlantic spread remains below USD 10/b. WTI at Houston, which has access to seaborne markets, is at a premium of more than USD 7.7/b for the front month to NYMEX. The longer Houston prices remain elevated we would expect demand for pipeline usage to stay high and lead to further discounts at Midland and other producing centres (WTI Midland closed yesterday at USD 55.6/b).

Source: EIKON, Emirates NBD Research

Source: EIKON, Emirates NBD Research