Recent Search

Popular Searches

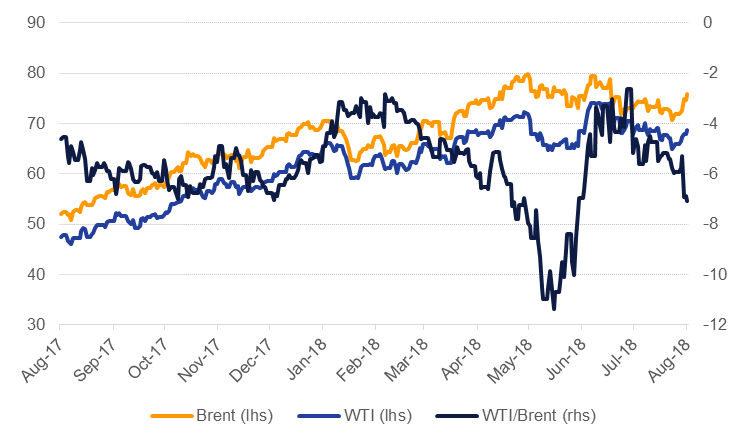

Oil markets snapped their string of weekly declines last week with both Brent and WTI futures gaining strongly. WTI added 4.3% over the week to close at USD 68.72/b while Brent gained 5.6% to end the week at USD 75.82/b. Signs of trade tensions easing between the US and China helped catalyze a broader upward move in commodities with most industrial metals also recovering some of the ground they had lost in the previous week. Both oil benchmarks are trading toward the upper end of their one-year range with levels of USD 80.50/b for Brent and USD 69.02/b for WTI the next upside targets.

The IPO of Saudi Aramco has reportedly been put on hold, removing one of the major oil market dynamics of the last two and a half years. We had never expected that the IPO would mean a shift in Saudi Arabia’s oil market policy as investors would have held a small share of the company and broader national economic objectives will set the tone for oil policy. However, the removal of the ‘Aramco put’, an implicit assumption that Saudi Arabia would keep oil prices above a certain level to support the valuation of the company, does raise some downside risks to prices if a USD 2trn valuation of the company is no longer officially in development.

Forward curves diverged over the course of trading with Brent spreads holding relatively steady for the 1-2 month spread while WTI oscillated quite sharply. Brent finished the week in a contango of around USD 0.3/b for the 1-2 month spread compared with a level around USD 0.2/b a week earlier. WTI, however, narrowed its backwardation from USD 0.7/b to just USD 0.36/b over the five days. December spreads improved across both 18/19 and 19/20. Despite the gains in spot prices, sentiment toward oil still remains soft. Net length in both WTI and Brent futures and options fell last week and there was a sizeable (14.6k contracts) increase in short positions in WTI.

In the US, exploration and development companies took nine rigs out of operation last week, the largest weekly drop since 2016. WTI calendar strips for 2019 have held in a range of USD 62-69/b for most of Q2 and Q3, providing headroom for oil companies to profitably drill wells when hedged with futures prices. However, physical pricing has yet to show signs of material improvement, particularly in Texas: WTI Midland closed at a discount of USD 15/b to NYMEX WTI last week.

US crude stocks fell 5.8m bbl according to the latest EIA data while production edged back up to 11m b/d. Total inventories—products and stocks—fell by 2.5m bbl last week and remain roughly level with their five-year average. Product inventories in both Singapore and ARA fell last week.

Source: Eikon, Emirates NBD Research.

Source: Eikon, Emirates NBD Research.

Click here to Download Full article