Recent Search

Popular Searches

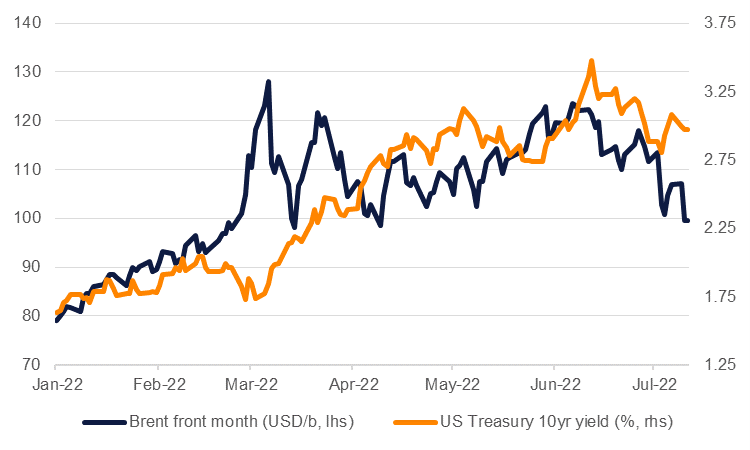

Oil futures have turned considerably lower in the last few weeks with both Brent and WTI front month contracts falling below USD 100/b as of mid-July. But time spreads across the curve remain in historically high backwardation and bids for physical barrels are strained at elevated levels. The oil market looks stuck then in a state of limbo, trying to determine whether it is indeed about to loosen substantially as a pending recession will ravage demand or whether, as cautioned by Fatih Birol, the executive director of the IEA, the world will move into an unprecedented “major energy crisis in terms of its depth and its complexity.”

At current prices, front month Brent futures have fallen USD 24/b from a recent peak in June of around USD 122/b. In WTI the fall has been as much as USD 26/b. The drop has come in line with a substantial pick-up in market anxiety over a looming global recession, prompted by central banks’ belated but aggressive response to dealing with inflation. The IMF has cut its expectation for US GDP growth this year to 2.3% from closer to 3% previously and warned that preventing a recession is “becoming increasingly challenging.” Meanwhile in the Eurozone, the prospect of a sustained interruption to energy supplies caused by the EU’s response to Russia’s invasion of Ukraine will exacerbate slowing growth and could induce a contraction in the economy.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Oil markets received a preview of demand deteriorating on weak economic activity thanks to China’s zero-Covid policy which the IEA estimated caused a demand drop of 840k b/d in May compared with the same month a year earlier. But like the dramatic slump in demand caused by the Covid-19 pandemic in 2020, the drop in China’s consumption was caused by public heath restrictions, rather than economic responses to prices. While major economies may show slower growth over the rest of 2022 and into next year, if not actually falling into recession, the impact on oil demand may be limited given the relative inelasticity of oil demand in the short term. During the global financial crisis in 2008-09, global oil demand fell by a bit more than 2.1m b/d over two years before it was more than recovered in 2010.

While the downside risks to economic activity and oil demand generally are salient, there are still considerable risks to supply over the next 12-18 months. Russia’s ability to freely export crude oil and other energy products is likely to become more proscribed once a comprehensive ban on EU seaborne imports of Russian oil and products takes effect toward the end of the year. Those sanctions will contribute to lower output levels from Russia though the degree of negative impact is still uncertain.

Among the rest of the OPEC+ producers, higher output targets have been agreed for July and August but the producers’ alliance has already been struggling to hit lower targets as member nations run up against capacity constraints. Saudi Arabia has a target level of more than 11m b/d for August which would mean an increase of more than 500k b/d from estimates of June production levels. How long Saudi Arabia can keep output at 11m b/d or higher, a level it has hit only twice before, is a considerable market uncertainty.

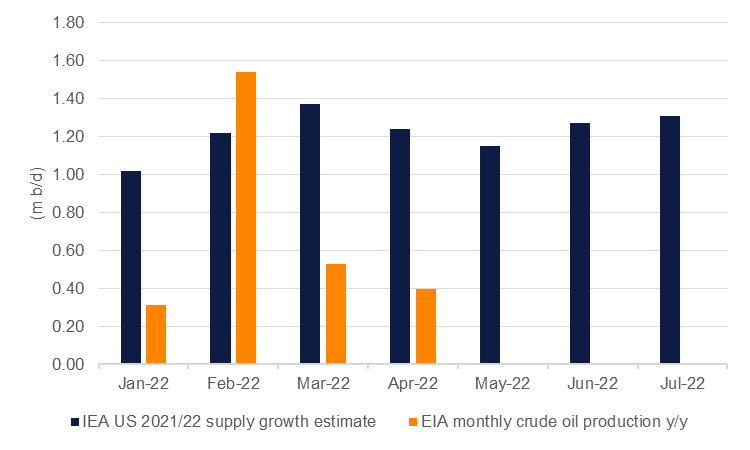

Oil production in the US is also coming in short of expectation in 2022. Forecasts of supply growth this year from the IEA have ranged from 1m b/d in the January oil market report to as high as 1.37m b/d in the March report. But actual output growth has so far come in short of those levels, averaging about 700k b/d in the first four months of the year according to the EIA’s measure of crude oil output. A marked acceleration in output will be required in H2 2022 in order to achieve expected levels though risks to supply chains and elevated labour costs may be a risk to sustained investment.

Source: IEA, EIA, Emirates NBD Research

Source: IEA, EIA, Emirates NBD Research

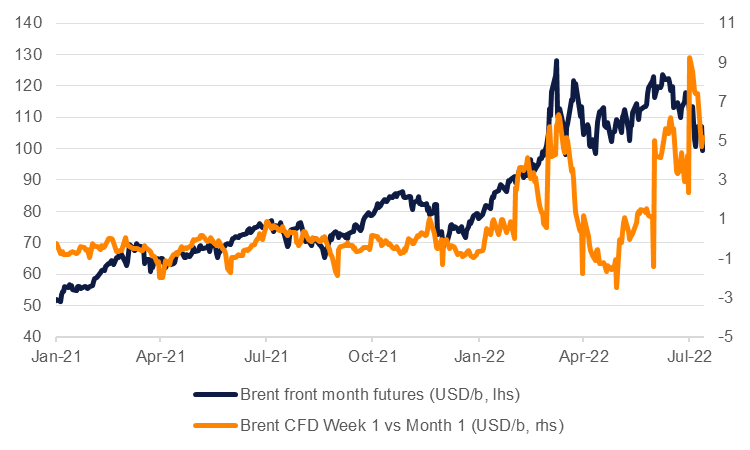

The different components of the oil market are picking up different parts of the macro narrative. Oil futures look to be focused on the recession risks and potential negative implications for demand while the physical market is looking squarely at the relative scarcity of barrels. Contracts for difference in the physical Brent market, a short-term derivative used to hedge oil loading in the very near term, remain at high levels even as spot futures have come off.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

We expect that supply risks will remain the primary factor in setting oil prices over the rest of 2022 and into next year. Our expectation for Q3 Brent is for an average of USD 120/b and we are holding to that view as we expect the sell-off should be reversed as supply shortfalls remain acute. In a best-case scenario where major economies avoid recession, there would be considerably upside risk to oil prices as supply fails to match higher marginal demand. But even in a recession scenario we expect that much of the sell-off in prices has already occurred, putting a floor on how much lower prices can go.

Edward Bell

Edward Bell