Recent Search

Popular Searches

Weekly EIA data was largely bearish as a trend of quietly rising inventories remains in place. Overall crude inventories remain close to their five-year average of around 425m bbl while Cushing stocks have turned upward sharply in recent weeks. Production continues to move higher, adding 65k b/d last week to take total output to over 10.52m b/d.

The EIA recently cut its projection for US crude oil production in 2018 to growth of 1.37m b/d from 1.38m b/d. So far in 2018 US crude has averaged 1.1m b/d higher than year ago levels, according to weekly EIA data, but the pace has been accelerating. We are now growing cautious about how close US producers will get to the EIA’s projections as logistical constraints may hamper production. Production growth has centred on the Permian basin in Texas where pipelines taking crude from the region to the Gulf coast are already close to capacity. Prices at Midland, in the Permian, have widened to as much as a USD 5/b discount to WTI as the crude remains effectively trapped inland. Taking crude by truck or rail is an option but there too constraints on availability may derail production plans.

Source: Eikon, Emirates NBD Research. Note: USD/b

Source: Eikon, Emirates NBD Research. Note: USD/b

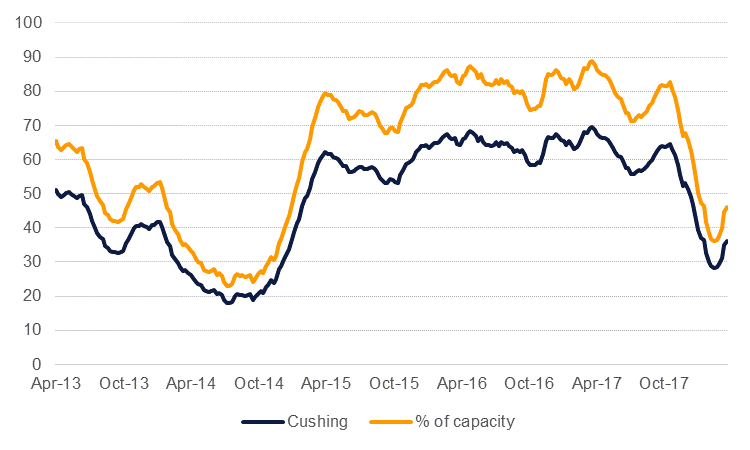

Pipeline expansions are expected by 2019 but until then the only means of egress for Texas producers may end up being Cushing. We would expect to see further builds in Cushing stocks over the year as few alternatives remain open to producers. Inventories at the pricing hub are currently low and at less 44% of capacity. We don’t expect they will have a significant bearing on WTI or the shape of the curve until spare capacity at the hub shrinks considerably from current levels.

Source: Eikon, Emirates NBD Research. Note: m bbl.

Source: Eikon, Emirates NBD Research. Note: m bbl.