Recent Search

Popular Searches

Oil markets weren’t spared the savaging that equity markets fell under last week despite there being no single fundamental catalyst to send equity indices or oil prices sharply lower. Brent futures closed the week down more than 4.4% and have regained a USD 80/b while WTI fell more than 4% to close at USD 71.34/b. An increase in general risk asset volatility will weigh on oil markets in the near term and a deeper push downward would appear the easiest direction of travel.

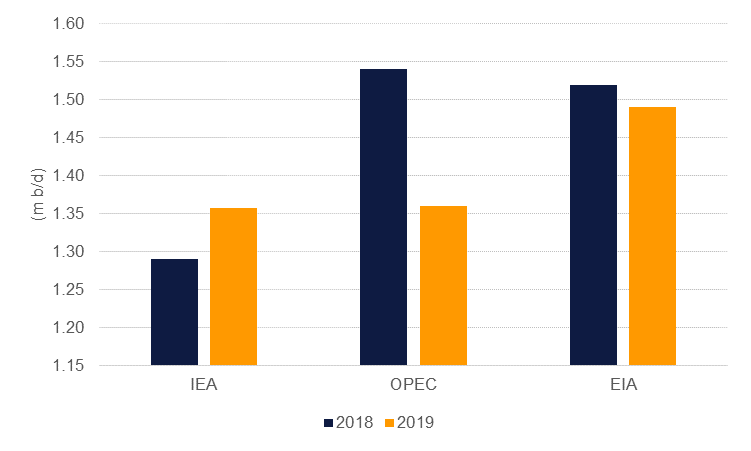

Both the IEA and OPEC cut their oil demand growth forecasts for 2019 last week on a weaker economic outlook in several large oil importers. The IEA expects 2019 demand at 1.36m b/d, up from 1.28m bb/d this year while OPEC sees an opposite trajectory, with growth slowing from 1.5m b/d to 1.36m b/d next year. Both agencies cautioned that oil markets were currently adequately supplied which may give OPEC oil market policymakers pause as they consider whether to raise production and possibly cause a market surplus in 2019. We still see considerable uncertainty in the 2019 demand outlook but find an acceleration in oil demand growth an outside chance, rather than our core expectation.

In line with the sell-off, there was considerable flattening in forward curves last week and in the WTI market in particular, the curve is noticeably flat from 1-9 months out. We see a growing risk that the WTI market flips back into contango as production continues to increase despite broader fundamentals still looking shaky. The increase in interest rates will also erode roll yields and has likely already pushed it negative.

Sagging roll yields for WTI likely explain why long positions have been cut for five weeks in a row. Net length fell by more than 36k contracts last week as shorts began to add up. The drop in Brent length was far less severe (more than 6.4k contracts); however, long positions have fallen in the past two weeks as investors may be estimating that recent highs of nearly USD 87/b are the top of the current cycle.

Outside of financial markets though exploration and drilling companies picked up activity last week. The rig count rose by 8 rigs, more than unwinding the last three weeks of decline. Indeed, earlier in the week the EIA raised its forecast for US supply growth even as infrastructure constraints still bottle up crude away from higher valued markets. Spreads for US producers have started to stabilize although there was sharp move downward in Bakken spreads over WTI.

US crude stocks rose nearly 6m bbl last week, extending the run of inventory builds to three weeks in a row. Total petroleum inventories rose by more than 11m bbl last week and are increasingly moving further above their five year average. The rapid pace of refinery utilization in the past few months has helped to keep gasoline inventories high and also seen a noticeable pick up in jet inventories.

Source: IEA, OPEC, EIA, Emirates NBD Research.

Source: IEA, OPEC, EIA, Emirates NBD Research.

Click here to Download Full article