Recent Search

Popular Searches

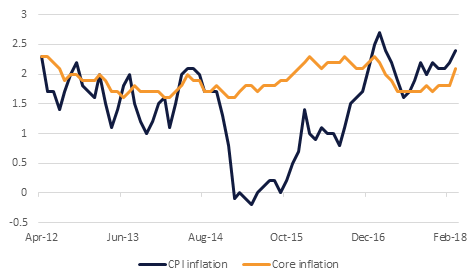

US inflation data was in line with expectations in March, with core inflation rising 2.1% y/y and headline CPI by 2.4%. This compared to 1.8% and 2.2% in February. The boost came in part from weaker mobile phone tariffs which had dampened price growth for the previous 12 months dropping out of the base, but a range of sectors including healthcare, shelter, car insurance and airfares also contributed. Minutes from the March FOMC meeting were released last night, showing that while a number of officials thought that the positive data coming out of the US implied that ‘the appropriate path for the Federal Reserve Funds Rate would be steeper than they had expected’, the consensus remained that risks were fairly evenly balanced. There was a discussion over at some point changing the language of the board to acknowledge that policy ‘would gradually move from an accommodative stance to being a neutral or restraining factor for economic activity.’

UK production data for February was significantly weaker than anticipated, with manufacturing production falling m/m for the first time in 11 months. Factory output contracted 0.2% compared to expectations of 0.2% growth. Industrial production fared little better, expanding 0.1% m/m, compared to expectations of 0.4%. With consumer activity likely to have taken a hit from the adverse weather conditions seen in the UK in March, the poor production data does not bode well for Q1 GDP growth figures, and could even bring into question the assumption that the Bank of England will enact another rate hike at its May meeting. The construction sector also fared poorly, contracting 1.6% m/m, and this will also have been hit by poor weather in March.

Egypt’s cabinet has given the go-ahead for launching a sovereign wealth fund with an initial EGP5bn. The government will also enter into talks with the World Bank over a support deal worth USD500mn, which will support government social aid programmes. Elsewhere in the region, Bahrain’s reserves have fallen to just USD1.6bn, marking a six-month low. The country has struggled to deal with the lower oil prices seen over the past several years.

Source: Emirates NBD Research

Source: Emirates NBD Research

US treasuries closed higher as a hawkish bias in the US Fed meeting was offset by increased geo-political tensions in the Middle East. Yields on the 2y UST closed unchanged while on 5y UST and 10y UST dropped by 1bp to 2.61% and 2 bps to 2.78%.

Regional bonds closed flat as investors look to re-price the existing ones following significant primary issues this week. Yields on the Bloomberg Barclays GCC Credit and High Yield index closed flat at 4.29% and credit spreads remained at 173 bps.

Damac raised USD 400mn from a 5y sukuk which was priced to yield 6.625%. Sharjah Islamic Bank raised USD 500mn from a 5y sukuk which was priced 150bps over mid-swaps. Qatar has set indicative price guidance for its proposed offering and may price later today.

The dollar remains near two week lows as investor concerns over a possible US strike in Syria weigh on sentiment. As we go to print, the Dollar Index is almost unmoved at 89.55, having closed below the 50 day moving average (89.84) for two consecutive days. While the index remains below this level there is a risk that we see further declines towards the 38.2% five year Fibonacci retracement of 88.42. Should this level be breached, a larger decline towards 85 is a medium term risk.

Developed market equities closed lower as geo-political tensions over Syria rose. Investors’ also exercised caution over the hawkish tilt reflected in minutes of the last Fed meeting. Both the S&P 500 index and the Euro Stoxx 600 index dropped -0.6% each.

Regional markets closed mixed with the DFM index adding +1.4% and the Tadawul losing -1.9%. Saudi equities had their worst single-day decline since November 2017 as rhetoric over Syria weighed on investor sentiment. Elsewhere, the EGX 30 index added a further +1.4% following reports of possible merger talks between Medinet Nasr Housing and SODIC.

Oil markets continue to remain on the boil as anxiety over a US intervention into Syria adds geopolitical premia to the market. Brent closed up 1.4%, above USD 72/b, and WTI has now broken above USD 67/b after a 2% gain yesterday. Saudi Arabia’s military also shot down a missile apparently targeting Riyadh which has kept oil bid. Time spreads at the front of both WTI and Brent curves widened thanks to the gains in front month pricing.

The EIA data was uniformly bearish. Crude inventories rose 3.3m bbl, including a 1.1m bbl build at Cushing, while imports were up and product supplied (a proxy for demand) fell. US crude production rose 65k b/d to over 10.5m b/d and is now 740k b/d since the start of 2018 and nearly 1.3m b/d higher than it was at the same time last year.

Aluminium prices have continued to rise as the metals market digests the impact of US sanctions on Rusal, one of the world’s largest producers. LME 3mth forwards gained 2.2% overnight and are up more than 10% since the start of the week.

Daniel Richards

Daniel Richards