Recent Search

Popular Searches

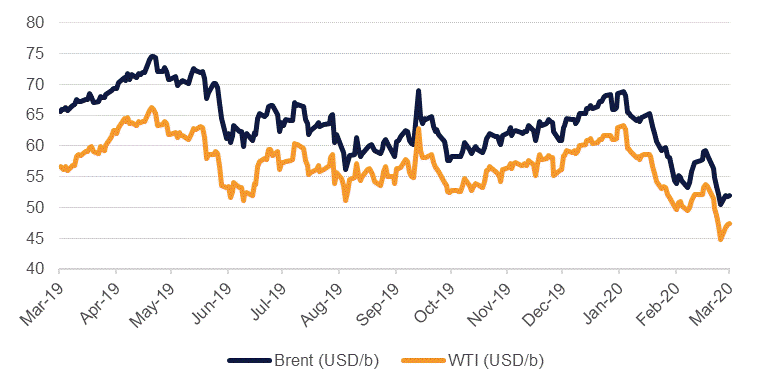

Oil markets have recovered ground this week on the expectation that OPEC+ will endorse a new and deeper level of production cuts when the producers’ bloc meets later March 5th-6th. Brent prices, which had moved below USD 50/b as fears that the outbreak of Covid19 would ravage oil demand, have moved back to nearly USD 53/b in anticipation of the cuts. How big OPEC+ is prepared to cut output remains unknown but markets appear to be pricing in a cut of at least 1m b/d. While significant in terms of getting the oil market closer to balance by the second half of the year, the scale of cuts appear unlikely to be enough to push prices out of their current range between USD 50-60/b.

OPEC+ has already implemented deeper cuts of 2.1m b/d from Oct 2018 baseline levels for Q1 2020. However, those production adjustments were outlined before Covid19 fully took hold in China and spread to other markets. Demand growth expectations for 2020 have been revised lower by all major forecasting agencies: the IEA expects global oil demand to contract by more than 400k b/d y/y in Q1, the first decline in total oil demand since the global financial crisis. The agency expects demand to recover over the rest of the year but still come in at only 825k b/d for 2020 as a whole, the slowest since 2011. We have incorporated the IEA’s projections for demand and non-OPEC supply as our baseline assumptions in determining the impact of OPEC+ production cuts.

If OPEC+ let its current deeper cuts expire and then returned to average 2019 production levels for the rest of the year, oil market balances would be biased toward inventory builds, with a surplus of around 1m b/d for H1 weighed against a modest deficit of around 400k b/d in H2. OECD stocks—measured in days of demand—would average 63 days for 2020, higher than their level in 2019 but not a substantial step-change. By all measures, such an outcome doesn’t appear particularly ominous for prices but we doubt the impact on oil consumption as a result of Covid19 will be as muted and short-lived as the IEA currently expects. The IEA’s next assessment of demand will be released March 9th, after the OPEC+ meeting and may provide a clearer indication of how badly demand has been impacted. Early data points from the period that Covid19 has taken hold have been dreadful: China’s February manufacturing PMI slumped to 35.7 from 50 a month earlier while PMI numbers across the rest of Asia have also declined.

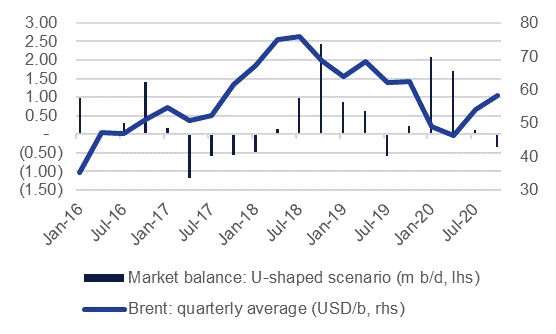

Source: IEA, Emirates NBD Research. Note: scenario oil price assumptions.

Source: IEA, Emirates NBD Research. Note: scenario oil price assumptions.

