Recent Search

Popular Searches

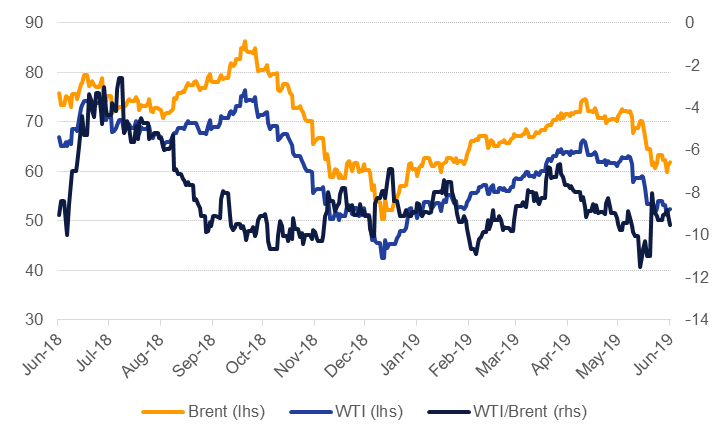

Oil markets were wrenched by competing forces last week as anxiety over global demand conditions weighed on prices to start trading while elevated geopolitical tensions boosted prices toward the close. While prices did surge on news that two tankers were damaged in the Gulf of Oman, just outside of the Strait of Hormuz, benchmark futures closed the week lower at USD 62.01/b for Brent (down 2% over the week) and at USD 52.51/b for WTI, down 2.7%. Brent is now nearly 17% lower than its year-to-date peak of USD 74.57/b while WTI is officially in a bear market, having fallen 20.8% from its peak of USD 66.30/b.

All major forecasting agencies lowered their demand projections for 2019 as the EIA, OPEC and IEA all pointed to the uncertain impact a global trade war will have on commodity demand. The IEA in particular suggested that fiscal stimulus should help to support growth in the second half of the year. However, we would caution that many emerging markets face elevated debt-servicing costs as benchmark rates have risen and may not be as free to carry out heavy handed stimulus to support growth. Oil demand normally picks up in the second half of the year on seasonal factors but with a highly uncertain outlook for trade relations between the US and China we aren’t holding out for a significant boost in consumption.

An elevated geopolitical atmosphere in the Middle East won’t help investor confidence if there is a perceived risk to security of oil supply coming out of the Gulf region. These recent attacks on tankers follow shortly on from attacks on tankers in Fujairah around a month ago. Oil production from countries using the Strait of Hormuz as an export route has declined by 1.47m b/d since the start of the year (according to Reuters data) as OPEC members restrain output and Iranian output is under US sanctions. OPEC reported that Iran’s production had fallen to 2.37m b/d in May, down 1.45m b/d from the same month in 2018, while exports were estimated at just 500k b/d in May. Importers of Iranian crude will likely continue to shun the country’s cargoes, helping to keep oil markets tight over the next few months.

The perceived risk of crude supply coming out from the region will be a focus for OPEC+ as it decides whether or not to maintain production cuts into the second half of the year. We expect a roll-over of the production cut deal but that compliance (actually, over-compliance) will start to ebb for two reasons. First, heightened geopolitical risk will give a boost to oil prices that may be too tempting for exporters to resist. One-off geopolitical flashpoints like these attacks tend to have a fleeting impact on crude markets but if events like this occur with regularity it will help to keep a floor under prices. Second, OPEC producers, particularly major ones like Saudi Arabia and the UAE, will want to reassure off-takers over the availability of their crude exports at a time when alternatives are available: the US exported more than 3m b/d in the week ending June 7th, more than the entire production of the UAE. OPEC’s latest report estimated Saudi Arabia achieved 293% compliance with its production target, giving the kingdom ample room to increase output and not breach OPEC targets.

Forward curves in both Brent and WTI suggest to us that the fear of a trade war cratering oil demand still remains the dominant risk for the rest of the year. Front month backwardated spreads in Brent gained on news of the tanker attacks but still closed the week lower while the contango in WTI deepened (another build in US crude inventories highlights the relative oversupply in US vs international oil balances). Longer dated spreads look particularly vulnerable to trade war risks. Brent Dec spreads for 20/21 are almost in contango, having fallen from almost USD 3/b in May to barely above neutral now.

Investors continued to close long speculative positions in Brent and WTI and added shorts for the seventh week in a row in WTI. Meanwhile the US drilling rig count fell by one rig last week. The US rig count has fallen by 97 rigs since the start of the year but output has managed to still increase, up by 1.4m b/d (almost 13%) as of June 7th y/y. The pace of US supply growth is slowing but still remains at exceptionally elevated levels.

Source: EIKON, Emirates NBD Research.

Source: EIKON, Emirates NBD Research.

Edward Bell

Edward Bell