Recent Search

Popular Searches

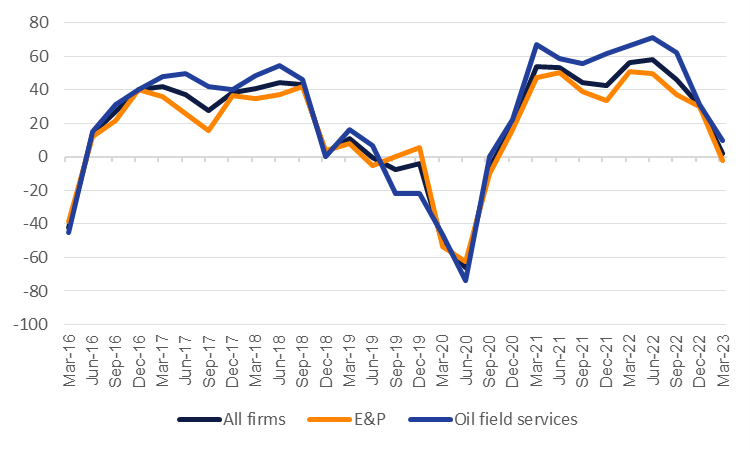

The Dallas Fed survey of energy firms showed a substantial deterioration in activity in the first quarter of 2023 as firms held back on increasing output and spending. The overall business activity index fell to 2.1 in Q1 2023, down from almost 30 in the final three months of 2022 and representing the slowest activity since Q3 2020 during the height of the Covid-19 pandemic. The weak activity was spread across both exploration & production (upstream) firms as well as oil field services companies. For both sectors the outlook component of the survey slumped heavily into negative while uncertainty indicators also ticked higher.

Source: Dallas Fed, Emirates NBD Research

Source: Dallas Fed, Emirates NBD Research

The quarterly survey also gives an indication how firms operating in the sector expect prices to develop over the rest of the year. The average price for WTI at the end the of 2023 was pinned at USD 79.64/b, lower than the previous survey’s estimate of USD 86.33/b, but still about USD 10/b higher than where prices were when the survey was carried out. That would suggest that the slump in mid-March in oil futures is set to be unwound and prices will recover toward the end of the year.

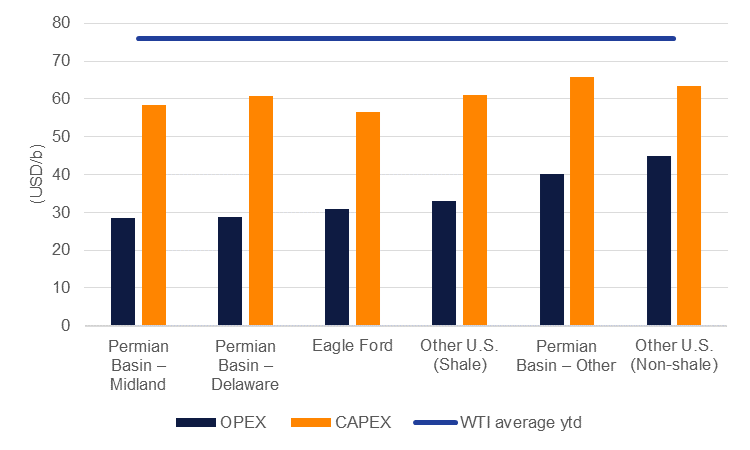

WTI futures have recovered from recent lows, trading closer to USD 73/b in recent days after having slumped to as low as USD 64/b in the wake of the stress in financial markets. At these levels, prices provide for E&P firms to comfortably cover opex costs at existing wells according to the survey, with average costs at specific fields ranging from USD 29/b to USD 45/b and a sample average of USD 37/b. Capex costs are higher with an average of USD 62/b, with some fields having capex costs close to where prices recently hit their bottom. With only about USD 10/b of headroom from spot WTI futures and capex costs, firms seem to be reluctant to substantially increase investment. Most firms cited cost inflation as the biggest challenge for profitability this year and with an essentially flat year/year outlook for prices—WTI ended 2022 at USD 80.26/b—the scope for substantial output increases from the US this year remains low.

Source: Dallas Fed, Bloomberg, Emirates NBD Research.

Source: Dallas Fed, Bloomberg, Emirates NBD Research.

Edward Bell

Edward Bell