Recent Search

Popular Searches

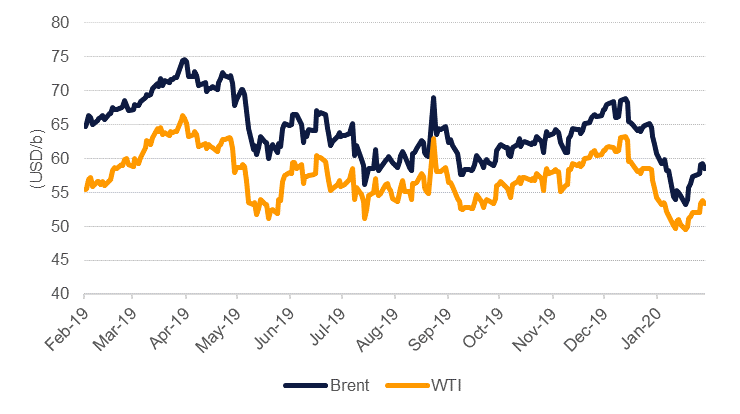

Oil markets managed to hold on for another week of gains, with both Brent and WTI futures rising more than 2% last week. Brent closed at USD 58.50/b while WTI settled at USD 53.38/b. Both contracts slipped in their final day of trading as fears that the Covid-19 outbreak was entrenched elsewhere in Asia—South Korea and Japan in particular—weighed on markets. Poor PMI data from the US also helped dragged risk markets lower at the end of the week as the US composite PMI for February fell to 49.6, its weakest level since 2013. US economic data has generally held up in recent prints but the dip in business activity may reflect waning confidence in the outlook for the rest of the year should Covid-19 erode external demand.

Several major OPEC producers are considering a stand-alone cut of 300k b/d according to press reports. Saudi Arabia, the UAE and Kuwait have reportedly discussed the additional cuts as achieving a broader OPEC+ consensus on cutting output has proven to be a challenge. The plan has been denied by official sources from the countries and on its own would do little to offset the significant drop in crude demand from Chinese refineries. OPEC has officially confirmed its next extra-ordinary meeting for March 5th and will hold a session with partners such as Russia the following day.

Market structures also rallied in line with the improvement in spot prices. Brent has returned to backwardation after a brief dalliance with contango; the 1-2 month time spread ended the week in a backwardation of USD 0.56/b while longer-dated spreads ended the week in much higher backwardations. WTI also showed a substantial improvement with the contango at the front of the curve falling to just USD 0.12/b from nearly USD 0.3/b a week earlier. While there is some apparent optimism in markets that China’s authorities are getting the viral outbreak under control we suspect some of the improvement in the WTI and Brent curves is premature. China’s industrial economy is still running at a diminished capacity and lingering fears over the virus spreading will curb air travel for much of H1 2020. The Brent curve could be at risk of slipping back into contango should OPEC+ fail to agree any substantial change in output levels or the length of their current production cut levels.

Investors continued to pull long positions out of Brent and WTI futures and options. Speculative net length in WTI fell by 27k contracts last week while Brent was relatively unchanged. Put premiums widened last week in both the Brent and WTI first expiring contract although risk-reversal strategies still appear relatively sanguine considering the level of downside risks affecting markets. Put options for June Brent at a USD 55/b strike have slipped around 50% from their ytd high earlier in February.

As crude futures have staged a bit of a recovery in the past two weeks, jet fuel has stabilized as air travel remains under tremendous scrutiny. Singapore jet fuel swaps have held at around USD 65/b over the past two weeks while jet cracks over Brent have fallen to their lowest levels since 2016.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Edward Bell

Edward Bell