Recent Search

Popular Searches

.jpg?la=en&h=600&w=800&hash=EDC56B9A24609FD2EC604BDCE0FB5556)

Source: Bloomberg, Emirates NBD Research

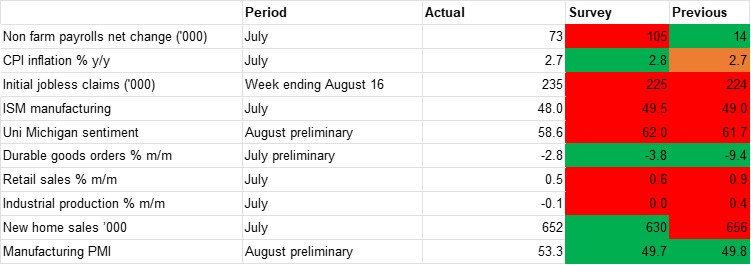

Source: Bloomberg, Emirates NBD ResearchThere has been a deterioration in the data going into our US macro scorecard over the past month, with most indicators flashing red – signalling not only that the data has worsened on the previous month but that they also came in weaker than analysts had anticipated. It is in this environment that Fed Chair Jerome Powell made his address at the annual Jackson Hole symposium last week, where he adopted a more dovish tone than he had previously, and than had been anticipated by markets. Powell spoke of a ‘shifting balance of risks’ which ‘may warrant adjusting our policy stance’, suggesting that the recent weak jobs report for July might be taking precedence for now over inflationary concerns.

The NFP report saw a net gain of just 73,000 jobs in July, far short of the predicted 105,000. Even more notable was the downgrade for the previous two months, with May-July averaging just 35,000 monthly jobs gains now, the worst period for job creation since 2020 when national lockdowns were implemented amidst the Covid-19 pandemic. The latest weekly initial jobless claims report also points towards greater labour market weakness as there were 255,000 claims in the week to August 16, up from 224,000 the previous month, while continuing claims continue to tick up. This is being reflected in sentiment, with the Conference Board consumer confidence index for July seeing a notable deterioration in views on the labour market.

If Powell’s speech is representative of wider FOMC members’ thinking then it would mark a shift from the previous July meeting, with the subsequent minutes showing that a majority of policy makers ‘judged the upside risk to inflation as the greater of these two risks.’ However, while the Fed’s focus may be more squarely on the labour market for the time being, that is not to say that inflationary concerns have been put to rest, and Powell noted that the risks there remain ‘tilted to the upside.’ CPI inflation remained at 2.7% y/y in July, unchanged from the June print and marginally lower than the predicted 2.8%. The round of tariffs implemented in August is yet to feed through to the data, however, which will likely exert some upwards pressure in the coming months. With this in mind, while we expect that the Fed will resume its rate-cutting at the upcoming September meeting, we expect that this will be a 25bps move lower, with the balance of risks precluding an outsize move.

Production data over the past month has been somewhat mixed. The ISM manufacturing survey remained in contractionary territory at 48.0, down from 49.0 the previous month, but there was a sizeable rebound in the S&P Global manufacturing PMI survey for August. It picked up to 53.3, compared with 49.8 in July and beating the predicted 49.7. This was the fastest pace of expansion in the index since May 2022, with business reporting high demand. In this growth environment, firms are managing to pass on higher tariff costs to consumers with the prices charged subcomponent at the highest in three years, another potentially inflationary signal.

Daniel Richards

Daniel Richards