Recent Search

Popular Searches

Since the war in Ukraine began, the stance of OPEC+ and its constituent members has been that volatility in oil markets has “not been caused by fundamentals” but rather that the high prices at present are caused by “geopolitical developments.” At the same time, oil prices have cemented themselves above USD 100/b – the brief dip in April below that level caused by market focus shifting to the Covid-19 outbreaks in China – and markets seem to be preparing for higher prices ahead.

So how then can we assess whether the oil market is tight or loose and what variables will affect its progression in the coming months?

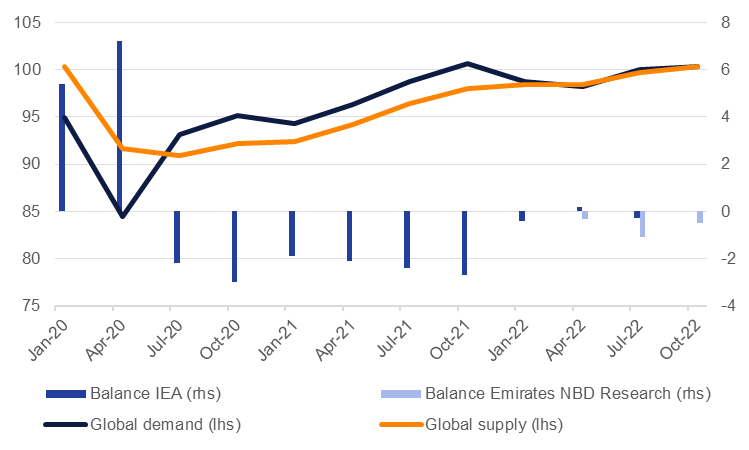

At the headline level we make use of the International Energy Agency’s balances to provide a sense as to whether the oil market is in deficit or surplus. For 2022 as a whole the IEA is projecting oil demand at an average of 99.4m b/d with demand growth of 1.8m b/d. On the supply side, the IEA estimates under its full OPEC+ compliance scenario total oil production of 99.2m b/d this year, leaving the oil market in a small deficit of around 125k b/d. The supply estimate, however, includes all OPEC+ members hitting their targeted production increases barring Russia, where the agency expects output to drop to 7.3m b/d by Q4 2022 compared with 10m b/d in Q4 2021.

Source: IEA, Emirates NBD Research

Source: IEA, Emirates NBD Research

By those measures, the shortfall in oil markets would appear manageable, even with such a dramatic drop in Russian oil output. But the rest of OPEC+ is failing to hit its targeted production levels as many members run up against capacity constraints and output from some OPEC members like Libya has proven to be highly volatile. In April, collective OPEC production rose by just 10k b/d month/month as output was disrupted in Libya, Nigeria and other smaller members. Our own projections for OPEC+ supply account for some producers failing to hit their targets while others like Saudi Arabia or the UAE come much closer. That results in a wider market deficit than the IEA projects under its full OPEC+ compliance scenario. The deficit won’t be as wide as what the market endured in 2021 but oil demand is basically back to pre-Covid levels and there is seemingly little flexibility on additional supply this year. That means that relatively small shortfalls will be amplified in their impact: every barrel will be that much more important this year.

