Recent Search

Popular Searches

Oil markets appear to be now pricing in some chance that Iran will resume oil exports on a large scale following a potential diplomatic breakthrough where the US and Iran return to the terms of the Joint Comprehensive Plan of Action. Negotiations between counterparties to the JCPOA, the Iran nuclear deal reached in 2015, have been ongoing for the past several weeks and officials have spoken positively about their tenor, even if substantial issues around the parameters of nuclear monitoring and regional geopolitics are outstanding.

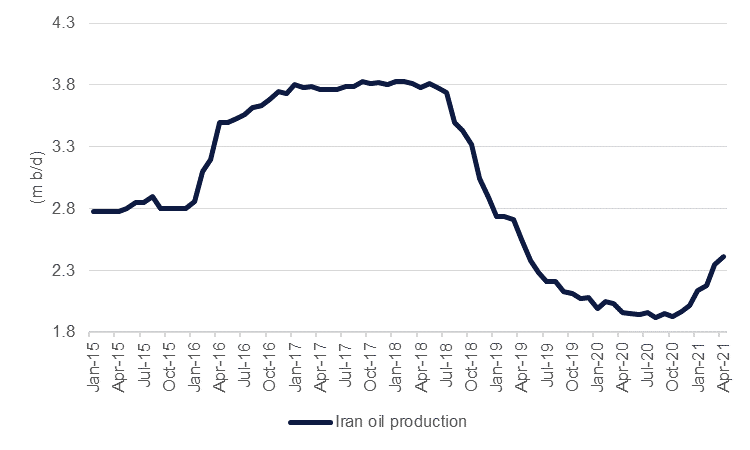

After being agreed during the Obama administration in mid-2015, the JCPOA lifted sanctions on Iran in early January 2016 and allowed the country to increase oil production rapidly. Oil output in Iran had fluctuated between 2.5 – 2.8m b/d during the period from 2012-15 when it was under international sanctions but then jumped by 700k b/d in just five months in 2016 after sanctions were lifted. When the Trump administration pulled the US out of the deal in May 2018 output fell rapidly, moving from around 3.8m b/d to 2.9m b/d by the end of that year and then drifting lower to less than 2m b/d by early 2020.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Should the US and Iran manage to come to a diplomatic agreement we would expect Iran’s oil production to be able to rebound in relative short order. Production has already been moving steadily higher in 2021 so far, edging up to around 2.4m b/d in April from around 2m b/d at the end of last year, according to market surveys. If a post-sanctions recovery followed a similar trend to 2016 then Iran could see output rise to 3m b/d or more by Q4 2021.

We can’t forecast the direction of travel for the diplomacy between Iran and the US but the market hadn’t appeared to price in a return of Iranian crude in a meaningful way until recently. The Russian representative to the IAEA, the UN’s nuclear energy supervisory agency, noted this week that “significant progress” on talks had been made but later tempered his comments by noting that “unresolved issues remain” and that a timeline for a return to the JCPOA hadn’t been set. Brent futures had briefly moved above USD 70/b on May 18th before pushing lower in response to, among other things, the mood around the JCPOA diplomacy.

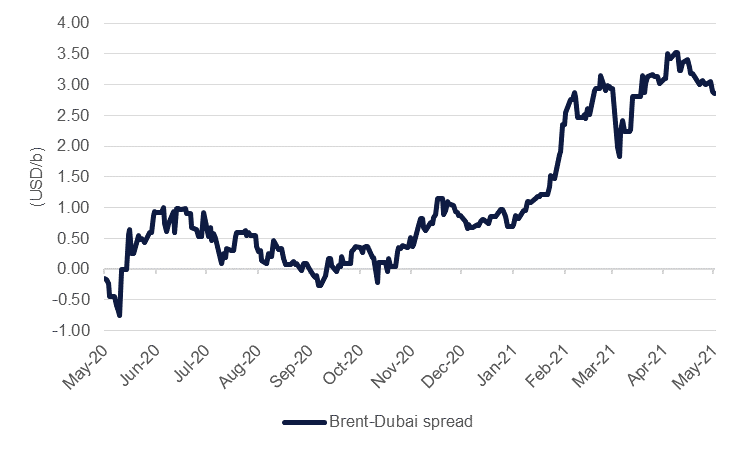

Signals from the physical oil market have also been pricing in greater availability of heavy, sour crudes from the Middle East. Brent’s premium over Dubai swaps has been holding at around USD 3/b, compared with less than 1/b at the start of the year. The wider spread likely reflects both higher volumes from OPEC+ producers in the coming months as well as some expectation that Iran will be able to export crude without restrictions in H2 2021.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

However, even if Iran were to increase output rapidly and on a similar scale to what the market witnessed in 2016 we don’t believe it would be enough to push headline crude balances into surplus. Demand expectations for H2 2021 are for a surge in consumption y/y, led by developed markets thanks to expansive Covid-19 vaccine programmes. We have noted previously that there are still substantial downside risks to demand given that many economies are still facing considerable public health challenges related to Covid-19, forcing lockdowns and mobility restrictions. But thanks to a solid erosion of the excess build in stocks in 2020 and a healthy demand outlook in some key consuming economies, oil markets are still pricing in considerable tightness for the second half of the year. Time spreads in the Brent market show a large backwardation of around USD 2/b in 1-6 month contracts.

.png)

Source: IEA, Emirates NBD Research

We would also expect OPEC+ members to push Iran to accept a production quota if sanctions are removed. Iran has not been part of the OPEC+ agreements as its ability to export has been restricted by sanctions. Some pushback from the Iranians would be likely, as they would seek to recapture lost market share, but pressure from other major OPEC+ producers to not overwhelm markets with additional production would be high.

Edward Bell

Edward Bell