In a more U-shaped demand impact from Covid19—where demand slumps heavily in Q1, records no growth in Q2 and then tentatively moves higher by the end of the year—our baseline OPEC+ production views would mean a market surplus of around 0.9m b/d for the year as a whole, not just concentrated in H1. OECD stocks would blow out past 3.1bn bbl and take days of demand up to nearly 67 in Q2. The last time stocks were that bloated in H1 2016 Brent prices were in free fall, averaging just USD 35/b in Q1 2016 and USD 47/b in Q2 2016. A production adjustment clearly is imperative for OPEC+ producers to try and stabilize oil prices and avoid ballooning fiscal deficits or balance of payments crises.

Source: Emirates NBD Research

Source: Emirates NBD Research

OPEC’s own advisory committee has revised up its recommendation for cutting production to a range between 600k b/d to 1m b/d, from an initial proposal of just 600k b/d. A production cut of 600k b/d market balances would mean a roughly similar trajectory for oil market balances compared with our baseline although more exaggerated: a wider surplus in H1 compensated by a larger deficit of around 700k b/d in H2. However, the impact on OECD stocks would still mean days of demand widens to 64 on average for the year.

A 1m b/d would be much more significant in limiting a build in inventories even in a demand constrained environment. The H2 deficit would widen to 1m b/d and help to cap the increase in OECD days of demand. Commentary from OPEC officials is reportedly looking at 1m b/d as the target for a new level of cuts, hence the market anxiety that it sees at least that much agreed in Vienna. As ever with production cuts though, the traditional bugbear of compliance will temper their effectiveness. We have assumed compliance roughly level with where producers have been in the last few years of production restraint: high in the GCC, less so across the rest of OPEC.

Another significant variable here is how compliant non-OPEC members of the bloc are with the terms of the production cut. Russia is the most important producer outside of the core OPEC countries and our projections for balances in this scenario assume 100% compliance with its share of production cuts. At 70% compliance—roughly where Russia has been in the last rounds of cut backs—the impact of cuts is moderated. Russia was apparently not on board with the initially proposed increase to cuts of 600k b/d and the recent stabilization in prices—albeit at low levels—may give them further pause in endorsing a cut of 1m b/d.

While a 1m b/d cut may help to prevent inventories from expanding significantly, we expect it would entrench prices in the current USD50-60/b range for Brent rather than allowing them to push much higher even if a single variable pricing model suggests prices could improving back to a USD 60-70/b range by Q4. Weighing against the impact of the cuts is market anxiety over how bad the impact of Covid19 will be on the global economy—the US Federal Reserve’s emergency 50bps cut smacked of a panicked response while other central banks are expected to follow with easing. Moreover, there is roughly 1m b/d of Libyan production that is offline and could return in short-order following political stabilization in the country. Were Libya’s production to return to peak 2019 levels in H2 then 1m b/d of cuts would be effectively neturalized and the outlook for oil prices would be much worse.

If 1m b/d is endorsed as the cut by OPEC+ and the share of adjustment is roughly proportionate with the December 2019 agreement then GCC countries would bear almost 60% of the cuts. Production in Saudi Arabia would decline by more than 3% y/y while in the UAE output would be down by more than 4% and Kuwait would see production fall almost 3%. As Covid19 represents a serious threat to the region’s non-oil economies, particularly for the UAE’s travel and logistics sector, further production adjustments would add even more headwinds for domestic economies.

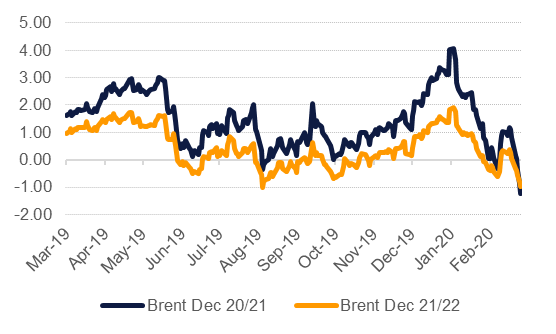

Aside from the negative economic impact, production cuts that only set a floor under prices, rather than push them higher, would be unlikely to shift market structures. December time spreads for Brent futures have moved back heavily into a contango of more than USD 1/b. While anxiety over demand remains a theme for the year we would expect the contango in Brent and WTI markets to remain intact, particularly if there are signs of progress on Libya’s peace talks.

Source: Bloomberg, Emirates NBD Research. Note: USD/b.

Source: Bloomberg, Emirates NBD Research. Note: USD/b.