Recent Search

Popular Searches

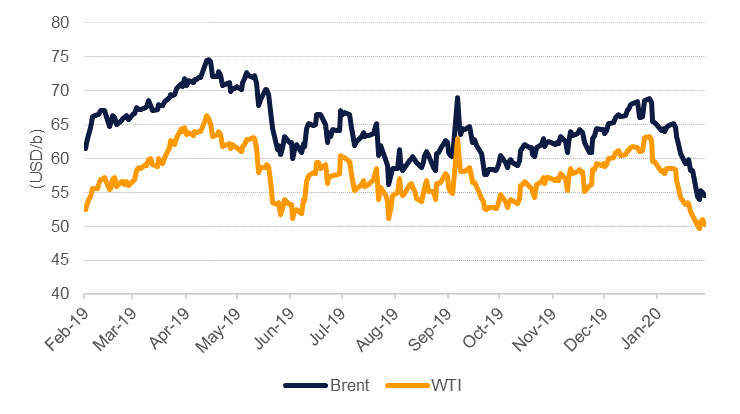

Oil markets moved back into bear territory last week as concern over how badly demand will be affected by the coronavirus outbreak widened. Brent futures settled the week at USD 54.47/b, down 6.3% over the five days and a fifth consecutive weekly decline. WTI fell 2.4% over the week to close at USD 50.32/b having moved below USD 50/b earlier in the week. Both contracts have fallen more than 20% from their 2020 highs and are hovering close to their lowest levels in the past year.

A technical committee for OPEC+ recommended a 600k b/d cut to current production targets as a way to offset the negative demand impact of the coronavirus. The proposal is non-binding and only OPEC+ ministers can actually agree on the cuts and choose how to allocate and enforce them. The overall impact of the cut proposal was muted as Russia gave only an acknowledgement and said they would notify the rest of the producers’ bloc soon if they agreed in principle for further cuts to output. With the scale of demand slowdown still an unknown variable, the Russian view may be to err on the side of caution and not risk cutting output should prices stabilize in the USD 50/b-USD 60/b over the coming weeks. The lack of clarity over OPEC’s position—including whether to also extend the current cuts—means that markets appear poised to take downside views on oil in the short term until there is greater conviction that OPEC producers are ready to endure substantial production cuts to support prices.

Markets will also be scanning reports out both from OPEC and the IEA later this week for further analysis on how badly China’s demand will be impaired this year. Neither forecasting agency had a particularly bullish conviction for oil in 2020 given already tepid demand expectations and a healthy supply picture from non-OPEC producers. A major downgrade to demand expectations may be apparent in either agencies’ report, helping to keep prices anchored around current levels. Meanwhile, a UN-led conference on Libya will work on restoring production to shore up the country’s economy. Political unrest in the North African producer means that as much as 700k b/d of output has been shut in, threatening a significant negative move if it is restored in short-order.

As one of the surest signs that OPEC’s messaging around cutting production hasn’t been effective, the Brent market closed in contango last week across the first five expiring contracts. Time spreads at the front of the curve closed at USD 0.33/b in contango compared with a backwardation of around USD 1/b a week earlier. Longer-dated time spreads also pushed deeper into contango structure with Dec spreads losing significant strength. Meanwhile, WTI entrenched its contango position with 1-2 month spreads closing at USD 0.23/b. Worryingly for regional producers, the Dubai curve also flipped into contango, with 1-3 month spreads closing at USD 0.36/b.

Investors accelerated their dumping of long positions in Brent and WTI last week. Net length in Brent fell by almost 50k contracts, the heaviest amount of net selling since October 2018 while WTI net length fell by 44k lots, down more than 100k over the last two weeks. Long positioning as a share of open interest in both benchmarks declined last week.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

Edward Bell

Edward Bell