Recent Search

Popular Searches

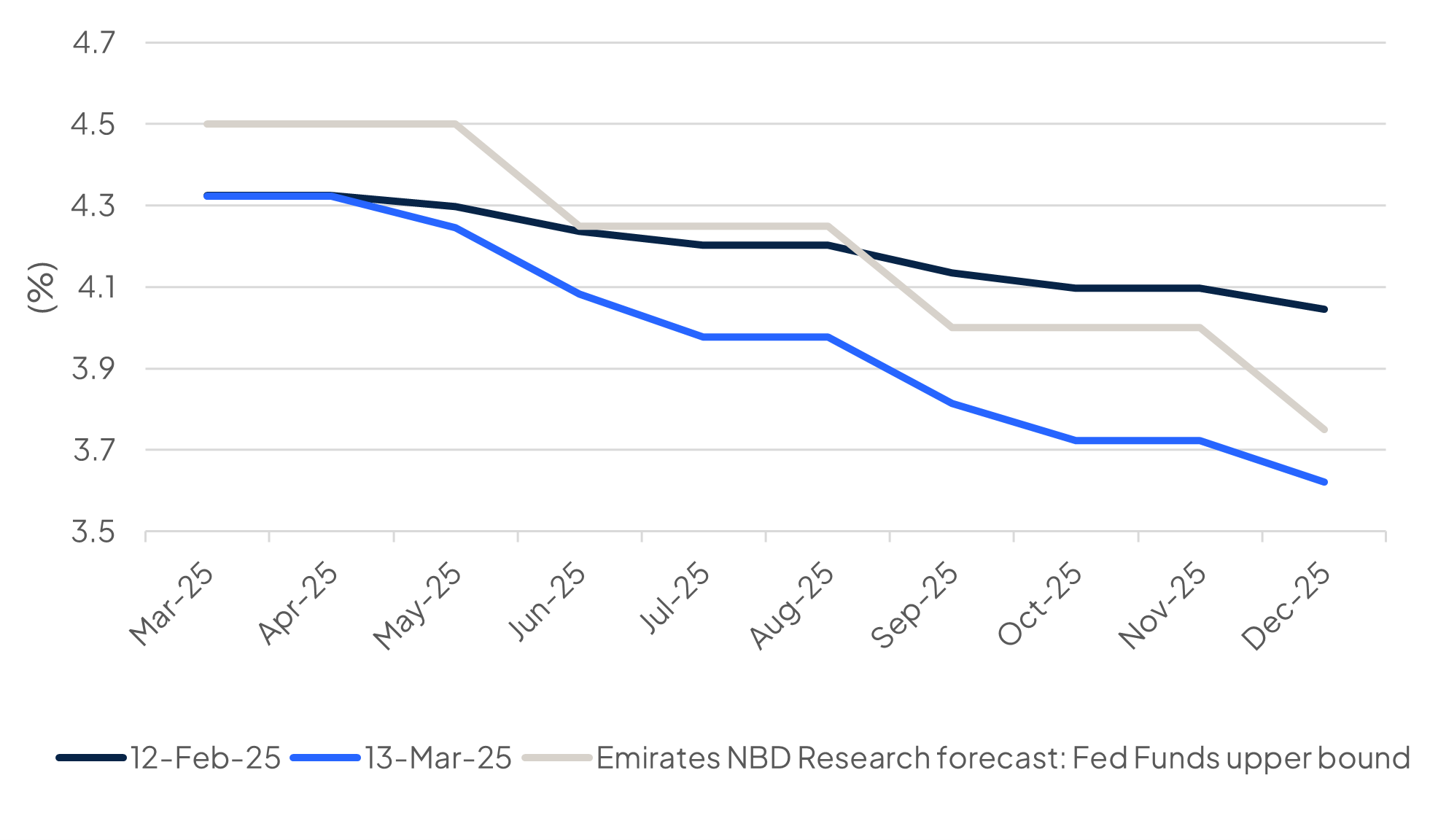

We expect the Federal Reserve to hold policy unchanged at its March 18-19 FOMC meeting, a shift from our previous call of a 25bps rate cut in Q1. The scale of uncertainty facing the Fed favours taking a cautious and moderate pace in adjusting policy and we now expect that rate cuts will come only later this year.

