Recent Search

Popular Searches

Oil markets have managed to escape the clutches of the bear market they were stuck in from late May until the end of July, in part helped by news that OPEC countries would hold an informal meeting on the sides of an energy event in Algeria in September. The prospect of OPEC cutting output or reintroducing the freeze seems to have captivated markets but we doubt that an agreement will be achieved at the event. Since these proposals were last floated, more OPEC members have seen production disrupted, most notably Nigeria, and we think it is highly unlikely that any member will voluntarily limit production.

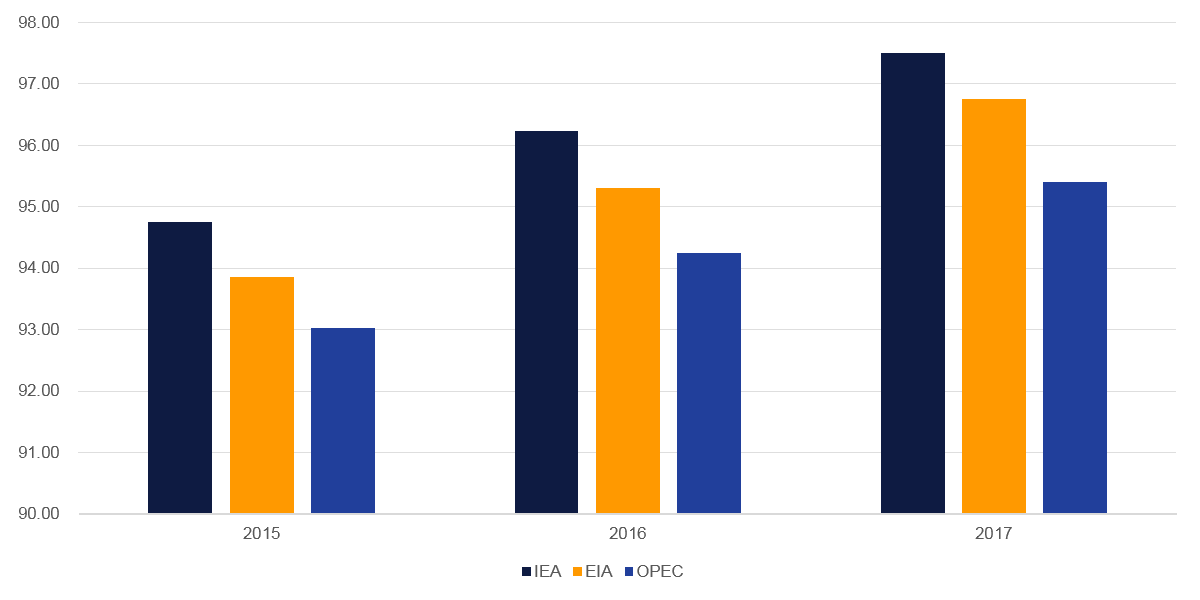

While it doesn't quite capture the headlines as much as surging output from major producers like Saudi Arabia (which self-reported a blistering 10.67m b/d of output in July), we think that the outlook for demand will be keeping oil ministers a little uncomfortable in their seats in Algiers. Since the oil price began its current slump the market's attention has been on how quickly supply can be cut to help alleviate the downward pressure on prices. A bump in demand in relation to low was taken as a given and indeed oil consumption did rise at its fastest pace in 2015 (1.86m b/d according to the IEA) since the post financial crisis recovery in 2010.

However, that low price-high demand effect has shown signs of waning and with prices expected to continue their upward grind into 2017 (we forecast Brent at an average of USD 55/b next year, some ways between market consensus and the current forward strip) consumers may begin to reevaluate how much marginal oil they need.