Recent Search

Popular Searches

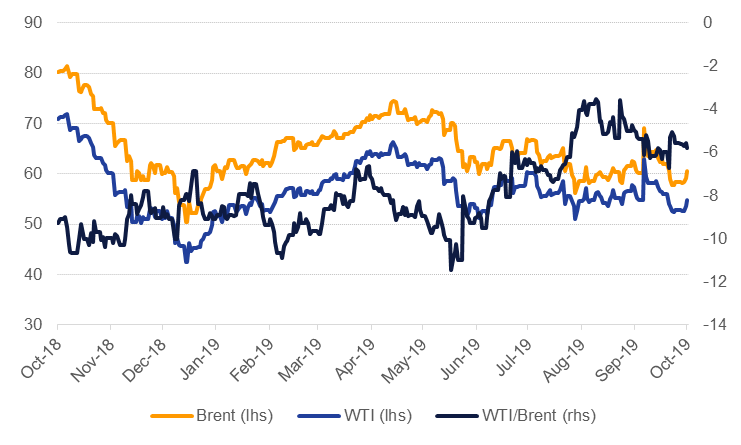

Oil markets managed to snap a few weeks of losses as risk appetite returned last week. The outlines of a US-China trade deal propelled oil prices higher, helping Brent futures close up 3.7% at USD 60.51/b and WTI up 3.6% to close at USD 54.70/b. Financial markets generally got a boost from the chance of a trade deal along with hope that no-deal Brexit could be avoided. More specifically to oil markets, another bump in geopolitical risks kept oil prices from slipping as an Iranian oil tanker has reportedly been attacked.

The IEA and OPEC released their monthly market reports last week and both agencies shaved lower their demand expectations for 2020. The IEA projects demand growth at, what it calls, a “still solid” 1.2m b/d while OPEC’s projections were for a little more than 1m b/d. The IEA highlighted the relative lack of price movement in response to attacks on oil infrastructure in Saudi Arabia in September as concern over demand and non-OPEC supply growth capture markets’ attention. In OPEC’s report, Saudi Arabia self-reported a decline of 660k b/d in September while the secondary source estimate was nearly twice as much. OPEC actually revised up its call on OPEC crude for 2020 to 29.54m b/d but that still represented a drop of almost 1.2m b/d from its 2019 estimate.

OPEC’s secretary general, Mohammad Barkindo, indicated the producers’ bloc could consider deepening its production cuts when it meets again in December. Deeper cuts could come for two reasons. First, OPEC (and its partners) could keep their market management strategy in place with the aim of supporting prices and drawing down inventories. So far this has helped to keep prices from collapsing but we don’t see much more upside to oil prices if cuts are deepened. A second reason may be more ominous: cutting output to match lower levels of demand. The outlook for 2020 remains clouded by the outcome of US-China trade talks, central bank action, trade growth—among other factors—but it should be plainly apparent to markets that no major agency is revising their demand forecasts higher. Cutting in that scenario would amplify the downside risks to demand rather than spark much optimism over prices.

Spot prices may have rallied last week but forward curves are losing some strength. Brent 1-2 month spreads closed the week at USD 0.39/b in backwardation compared with USD 0.63/b a week earlier. WTI likewise lost support at the front of the curve and the 1-2 month spread dipped back into contango. Dubai spreads have stabilized at a backwardation of around USD 2/b in the 1-3 month spread, lower than their level around the time of the Aramco attacks, but still displaying some sensitivity to geopolitical risk.

Investors continue to abandon positions in crude futures and options with net length in WTI and Brent declining by more than 40k contracts each! Investors are accumulating short positions in WTI as the curves failure to sustain a backwardated structure highlights the persistent oversupply of the market in the US while Brent does not seem to be attracting geopolitical risk premium hunters. E&P companies in the US, however, did add two rigs last week, the first increase in the rig count since August.

Source: EIKON, Emirates NBD Research.

Source: EIKON, Emirates NBD Research.

Edward Bell

Edward Bell