Recent Search

Popular Searches

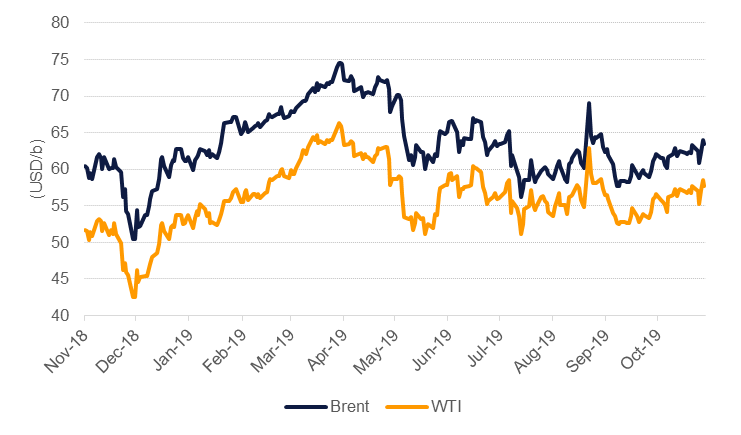

Oil markets remain spellbound by US-China trade headlines, leading to choppy trading over the last five days. After recording greater than 1% moves each day last week Brent futures ended the week at USD 63.39/b, a gain of just 0.14%, while WTI was up even less, settling the week at USD 57.77/b. Markets were devoid of any significant fundamental catalyst specific to oil, contributing to volatile trading: moves in the futures market showed a greater than 1 standard deviation change on three out of five days last week.

OPEC holds its next meeting on December 5th, joined by non-OPEC participants in its production cuts the following day. Faced with a 2020 demand outlook that is beset with downside risks thanks to the trade conflict and general downturn in industry globally, OPEC+ has few enviable choices at its meeting. A rollover of the current production cut agreement appears to us the most likely outcome although there is a chance the producers’ bloc could endorse deeper level of cuts. But there is no guarantee that heavier cuts would result in prices ending up near where OPEC+ economies need them to balance budgets or keep external accounts stable. A higher level of cuts of 1.75m b/d (a near 50% increase on the current agreement of 1.2m b/d) would still result in a surplus of around 800k b/d in H1 2020 before a moderate deficit emerges in H2. That also assumes that all participants achieve 100% compliance with the higher level of cuts. Considering OPEC+ performance this year where good aggregate compliance has only been achieved thanks to enormous over-cutting by Saudi Arabia, we doubt that 2020 would see any improvement in individual country compliance.

OPEC’s outlook for 2020 highlights the challenge of using heavy handed production cuts to impact oil market balances and prices. OPEC lacks enforcement mechanisms to punish producers who breach target levels. An increase in production by one party aimed at pushing prices lower—to penalize recalcitrant members—is felt by all, including the enforcer. Indeed, such an increase in output could end up backfiring further as all members raise output to keep their market share intact.

Similar to flat prices, time spreads showed little movement over the past week. Dec spreads for both Brent and WTI in the 20/21 spread were marginally higher and there was a modest strengthening at the front of the curve. Dubai spreads showed a stronger pull upward, closing at USD 2.40/b in the 1-3 month spread, compared with less than USD 2/b at the end of the prior week (according to Bloomberg data). The Brent/Dubai spread narrowed thanks to a tighter picture for heavy, sour grades. A rail strike in Canada is impacting flows of crude oil from producing provinces, helping to tighten up an already relatively short market.

Investors tempered their recent buying frenzy on Brent and WTI. Net length in WTI positions fell by more than 19.5k lots last week as longs were closed out a second week running while in Brent net length rose by just 543 contracts thanks to muted growth in long positions and some new, although small, short positions being added.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Edward Bell

Edward Bell