Recent Search

Popular Searches

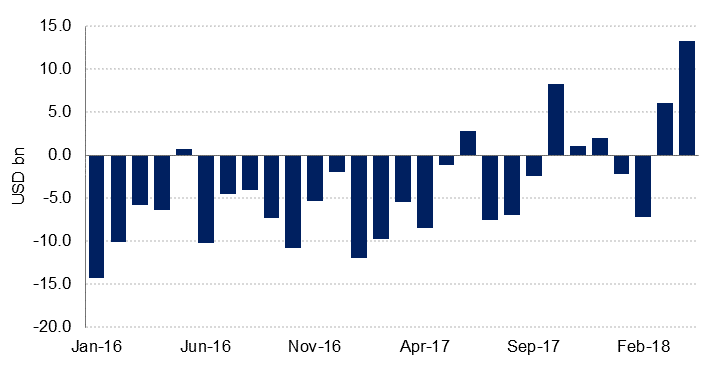

SAMA’s net foreign assets rose to USD 498.9bn in April, the highest level since March 2017. While the higher oil price likely contributed to an improved external balance, the USD 11bn bond issue in April was the main driver of the USD 13.3bn rise in the stock of foreign reserves last month. The apparent stabilisation in the level of NFAs in recent months is encouraging, and something we were hoping to see this year after the sharp drawdown since 2015.

Source: Haver Analytics, Emirates NBD Research

Source: Haver Analytics, Emirates NBD Research

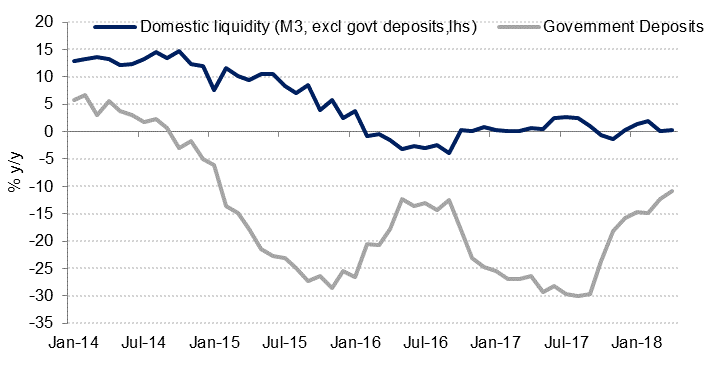

Broad money supply growth (M3) remains relatively weak at just 0.2% y/y in April, unchanged from March. Although M1 is growing at a faster rate than M3, quasi money (FX and longer term SAR deposits) continue to decline. Government deposits increased 2.4% m/m in April, the biggest monthly rise since October last year; on an annual basis government deposits fell -10.9% y/y. The rate of decline in government deposits has slowed significantly however.

Source: Haver Analytics, Emirates NBD Research

Source: Haver Analytics, Emirates NBD Research

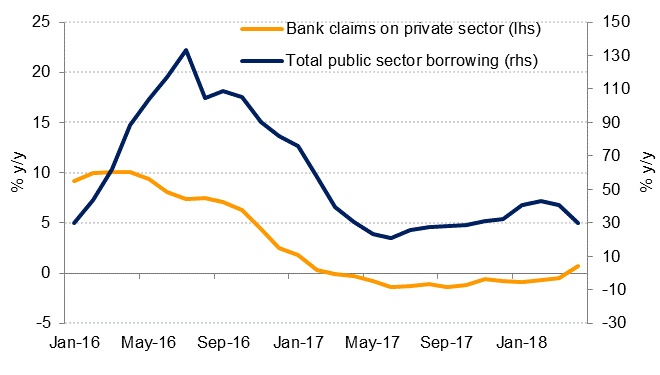

Private sector credit increased 1.5% m/m and 0.7% y/y in April, the first annual rise in lending to the private sector since February 2017. The m/m rise in private sector credit was the strongest in more than two years.

Meanwhile, public sector borrowing declined -0.1% m/m, the first contraction since June last year, while the annual growth in public sector credit slowed sharply to 29.8% y/y in April from 40.8% y/y in March. While this likely also reflects the shift to external debt issuance last month, higher oil revenues will also likely contribute to a smaller budget deficit and thus a lower borrowing requirement this year relative to 2017.

Source: Haver Analytics, Emirates NBD Research

Source: Haver Analytics, Emirates NBD Research

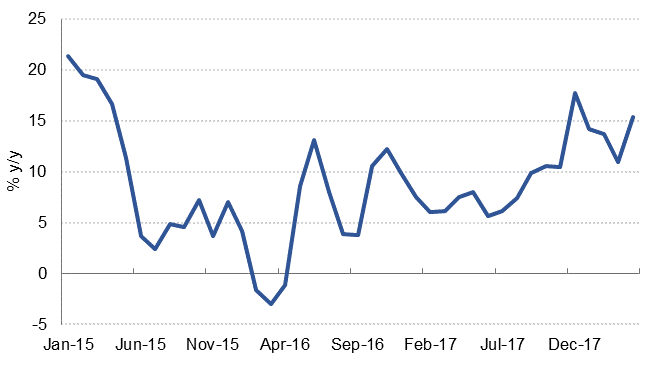

The value of point of sale transactions rose 17.8% y/y in April, and the 3m moving average shows an accelerating trend in this proxy indicator for retail sales. The number of point of sales transactions also shows strong growth and a rising trend.

Source: Haver Analytics, Emirates NBD Research

Source: Haver Analytics, Emirates NBD Research

Overall, the monetary survey and point of sales data for April are very encouraging. They reflect a more stable external balance on the back of higher oil prices and external debt issuance, as well as pointing to slower domestic borrowing by the government, as the budget deficit narrows. Private sector data is also positive, with credit growth recovering and point of sales data indicating increased consumption by households through April.