Recent Search

Popular Searches

Oil markets have run up against headwinds in the second half of 2022. China’s zero-Covid policy remains an impediment to global demand growth as the country continues to restrict mobility and broader economic activity. At the same time central banks globally are moving in a much more aggressive manner to tighten monetary policy to cool inflation, clouding the outlook for oil consumption. Balanced against that though is still a precarious supply scenario with OPEC+ showing a bi-directional approach to production targets and flows of commodities being subjugated to the political consequences of Russia’s war in Ukraine.

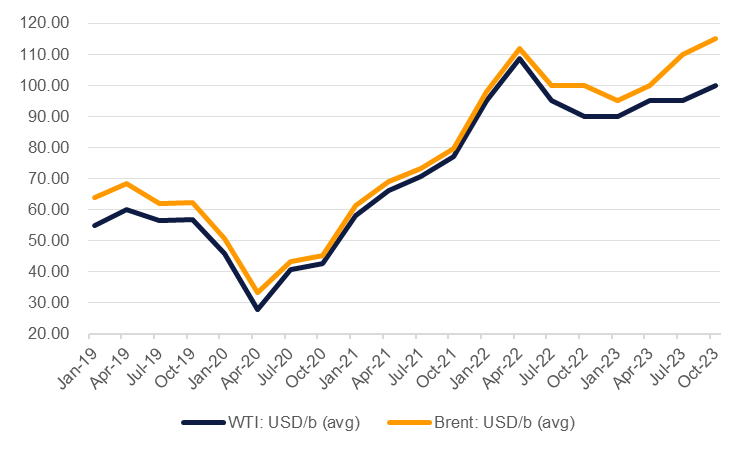

For now, the negative mood around global growth is pulling oil markets lower with Brent futures at around USD 92/b as low as they were ahead of Russia’s invasion of Ukraine. Prices have fallen more than 30% since their year-to-date peak of USD 139/b hit in March and look set to at least linger around current levels until the end of 2022. We are adjusting our forecasts for average Q4 oil prices to USD 100/b in Brent, down from USD 115/b previously, and for WTI we are lowering our view to USD 90/b, down from USD 110/b previously.

For 2023 we expect Brent at an average of USD 105/b. However, the trajectory of prices has shifted as we expect balanced conditions in the first half of the year to give way to a sustained deficit in H2, meaning prices move from low to high over the course of 2023 with a target of an average of USD 95/b in Q1 rising to USD 115/b by Q4. In WTI we expect prices at an average of USD 95/b in 2023 with a pattern roughly similar to what we’ll see in Brent, with low prices earlier in the year giving way to higher ones later on.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Demand contingent on China’s Covid stance

Oil demand growth in 2023 is set to come out not far off 2022 levels with the IEA projecting consumption growth of 2.1m b/d vs 1.99m b/d this year. Demand growth will slow sharply in OECD economies as consumers adjust to high prices for retail fuels, tighter central bank policy and an overall slowdown in economic activity. But while consumption growth will slow, it doesn’t look as though it will go negative at this point. Retail gasoline sales prices in the US have fallen in line with crude oil prices, reaching USD 4.31/g as of mid-September, down from almost USD 5.50/g in mid-June. European gasoline prices have also moved lower though not to the same degree seen in the US. Depending on the severity of a pending recession in the Eurozone or the US, demand for retail fuels may find a bottom given the relative inelasticity of oil consumption to economic growth in mature markets.

The balance of risks in the near term though appears weighted to the downside as China’s restrictive Covid policies remain intact. The manufacturing PMI remains near or in negative territory and barriers to moving in and out of the country, as well as within it, are limiting oil demand. The IEA estimates total Chinese oil demand fell by nearly 1m b/d y/y in July with jet fuel/kerosene leading the way lower. Total jet fuel demand is expected to drop by nearly 24% y/y in 2022. An unfolding property market crash is also weighing on the outlook for growth and expenditure. That said, recent data points suggest a bottoming out of the economic slump with industrial production performing better than expected in August and retail sales for the same month coming in at their strongest level since July 2021. Until there is a firm path for China out of its Covid policies, oil markets will be running against a considerable headwind.

.png)

Source: IEA, Emirates NBD Research. Note:

The demand outlook for 2023 then looks to be roughly similar to what oil markets encountered this year with the notable caveat that China easing its zero-Covid rule would unleash an enormous amount of pent-up demand and tighten markets considerably.

