Recent Search

Popular Searches

The US dollar is poised to hold its ground against peer currencies as we anticipate that the Federal Reserve will be patient on when it begins to ease policy.

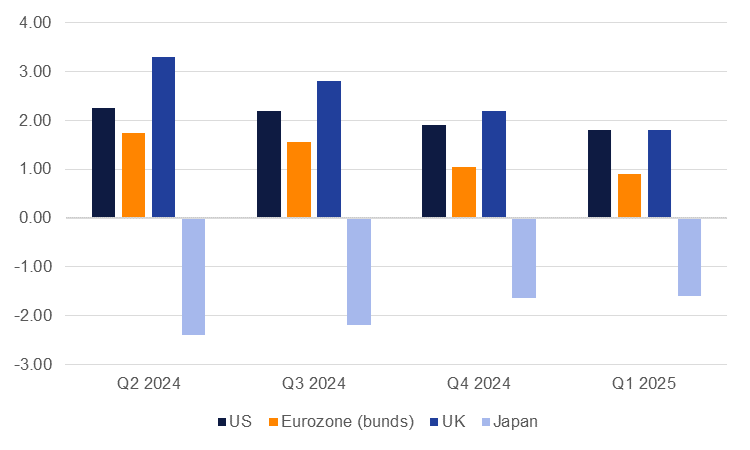

We recently revised our expectation on US rates, with cuts starting in September (from June previously) and now expect only two cuts this year (from three previously). The performance of the US economy—whether looking at the labour market, activity data or inflation—does not look as though it is screaming out for interest rate relief and policymakers have all but committed to delays in cutting rates. Fed chair Jerome Powell said in mid-April that the Fed wasn’t getting “greater confidence” on data moving in the right direction and that it would be “appropriate to allow restrictive policy further time to work.” That still sounds like a Fed preferring to err on the side of hawkishness and run policy tight even if it does cool the economy (which is the point of a restrictive policy stance in the first place).

By contrast the European Central Bank seems poised to cut as early as June. After the April meeting of the governing council ECB policymakers look as though they are lining up firmly behind a cut in less than two months’ time. ECB president Christine Lagarde described inflation in the Eurozone as undergoing a “disinflationary process” and that the regional economy was “heading towards a moment where we have to moderate the restrictive monetary policy” currently in place. Inflation in the Eurozone is maintaining a downward trend, falling from a peak of 10.6% y/y in October 2022 to 2.4% as of the March 2024 print. At the same time regional activity data is much weaker than in the US: the regional services PMI for the Eurozone has been holding close to the neutral level or dipping below it since Q3 last year while the ISM services index in the US has been more stable and positive.

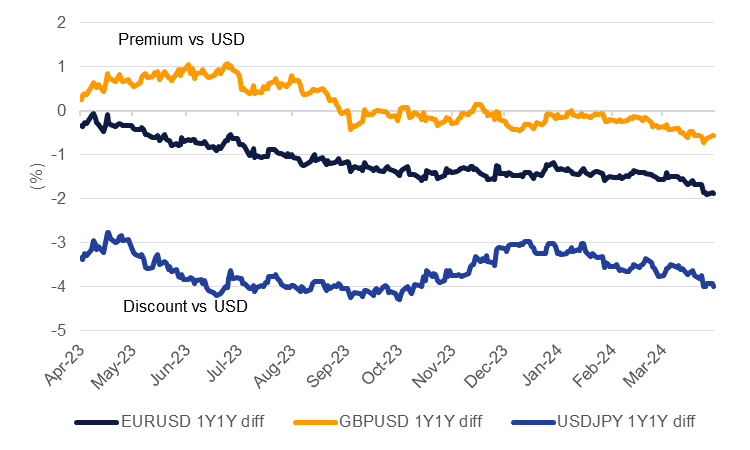

All other variables being equal, a softer economic performance and more accommodative central bank should mean a weaker currency and in 2024 that has been the case for the Euro. EURUSD is down more than 3% so far this year. We now expect that EURUSD will remain close to current levels until the end of Q3 and then only nudge modestly higher over the rest of the year. Real yield differentials, even as inflation has slowed more materially in the Eurozone, will still favour US dollar bonds over equivalent Eurozone bonds.

Source: Bloomberg, Emirates NBD Research. Note: consensus forecasts.

Source: Bloomberg, Emirates NBD Research. Note: consensus forecasts.

In the UK the inflation picture is somewhat in between the US and the Eurozone. The most recent print for March showed headline inflation cooling to 3.2% y/y but service prices are still hot at more than 6% and wage costs also aren’t showing a material sign of easing. But in 2024, activity indicators have been fairly robust for the UK economy—the services PMI has been above 53 for the first three months of the year—while monthly GDP prints have so far held positive.

The Bank of England has so far skewed neutral in its policy stance but comments from governor Andrew Bailey this week suggests the BoE is leaning toward easing later this year, saying of disinflation that he saw “strong evidence now that the process is working its way through”. Somewhat like the US, yields will favour the UK over the Eurozone so we see comparatively more room for GBPUSD to improve later this year than EURUSD.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

The Japanese yen has been the standout laggard among major currencies in 2024. USDJPY has soared to more than 154 for the first time since 1990 as markets price in a major divergence in policy between the US and Japanese central banks. The Bank of Japan is now finally tightening policy for the first time since 2007, moving away from negative interest rates at its March meeting, but the gap between US and Japanese rates remains substantial. Recent comments from Japanese financial officials that the G7 wants to avoid volatility in exchange rates has helped the yen to pull back some of its recent losses while the anticipation of intervention from the Bank of Japan or ministry of finance could also forestall substantial depreciation from here.

Nevertheless, the yen has a long climb back against peer currencies even if it is the most undervalued on an effective exchange rate basis at the moment. We expect it will be able to strengthen against the US dollar eventually, with USDJPY moving to 140 by the end of the year.

In general we now see space for the US dollar to maintain its current run of strength supported not just by positive economic fundamentals but a haven play as well as investors face an uncertain macroeconomic backdrop, a fraught global geopolitical environment and the prospect of a tight US election later this year. If there are benign outcomes in any of those themes then investors may move toward other currencies over the US dollar as a risk-on play. But for now, caution and economics favour the greenback.

| Last | Q2 24 | Q3 24 | Q4 24 | Q1 25 | Q2 25 | Q3 25 | Q4 25 | |

|---|---|---|---|---|---|---|---|---|

| EUR / USD | 1.0679 | 1.05 | 1.05 | 1.07 | 1.10 | 1.10 | 1.12 | 1.15 |

| USD / JPY | 154.27 | 150.00 | 145.00 | 140.00 | 135.00 | 130.00 | 120.00 | 120.00 |

| USD / CHF | 0.9098 | 0.91 | 0.91 | 0.90 | 0.90 | 0.88 | 0.86 | 0.85 |

| GBP / USD | 1.2467 | 1.25 | 1.26 | 1.28 | 1.30 | 1.31 | 1.33 | 1.34 |

| AUD / USD | 0.6450 | 0.64 | 0.65 | 0.67 | 0.70 | 070 | 0.73 | 0.75 |

| NZD / USD | 0.5924 | 0.60 | 0.62 | 0.62 | 0.65 | 0.68 | 0.68 | 0.68 |

| USD/ CAD | 1.3753 | 1.37 | 1.35 | 1.35 | 1.32 | 1.32 | 1.30 | 1.29 |

Edward Bell

Edward Bell