Recent Search

Popular Searches

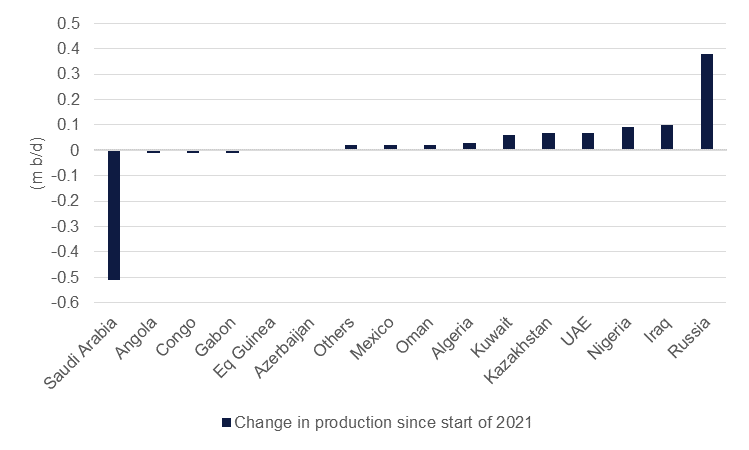

We expect OPEC+ will maintain its cautious stance when it meets again on July 1st and commit only to a modest increase in production from August onward. The producers’ bloc has tentatively returned some barrels to the oil market, increasing production by a collective 320k b/d by the end of May compared with the start of the year. Total production is still some 8.3m b/d below the peak level hit in April 2020 when several members were engaged in a market share battle.

Source: IEA, Emirates NBD Research

Source: IEA, Emirates NBD Research

However, since then the outlook for oil markets has turned much more positive. Demand in major markets is firmly in the upswing. Weekly data from the US show that oil consumption measured by product supplied is holding above 20m b/d, up from less than 14m b/d during the peak of the pandemic in April 2020 if still lower than pre-pandemic levels of closer to 22m b/d. Oil consumption in China is also on track to recover strongly, by more than 1m b/d according to the IEA’s estimates for this year as the economy has generally reopened even if demand for some products like jet/kero remains restrained.

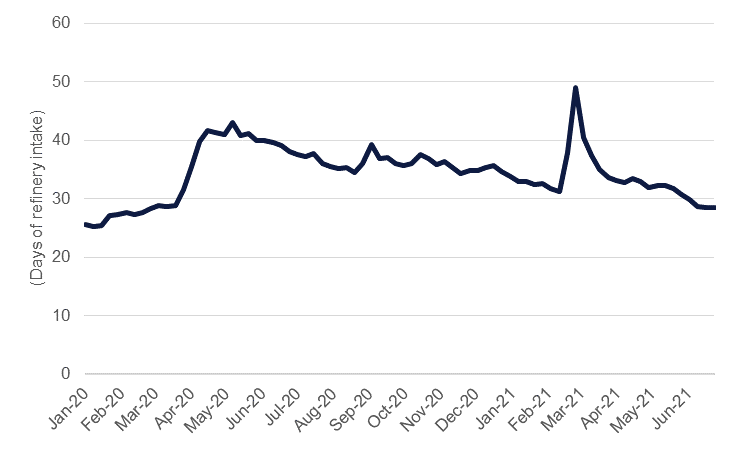

The build up in excess inventories caused by the drop-off in demand last year has also largely been worked through. Commercial crude oil inventories in the US have fallen more than 81m bbl since their April 2020 peak; measured against refinery input stocks now account for 29 days’ worth of demand compared with almost 43 days reached in May 2020 (notwithstanding a short-lived spike in February related to cold weather conditions). Inventories at the trading hubs of Singapore and NW Europe have also been trending steadily downward in the past year.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Furthermore, the timeline for an imminent and meaningful return of Iranian barrels is being pushed further back into the year as a deal between JCPOA counterparties has yet to be achieved. The election of a new Iranian president doesn’t on its own risk jeopardizing the prospect of a deal being reached but the diplomatic barriers to a deal remain wide.

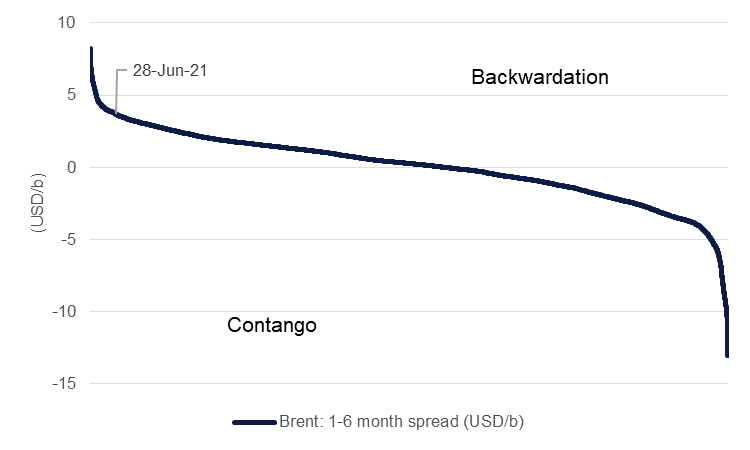

This combination of factors—along with OPEC+ supply restraint and limited supply response from other producers, such as the US shale patch—is setting the market up for considerable tightness. Market structures imply a substantially tight oil market in the second half of the year with 1-6 time spreads in the Brent market showing a backwardation of almost USD 3.70/b, around the 95th percentile of spreads in data back to 1990.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

OPEC+’s strategy of incrementally adding output this year has played out well for the bloc, allowing prices to rally 47% year-to-date in the Brent market, trading at more than USD 76/b at present. Commentary from Saudi Arabia’s energy minister, Prince Abdulaziz bin Salman, suggests to us that the country is not prepared to completely restore all its restrained production. In mid-June he noted that being “excessively cautious” had paid off and that the oil market was still “not out of the woods.” The uptick in Covid-19 cases in many economies in recent weeks related to the spread of the highly transmissible Delta variant does warrant some caution on strong linear recovery in oil consumption in the coming months.

Considering how high oil prices have reached mid-way through 2021, we would expect internal debate among OPEC+ members to increase in fervor. Some members may argue there is an opportunity for a moderate increase of 500-750k b/d of production for August onward. That wouldn’t push oil markets into surplus but could help to slow the current momentum in oil price rally. There is an awareness among OPEC+ members of letting prices rise too high; Prince Salman himself noted that OPEC+ had a responsibility in “taming and containing” broader inflationary trends that are playing out acutely in many emerging markets, forcing central banks to raise rates at a time when economies are still very much in recovery mode. India’s oil minister, Dharmendra Pradhan, has called on OPEC+ several times this year to bring output back online, including recently when he asked to keep prices in a “reasonable band.”

We will monitor the outcome of the OPEC+ meeting and adjust our oil market balances accordingly based on the outcome. For now, we maintain our view that oil prices will stay elevated with Brent futures at an average of USD 70/b in Q3 and Q4.