Recent Search

Popular Searches

OPEC's production cut agreement has now been in force for a full three months, allowing for some perspective on whether it has indeed been effective in supporting the oil market. Judging from the price response, compliance with the cuts by OPEC and non-OPEC producers and the impact on inventories the cuts have helped to keep the market from falling further but have not yet prompted a major turnaround in prices. We expect OPEC will extend its production cuts for another six months but that an eventual return to supply growth will act as a further barrier to price rallies.

OPEC's announcement to cut production has helped to set a floor under crude prices but hasn't yet catalyzed a rally to levels that would help member nations' economies. A level of around USD 50/b for Brent futures appears to be the new floor of the market as prices have bounced off that marker when they did break lower in March. However, prices has so far struggled to rise significantly higher, hitting a high of USD 57/b early in January and have actually been trending lower for most of 2017 so far. In terms of sparking a rally in near-term prices, against which OPEC producers price their exports, the cuts have so far had a relatively muted impact.

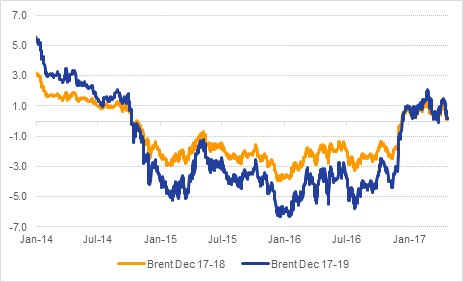

Where they have been more successful is in shifting the shape of the forward curve. When oil prices began their crash in mid-2014 futures flipped into a steep contango as burdensome inventories and a seemingly unending surplus weighed on markets. The contango structure incentivized storage plays, worsening the stockpiles numbers, and did little to weaken the ability of more nimble private producers, namely US shale producers, to hedge future production at commercial levels.

When OPEC announced its cuts the contango began a process of flattening and longer-dated time spreads have moved into what we would describe as a tentative backwardation. The size of the backwardation is still far smaller than where it was for much of the period prior to 2014 when spot prices were high and it has shown a tendency to move back to neutral or threaten to dip back into contango as the market reacts to upward revisions to production forecasts in the US. Indeed the front of the curve has so far resisted the urge to move into backwardation which to us would be more convincing evidence of a tightening market.

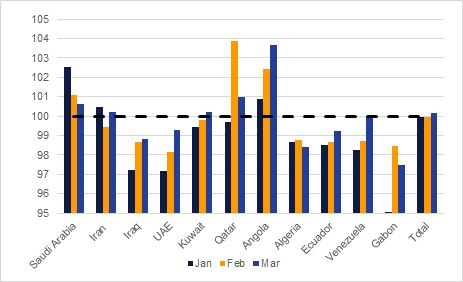

Compliance with the production cuts has so far been higher than the market likely anticipated with aggregate compliance among members liable for cuts averaging around 80% in the first quarter. Total output has fallen by more than 1m b/d since the end of 2016, not far off the 1.2m b/d cut that was set out by OPEC. This decline has been achieved even as both Nigeria and Libya have managed to arrest the decline in their output. In Libya's case, however, production fluctuates on a near weekly basis as militant groups take or lose control of oil infrastructure.

The production cuts have fallen heaviest on the GCC producers in OPEC as Saudi Arabia has 'overcut' and collective GCC output has fallen 980k b/d since the end of 2016. Saudi Arabia may be able to keep some of the steeper cuts in force and avoid a seasonal uptick in crude, fuel oil and diesel demand in summer months as the country has been making use of more natural gas in its power generation.

While overall production has fallen considerably from OPEC members, the decline in exports has been much more modest. Overall exports are down just 260k b/d up to March from the end of 2016 as major producers like Saudi Arabia have seen much smaller cuts to overseas shipments. Indeed, Saudi Arabia intends to keep shipments to overseas buyers intact and has been adjusting official selling prices downward to ensure it keeps markets share. Prices for exports to Asia have been cut for several months running for most grades of Saudi oil, bucking the general tightening trend they had seen for much of 2016.

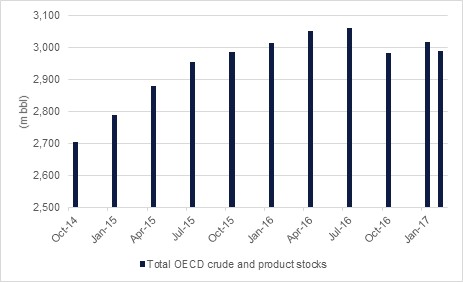

Clearing the excessive inventories that have built up in oil markets is, in our view, the priority for OPEC members as it would allow them to raise production and capture more market share without dampening prices. Inventory data so far this year has been mixed. Total developed market crude stocks have risen 62m bbl as of the end of February according to OPEC's estimation while product stocks have slipped. Overall, total hydrocarbon stockpiles in OECD nations have remained sticky at close to 3bn bbl. However, given the paucity of data on global inventories the market is subject to weekly changes in US data where inventories have pushed higher and have hit new record levels several times this year.

OPEC's decision to cut production but keep imports reasonably steady will grind against efforts to curb inventories, putting the onus to draw stocks down on demand and non-OPEC producers, both of which have proven to be fickle partners in the past.

Whether to extend the production cut will be the main question for OPEC ministers at its May meeting and this mixed performance in supporting the market suggests to us that an extension is likely. Saudi Arabia and Russia have been reportedly talking up the potential of an extension to cuts and if there is a unison voice on the issue from these two major producers then it is likely they will carry the motion to other producers. But another six months of restrained output opens up OPEC's key export markets to further encroaches from competitors: already in 2017 the US has emerged as a new supplier of crude oil to Chinese markets.

Edward Bell

Edward Bell