Recent Search

Popular Searches

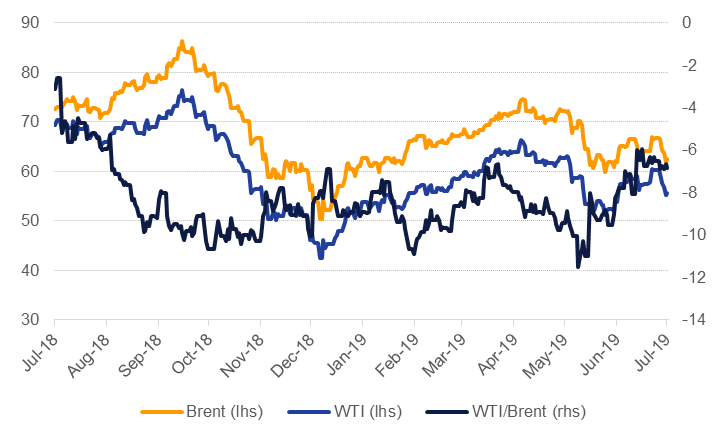

Oil markets weakened considerably last week despite an escalation of geopolitical tension toward the end of trading. Brent futures closed down 6.4% over the week at USD 62.47/b while WTI lost 7.6% to close the week at USD 55.63/b. The seizure of UK oil tankers and destruction of an Iranian drone have again raised concerns over the security of supply coming out of the Strait of Hormuz and helped prices stem losses somewhat on Friday. The market expectation of the US Federal Reserve cutting rates later this month is also weighing on the dollar, easing one additional headwind for crude and commodity prices.

Tensions in the Gulf remain high but they are occurring simultaneously with more uncertainty about the trajectory for global growth—China’s economy expanded by the slowest pace in nearly three decades in Q2—and a substantial downgrade by the IEA for oil demand growth. According to commentary from the IEA director, the agency expects demand to expand by just 1.1m b/d this year, compared with previous expectations of 1.2m b/d and 1.4m b/d at the start of the year. While we await the full breakdown of the demand profile, growth of just 1.1m b/d represents the slowest pace of demand growth since 2014—when Brent futures averaged close to USD 100/b—and will likely lead us to revise our market balances for H2 into considerable inventory builds.

Forward curves in both Brent and WTI dropped as worsening demand conditions weigh on forward pricing. Time spreads at the very front of the curve dipped to a contango of USD 0.13/b for WTI and a backwardation of just USD 0.19/b for Brent. Only one month earlier the backwardation for 1-2 months in Brent had been as high as USD 0.95/b. Longer-dated spreads have also collapsed with Brent Dec spreads losing nearly USD 1/b for 19/20 and the same spread for WTI falling more than USD 1.2/b over the week. Dubai 1-3 month spreads have managed to hold their recent strength, helped by the intensifying risks in the Gulf, and closed the week at USD 1.33/b. Dubai spreads are still below their year-to-date highs of over USD 2/b but recent gains may allow regional NOCs to reverse some of the latest cuts to OSPs.

Investors moved heavily back into speculative positions in both Brent and WTI, adding sizeable new long positions. Net length in Brent increased for the first time since the start of May thanks to more than 22k new long positions while WTI net length rose by 41k contracts. We still wouldn’t rule out a disorderly exit out of Brent should forward curves weaken even more or weak demand considerations overwhelm supply risks over the next few months.

Product prices have eased back from recent highs across all major trading hubs but cracks still remain strong thanks to the relative worsening fundamentals for crude. Inventories in Singapore have stood out in their declines relative to the US or ARA, particularly at the top and bottom of the barrels.

Source: EIKON, Emirates NBD Research

Source: EIKON, Emirates NBD Research