Security of supply remains a concern in 2023

For supply the picture is more uncertain. Russia’s invasion of Ukraine has upended energy markets as commodities are being used as political tools as much as enablers of economic activity. Security of supply will become a much more critical issue in oil markets going forward than it had been in the pre-pandemic years where OPEC and partners had to routinely make space for the surge in output from unconventional oil producers, particularly in North America.

EU sanctions on Russian seaborne exports of crude oil take effect in December 2022, shrinking the availability of supplies to Europe. In an effort to prevent Russia diverting cargoes to other economies, G7 nations have agreed to a price cap mechanism, to be enforced by suspending the provision of insurance and other ancillary services for trade in Russian oil. Whether the price cap will indeed be effective in limiting revenues to Russia’s government and its overall impact on oil market balances is still uncertain as few details of the mechanism have been released. But EU sanctions are still likely to accelerate the drop in Russian crude oil production which has been underway since the war in Ukraine began. Diverting cargoes to countries that haven’t signed up to the price cap—India or China for instance—will also have no guarantee of success if economic growth does slow materially.

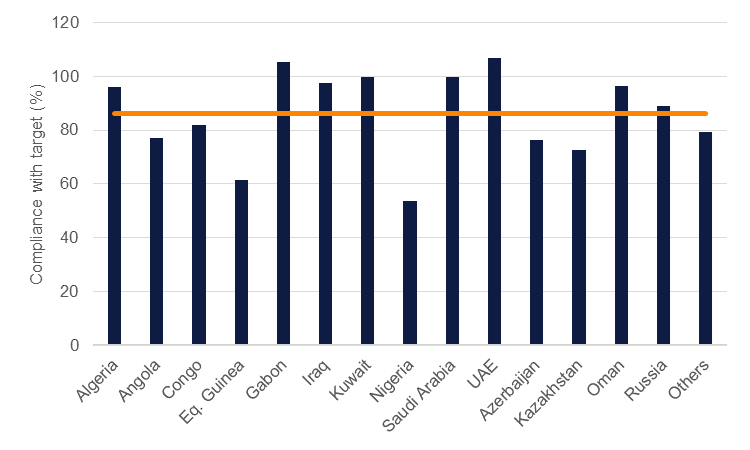

With uncertainty on the level of Russian supplies, the rest of OPEC+ will be under more pressure to make sure supplies are available. However, there has been some transparent unease within the producers’ alliance at how far prices had fallen over July-August and OPEC+ responded in early September by announcing a production cut for October levels. We doubt this will be the last downside adjustment to production targets from OPEC+ and in any case, several members have missed their output targets by a wide margin: Nigeria is producing 850k b/d below its target level for instance. OPEC+ may endorse a more material cut to monthly production targets, by as much as 500 – 750k b/d perhaps, if there is a genuine effort to put a floor under oil prices.

Should demand growth stabilize or come in ahead of expectation in 2023, there may be limited ability for OPEC+ to respond with spare capacity effectively held by just the UAE and Saudi Arabia. As noted many producers have been unable to hit their targets and Saudi Arabia has shown hesitancy to deploy its spare capacity. One source of untapped oil is Iran though negotiations for a resurrection of the JCPOA—the Iran nuclear deal—look to have halted as none of the signatories appear ready to accede to the demands of the others. We are not counting on Iranian production materially increasing over the rest of this year or next.

Source: IEA, Emirates NBD Research

Source: IEA, Emirates NBD Research

Production from the US is set to expand in 2023 though we are far past the period when the shale basin would produce double digit growth rates. Recently there has been a plateau in the number of rigs targeting oil production—holding at around 600 since the start of July and roughly a third below levels seen before the pandemic. Output per rig is also declining as firms need to target marginal reserves. With high borrowing costs, volatile equity markets and a less enthusiastic investor bias toward oil and gas production, the capital available for further upstream investment in the US is likely to be ever more constrained. Production in the US is set to grow by a bit more than 1m b/d in 2023, roughly on par with this year’s estimate although output in 2022 is so far running short of target.

Markets to move into deficit by H2 next year

We project oil markets will be roughly balanced in the first half of 2023 before a more considerable deficit emerges in the second half of the year. This is based on the assumption that OPEC+ holds output relatively stable in aggregate with some countries producing above target and others missing. However, should China emerge from its restrictive Covid rules then balances may tighten considerably earlier. Already we project OECD stocks measured against days of demand at 59 in Q1, below long run averages of about 62 days' worth, but that number drops to 54 days of demand by Q4.

Edward Bell

Edward Bell