Recent Search

Popular Searches

The US-China trade dispute remained in focus at the start of the trading week as US President Donald Trump said negotiations with China would resume again soon. China’s vice premier, Liu He, who has been responsible for China’s side of trade negotiations said that the country was willing to work with the US so long as negotiations remained “calm.” The risk-off tone to markets adopted on Friday quickly reversed following Trump’s comments with equity markets gaining nearly across the board and safe-haven assets, such as US treasuries, losing ground. While the comments are positive, the pace with which the US president apparently alters his view on trade negotiations contributes to highly volatile markets and trade talks have begun optimistically several times in the past only to later unwind significantly.

Durable goods orders in the US for July surprised on the upside with core capital goods orders gaining 0.4% and overall durable goods (including aircraft and other transport vehicles) rising by 2.1%. However, shipments, which the government incorporates into its measures of GDP, actually fell by 0.7% in July suggesting that businesses are still hesitant on investment.

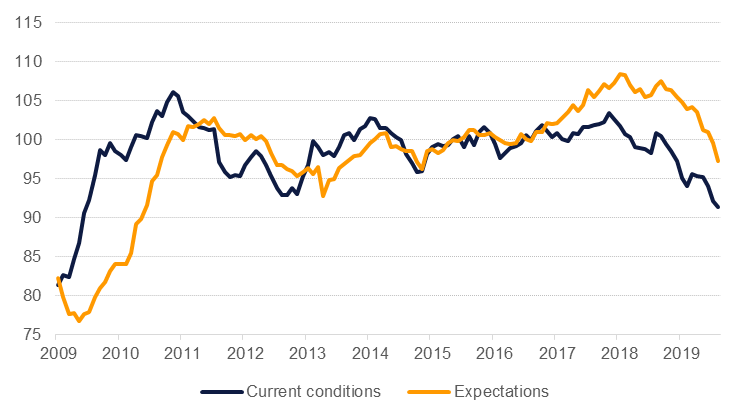

Germany’s IFO business climate index fell in August for a fifth month in a row, hitting 94.3 from 95.8 in July. The index hit its lowest level since November 2012 and is not far off levels last seen during the financial crisis. Germany’s economy appears set to enter recession in Q3 as manufacturing remains in the doldrums. Business expectations as measured by the IFO fell to 91.3 compared with 100.9 a year ago.

The Reserve Bank of India (RBI) decided at its board meeting to transfer c. USD 24.6bn of surplus funds to the government. The decision follows a recommendation from a panel set up by the central bank to make suggestions on its capital framework. The recommendations from the panel was unanimous and accepted by the RBI in full. The extra funds made available would make it easy for the government to provide fiscal stimulus to a slowing economy without breaching fiscal targets. Some of those steps are reportedly already in works and could be announced as early as this week.

Source: Emirates NBD Research

Source: Emirates NBD Research

Benchmark yields started the week higher as markets anticipated the restart of trade talks between the US and China following President Trump’s comments at the G7. Yields on 10yr USTs ended the day at 1.54%, up almost 2bps, while 2yr UST yields closed at 1.55%, keeping the spread slightly inverted. European benchmark yields also rose in the hope that a trade deal could be achieved.

It was a subdued day of trading for regional bonds owing to bank holiday in the UK. The YTW on Bloomberg Barclays GCC Credit and High Yield index remained flat at 3.15% while credit spreads hovered around 162 bps.

The dollar jumped as markets repositioned themselves for risk following US President Trump’s comments on the restart of trade talks with China. The DXY index rose 0.45% as the greenback gained against the Euro and sterling.

The RMB remains under pressure, trading above 7.15 against the dollar this morning despite the PBOC setting a stronger official rate.

Developed market equities closed higher amid hopes that the US and China are looking to dial back some of last week’s rhetoric over trade confrontation. The S&P 500 index and the Euro Stoxx 50 index added +1.1% and +0.4% respectively.

Most regional equities rebounded from yesterday’s losses. The DFM index and the Tadawul added +0.5% and +0.2% respectively. While there was no stock specific development, market heavyweights led the rally. Emaar Properties and Dubai Islamic Bank gained +1.0% and +0.6% respectively.

After showing some initial enthusiasm to the US president’s apparent shift in tone on trade, oil prices ended the day lower with both Brent and WTI falling by around 1%. Benchmarks are higher in early trade this morning. Commodity markets are likely waiting to see substantial headway made on trade progress before they can genuinely endorse Trump’s attitude toward trade.

The possibility of direct US-Iran negotitations is also likely to weigh on crude prices. Any sign that US sanctions on Iran would be eased and allow more crude out of the country would weigh on prices in a market that is already contending with too much supply in a slowing global economy. However, like the China talks, there is a high risk of markets getting ahead of themselves only to be disappointed by unchanging positions on either side.

Gold prices ended the day little changed despite opening significantly higher and then selling off sharply in response to Trump’s claim that China wants to restart trade talks. Gold is edging higher this morning at just shy of USD 1,530/troy oz.

Edward Bell

Edward Bell