Recent Search

Popular Searches

Oil prices managed to settle higher last week even as markets sagged at the end of the week in response to a stronger dollar. Brent futures closed up 2.5% at USD 44.40/b while WTI closed the week at USD 41.22/b, a gain of 2.4%. Brent prices had managed to hit USD 45/b mid-week, their highest level since March but current prices around USD 44/b for Brent represent a 50% retracement of the peak-to-trough move so far in 2020 and may be a substantial barrier if no further supportive fundamentals are forthcoming.

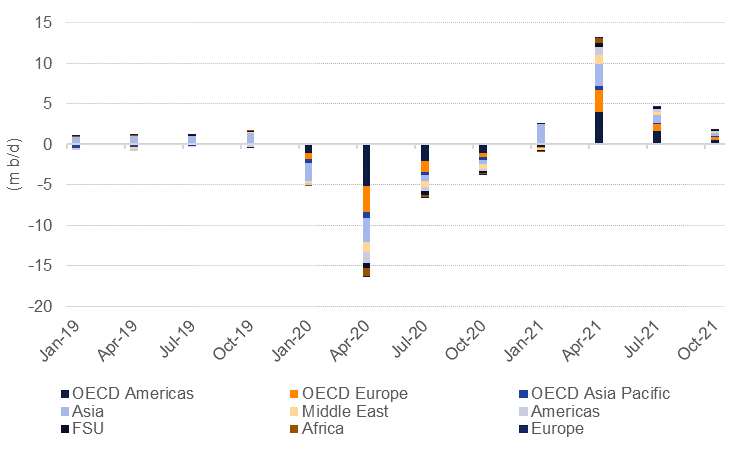

Markets will turn to OPEC, the IEA and EIA for their monthly assessments of oil market conditions this week. Of note will be the outlook for supply heading into 2021 and whether OPEC+ can maintain its schedule of tapering production cuts while other producers are out of the market. Last month the IEA revised its demand expectations for 2020 up by 400k b/d—but still anticipated a decline of almost 8m b/d y/y. The improvement in economic conditions across much of the developed world may prompt further upward revisions to demand forecasts for 2020.

In line with the expected increase in volumes from OPEC+ exporters, Saudi Aramco lowered its official selling prices to Asia and Europe. Refining margins—a key indicator to set regional OSPs—have recovered from hitting ytd lows in March but still remain well below year-ago levels. A 321 crack for Singapore product swaps based on Dubai crude closed at less than USD 3.50/b last week. The same spread was around USD 8/b at the start of the year. Saudi Aramco, however, kept pricing for the US unchanged. Making Saudi crude relatively more expensive for US refiners can help to deter imports and thus force a draw on crude stocks, creating a perception of tightening market balances even if shipments to other destinations remain unchanged or actually increase. US oil market data is the most regular, comprehensive and transparent and can thus exert a greater influence on market assessments of balances.

Time spreads showed relatively little change last week with contango structures remaining well entrenched in both the Brent and WTI markets. The Brent 1-6 month time spread settled at USD 1.67/b in contango, steeper than the USD 1.48/b a week earlier while in WTI the same spread closed modestly steeper at USD 1.54/b compared with USD 1.48/b five days earlier. Dubai swaps widened their contango to USD 0.58/b on 1-3 month spread, another contributor to lower OSPs from the GCC.

Source: IEA, Emirates NBD Research

Source: IEA, Emirates NBD Research

Edward Bell

Edward Bell