Inventory numbers show draw across products and geographies

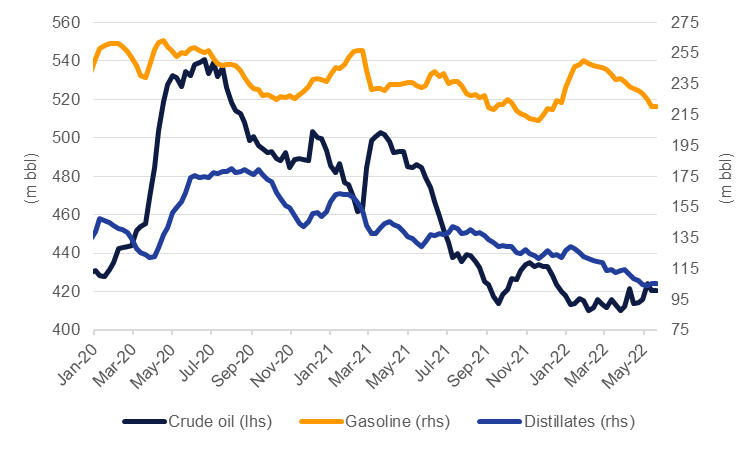

So on a headline basis the oil market will be in deficit this year, although to a varying degree depending on how generous of a production estimate is used. But oil market balances are pretty intangible measures, and generally observable only in retrospect. On a more near-term basis we can look at inventory levels in key trading hubs or pricing locations. Crude oil inventories in the US—excluding the strategic petroleum reserves—are down 13% y/y as of mid-May while stocks at the Cushing, Oklahoma pricing point for WTI are down 44%. Product inventories in the US are also tighter: gasoline stocks are down 6% y/y while distillates inventories are lower by 20% y/y.

Source: EIA, Emirates NBD Research

Source: EIA, Emirates NBD Research

Nor is the drain in inventories is a US-specific phenomenon. Product inventories in the ARA region of north-west Europe are down by more than 15% y/y with distillates and jet/kero accounting for much of the draw. In Singapore as well the middle of the barrel is leading the decline in inventories with total stocks down by 22% y/y as of mid-May with a near 50% drop in middle distillate stocks.

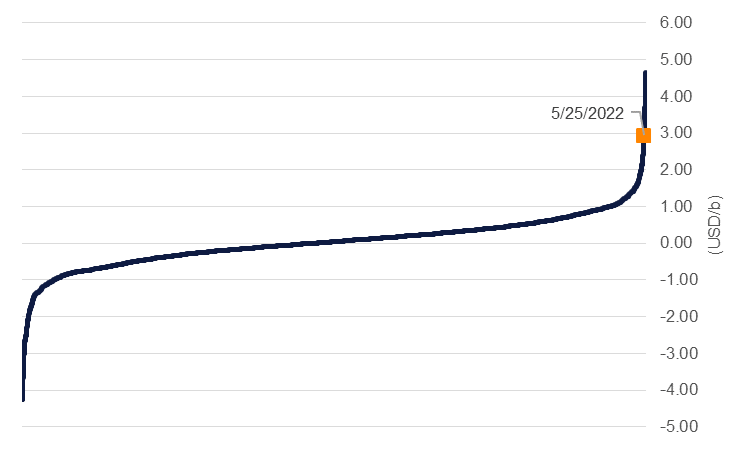

The most immediate litmus test for whether conditions in oil markets are tight or loose is the shape of the futures curve. Much like the yield curve in bond markets, the slope of the oil futures curve provides strong market-derived signals on conditions in oil markets. Currently the market is in a wide backwardation—near term prices are higher than longer-dated ones—meaning there is greater value placed on oil now, reflecting either strong demand or shortage of supply. As of May 25th, front month time spreads in the WTI market (the difference between the first and second futures contracts) are in a backwardation of USD 2.62/b, above the 99th percentile in data stretching back to 1990 and Brent, at a backwardation of USD 2.94/b, is at a similarly stretched reading.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

The OPEC+ argument that oil markets are currently distorted by geopolitical risks is not wrong. Sanctions from the US, UK and others on Russian crude and trade in Russian commodities are non-fundamental factors affecting markets and are not in and of themselves endogenous to oil and commodity markets. But the sanctions, or risk of an embargo on imports of Russian oil into the EU, are having a material impact on fundamentals with Russian oil output and exports of crude and products declining, leading to shortfalls in inventories. Market conditions continue to scream out for additional supplies but so long as OPEC+ keeps its focus on “fundamentals” we expect oil prices will continue to price in considerable tightness, meaning high and volatile prices will persist.