Recent Search

Popular Searches

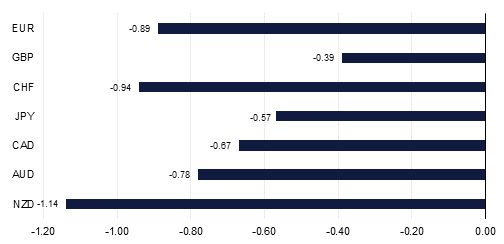

Markets have calmed down since their mini-correction at the start of the month, leaving the dollar a little bit firmer as well. Central banks last week continued to emphasize the gradual nature of policy normalization, with the Fed’s minutes interpreted as a little more hawkish, while the ECB gave few clues as to when asset purchases will come to an end. UK economic data was also softer than expected, introducing some doubt as to whether the Bank of England will go ahead and raise interest rates in May. March is building up to be a crucial month, with key central bank meetings due to be held in the US and the Eurozone, and with political risks in Europe also coming to a head. In the meantime this week the focus will be on new Fed Chair Jerome Powell’s first testimony to Congress.

The dollar’s firmer tone owes itself to a calming down in global markets in general, as well as to the appearance that the Fed will look through market volatility and continue to raise interest rates gradually. The minutes of the January FOMC meeting, the last one that Janet Yellen chaired, showed that the majority of FOMC participants felt that a stronger outlook for economic growth raised the likelihood that further gradual policy firming would be appropriate. The addition of ‘further’ in the accompanying policy statement was interpreted as slightly more ‘hawkish’, especially as the FOMC minutes pre-date the recent Congressional agreement to remove spending caps, which means that the overall fiscal stimulus could be even bigger over the next few years than was assumed at last month's FOMC meeting. The market implied probability of rate hikes in 2018 still remains at three hikes this year but has now increased from one to one and half for 2019.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

A subsequent monetary policy report (MPR) by the Federal Reserve released on Friday, which will serve as the basis for new Chairman Jerome Powell's congressional testimony on Tuesday, showed little difference with the last thoughts of the Yellen Fed. The report said that activity increased at a solid pace over H2 2017 and that the labour market continued to strengthen. It also mentioned that inflation has remained below target, and added that despite the tight labor market wage growth has been moderate, in part held down by low productivity growth. One thing that stood out was a warning of "elevated valuation pressures across a range of assets even after accounting for the corporate tax cut and current Treasury yields." However, the Fed seems confident in the financial system overall, and in its position to deal with any possible shocks.