Recent Search

Popular Searches

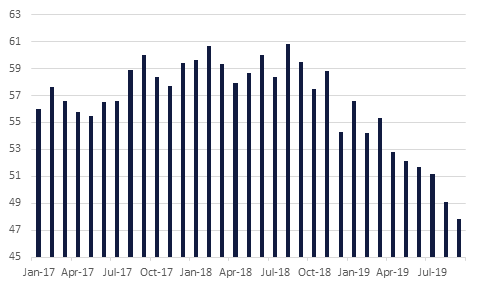

There was bad news from the manufacturing sectors of the world’s major economies yesterday. Most strikingly in the U.S. was the slump in the US manufacturing ISM index to a decade low 47.8 from 49.1 in August, perhaps providing more signs of an looming recession. The weakness may have had something to do with the strike underway at General Motors, but it also still speaks of a broader malaise and a sector under significant stress. From standing at 59.5 a year ago the index has plummeted more or less consistently over the twelve months, with most compnenents from employment to new orders, export orders and prices paid in contraction, and with inventories the only component in positive territory.

The final Eurozone manufacturing PMI was 45.7 in September up slightly from the first estimate of 45.6, but still bad news nonetheless. In Germany the index stood at 41.7 down from 43.5 in August and very clearly in recession territory. Separately headline inflation slipped to 0.9|% in the eurozone while the core rate nudged up to 1.0%. The UK manufacturing PMI rose to 48.3 in September from a 6 ½ year low of 47.4 in Augusty. The indicator is still highlighting a sector in contraction, with new orders, output and employment all showing fresh declines. The weakest part of the survey was investment goods, reflecting a reluctance by businesses to make new capital spending, presumably because of Brexit, along with slowing headwinds in the Eurozone and more globally.

The Reserve Bank of Australia (RBA) cut interest rates at their October meeting yesterday lowering the Cash Rate Target by 25bps to a new record low of 0.75%. In addition to this rate cut, the language took a dovish tone with the RBA indictating a further willingness to lower the rate to support growth. With concerns over subdued wage growth, low inflation and international headwinds, the market expects further action from the RBA and the OIS is currently implying a 56.6% chance of an additional rate cut before the end of the year.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

Yields on benchmark government bonds closed lower as markets digested more disappointing data out of the US. Yields on 10yr USTs declined nearly 3bps to settle at 1.64% while gilts and bunds also pushed lower.

The president of the Chicago Fed, Charles Evans, said the Federal Reserve was in a position where it could raise rates over the coming years if the US economy shows signs of improvement.

The dollar lost ground yesterday as a 10-year low in the U.S. manufacturing ISM knocked it back causing a broad sell-off as Fed rate cut hopes were raised, amidst pressure on equities and yields. EURUSD rallied to 1.0950 from 1.0885 lows, while USDJPY slid to 107.65 from 108.45. Cable was more mixed on reports the EU would consider a time-limited Irish backstop, taking the Pound momentarily to 1.2338, before falling back to 1.2260 lows.

Global equity had a negative performance across the board yesterday. In the U.S, the S&P500 finished the day 1.23% lower, while the Nasdaq posted a loss of 1.13%. Their Eurozone counterparts did not fare any better and the DAX lost 1.32% while the Euro Stoxx fell by 1.43%. Regional markets were more mixed and while the Muscat gained 0.5%, the DFM and ADX both declined by 0.1% and the Tadawul finisghed 0.5% lower.

This morning, Asian equity markets have opened to a soft performance and as we go to print, the Nikkei is trading 0.48% lower, while the Shanghai Composite is down by 0.92%.

Oil prices fell as disappointing US data weighed on demand expectations. A roll-over of the Brent contract saw it open at much weaker levels and prices for the international grade are now trading below USD 60/b. WTI closed at USD 53.62/b overnight even as the API reported a draw in US inventories of around 6m bbl of crude.

Ecuador has announced plans to quit OPEC as of 2020. The country produces around 550k b/d but has struggled to adhere to its OPEC+ production cut target and it will now seek to maximize production and income.