OPEC+ announced on May 3 that it will increase output in June by 411k b/d, with the increase coming from those countries that have agreed to additional production curbs. The original OPEC+ plan for June announced in December last year was that output would increase by 140k b/d. This is the second consecutive month where OPEC+ is targeting larger than originally planned increases after an announcement earlier in April projected May output levels higher across the core OPEC+ producers.

Some of our initial takeaways from the recent OPEC+ developments:

OPEC+ gave itself the flexibility to adjust production targets to match market conditions when it outlined targets for 2025-26 in December last year. However, the language at that time was that “monthly increases can be paused or reversed subject to market conditions.” Projecting larger than expected increases marks a reversal in OPEC+ strategy.

OPEC+ has now returned to setting monthly production targets, at least for those eight members who had been providing additional production limitations. Providing month-ahead target announcements for producers controlling nearly 30% of global oil production will inject substantial short-term volatility to prices.

OPEC+ only controls part of the oil market narrative and has little influence on demand. Prior to the announcement of new elevated and widespread tariffs from US President Donald Trump, oil demand growth was set to be moderate in 2025.

Internal cohesion within OPEC+ is fraying. The larger than expected increase for June included a direction to “fully compensate for any overproduced volume since January 2024.” Based on the IEA’s estimates of OPEC+ production, Iraq, the UAE, Kuwait, Kazakhstan and Russia have consistently over-produced during that time.

Market reports imply that Saudi Arabia has threatened to unwind the full production restraint that OPEC+ is implementing by November 2025, ahead of incremental increases planned until the end of 2026.

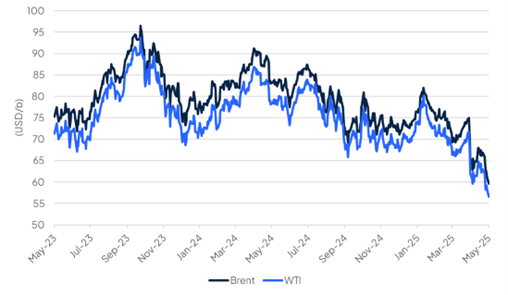

Oil markets continue their descent

Source: Bloomberg, Emirates NBD Research.

First order effects on market conditions:

Oil prices have taken another steep leg lower. Brent futures have now moved below USD 60/b while WTI is trading in the mid USD 50/b range.

The contango is shifting forward along the curves. At the end of April the Brent futures curve had been in backwardation out to the December contract and then was in contango until the end of 2026. Now that contango structure has shifted earlier to October while front-month backwardation has also narrowed.

Volatility has spiked. Downside protection costs have increased while overall volatility in Brent futures is at its highest level in the last two years though not quite at pandemic levels.

Impact on our market and regional forecasts:

We had been anticipating higher volumes from OPEC+ for some time. In September 2024 we wrote that “OPEC+ members are likely to doubt the effectiveness of restraining production if it means market share is eroded with no parallel support for prices.” Our regional GDP forecasts have growth in oil GDP and the upside risks to that view that we had highlighted look likely to materialize.

Our oil price outlook has long been built on higher production from OPEC+ and non-OPEC+ overwhelming demand growth this year. In April we revised our price outlook lower for 2025 with a target of an average of USD 65/b for Q4 2025. For now, we maintain that target though downside risks have increased substantially.

The prospect of a disorderly end to the Declaration of Cooperation (OPEC+) is increasing in probability. We had notedseveraltimes that this was a risk for oil markets that was being underpriced.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.