Recent Search

Popular Searches

Speculation about the next Fed Chair intensified further last week with Stanford University economist, John Taylor, a perceived hawk, seeming to lead the race and Fed Reserve Governor, Jerome Powell not too far behind. It is not clear which of the two men would be chairman and which would be vice chair, a position that Trump also needs to appoint after Stanley Fischer stepped down earlier this week. Both positions are subject to Senate confirmation. Current Fed Chair Janet Yellen also remains in the running for renomination to a second four-year term. The decision is expected to be announced within the next two weeks.

The situation in Spain became tense as Prime Minister Mariano Rajoy announced intention to dismiss Catalan President Carles Puigdemont and his government, and take control of the regional police force and public television and radio channels as part of a barrage of measures that could be ratified by the Senate within a week. The decision brings the Catalan crisis to a new intensity, particularly as Puigdemont vowed to fight on even as prosecutors warned he could face up to 30 years in jail if he refuses to back down. While Rajoy has the law, most of the country and ultimately the army on his side, the Catalan separatists are counting on widespread support from regional officials and an extensive network of activists who have drawn up plans for guerrilla action against export companies and critical infrastructure.

Prime Minister Shinzo Abe’s ruling Liberal Democratic Party led coalition has won the snap election in Japan retaining its two-thirds majority. This in turn is expected to bring continuity to economic policies, including the massive monetary easing which has helped to bring six straight quarters of growth and low unemployment even as he’s struggled to defeat deflation and boost pay.

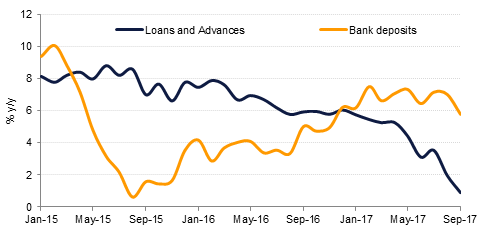

UAE bank deposits grew 0.9% m/m in September although the annual growth rate slowed to 5.8% from 7.0% y/y in August. Gross loans grew just 0.1% m/m and 0.9% y/y, the slowest annual rate of loan growth in the time series. As a result, the gross loan to deposit ratio declined to 99.0% from 99.8% in August. Broad money supply (M2) growth slowed to 4.7% y/y in September from 5.2% in August. M3 growth, which includes government deposits, grew 6.5% y/y last month.

Source: Haver Analytics, Emirates NBD Research

Source: Haver Analytics, Emirates NBD Research

Speculation about the next Fed Chair intensified further last week with John Taylor, a perceived hawk, seeming to lead the race. US Treasury curve steepened with yields on 2yr, 5yr, 10yr and 30yr all closing up at 1.58% (+4bps w/w), 2.02% (+7bps), 2.38% (+8bps) and 2.90% (+8bps) respectively. Still unsettled situation in Germany and on Catalonia front along with ongoing Brexit issues left sovereign yields in Europe following suit with the UST. Yields on 10yr Gilts and Bunds closed higher by 5bps to 1.33% and six bps to 0.45% respectively.

Despite stable oil prices CDS levels on GCC sovereigns had a slight widening bias. Credit protection costs increased by three bps each on Bahrain to 240 bps and Qatar to 102bps during the week. However, Dubai – the most diversified economy in the GCC region – was an exception with 5yr CDS spreads reducing by 8bps during the week to 120bps. In the GCC cash bond space, average yield on regional Barclays GCC bond index rose 2bps to 3.42% even as credit spreads tightened 4bps to 128bps.

EAPART 20s and EAPART21s were the worst performing bonds in the GCC universe, as their issuer, EA Partners was downgraded by Fitch to ‘CC’, barely two notches above default. Fitch cited concerns about liquidity pool being insufficient to offset lost contributions from Air Berlin and Alitalia, even if Etihad and other affiliates keep up payments. Yield on EAPART 20s closed 30bps wider at 13% with bond price falling to $85.3.

In the primary market, Bahrain’s Oil and Gas Holding raised $1 billion in 10yr notes at T+516.2bps which traded up by 2 points on its debut in the secondary market.

USD was the best performing G10 currency last week, the dollar index rising 0.61% after finding support near the 200 week moving average (93.009). This is now the fourth consecutive week that this key level has held as a firm support, an observation which strengthens our conviction that further gains lie ahead for USD in Q4 2017. While the index remains above the 200 day average, the risks are that there are further gains towards 94.20, above the 100 day moving average (94.15) and the 23.6% one year Fibonacci retracement (94.034). A break of this level is likely to result in further gains towards 96.00, levels last seen in July 2017.

Equity benchmarks advanced in most of the developed world last week. S&P 500 and Dow Jones gained support from solid result announcements and expectations of the tax cuts, closing up by 0.5% and 0.71% respectively. Across the pond, FTSE 100 closed unchanged while DAX gained 0.0%. Asia followed suit with the western world with Nikkei and Hag send up by 0.04% and 1.17% respectively.

Regional equity bourses generally fell on Sunday. Dubai index was down 0.8% with Emaar Properties leading the fall ahead of the IPO plans for its development business. Saudi stocks fell 0.5% lead by Jabal Omar and Qatar index was down -0.17% despite in line result announcements from corporates.

Oil prices were little changed over the week, holding in their range of USD 55/b-58/b for Brent and USD 50-52/b for WTI. The drilling rig count in the US fell last week with exploration and production companies cutting seven rigs despite the WTI 2018 calendar strip hanging close to USD 52/b. Tensions in Iraq continues to provide more of a floor under crude as well as there are reports of disruptions to exports to Ceyhan.