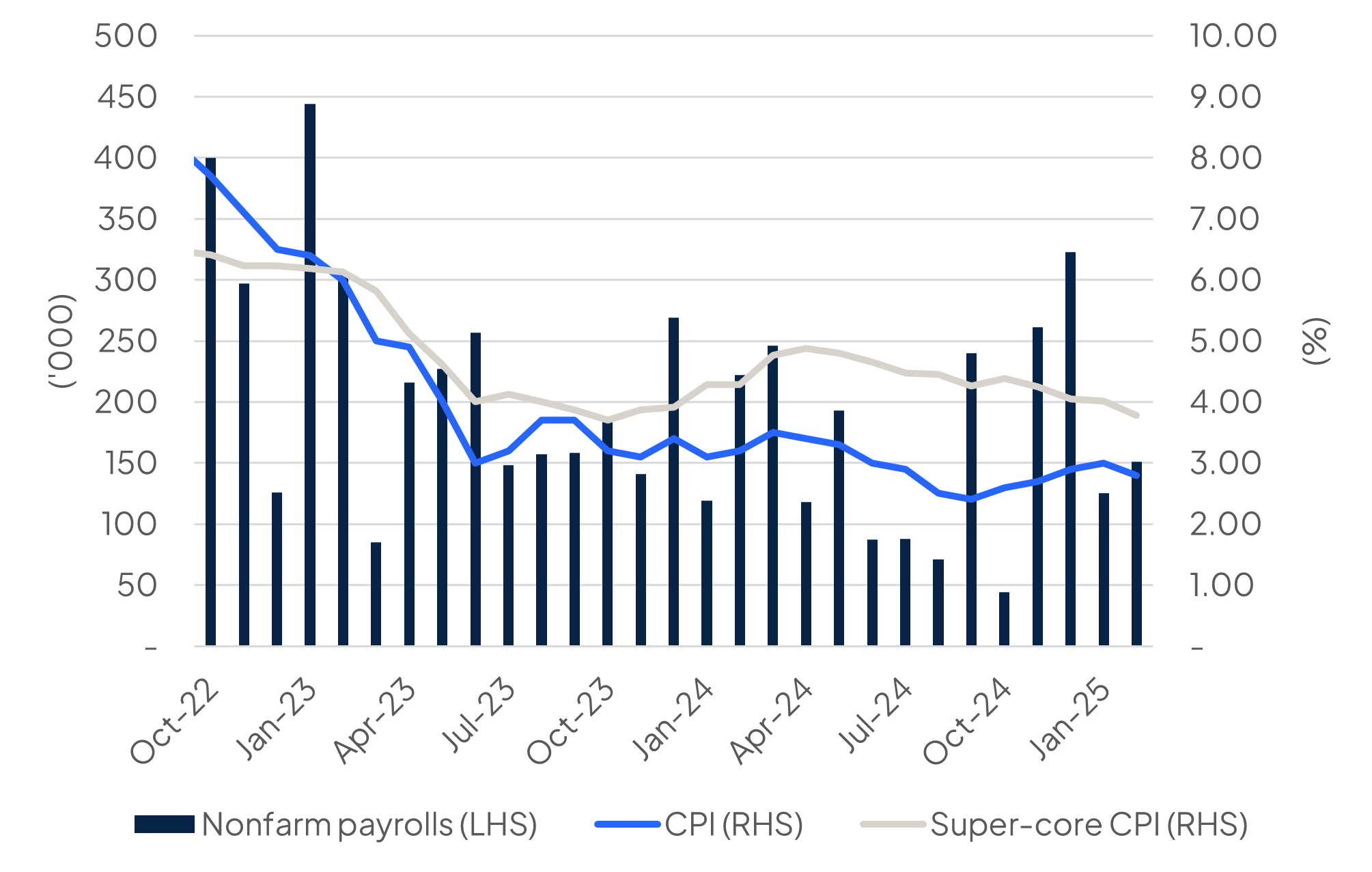

Macro signals from the US economy suggest that the Federal Reserve still has a clear path to cutting rates at a steady pace. Overall activity is moderating but remains positive. Employment data for January and February highlights a labour market still in good shape: the unemployment rate is holding around 4% and the three-month average of jobs growth is close to 200k as of February, down from Dec-Jan levels but higher than most months in 2024.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

Inflation also eased in February to 2.8% y/y on the headline CPI index, down from 3% in January. On a monthly basis, the CPI index rose by 0.2% in February, its lowest level since October last year, while super-core CPI that strips out volatile measures of food and energy as well as housing rose by less than 4% y/y for the first time since December 2023.

Activity data has also been holding up well with the ISM services and manufacturing PMIs recording decent, if not blistering, levels for the start of the year. But that’s where the good news for the Fed starts to dissipate.

Despite the improvement in the latest headline CPI print, there were some negative signals buried in the details. Airline fares were a drag on the index for the first time in six months while other signals of discretionary spending—sporting goods for instance—exerted a larger negative pull on CPI than they did for much of 2024. Core goods are showing far less of a downward pull that they did in 2024 and February only had the impact of the initial 10% tariffs on imports of Chinese goods. Subsequent inflation prints, including producer price inflation expected at 3.3% for February, may reflect more and more of the tariff effect on imported goods.

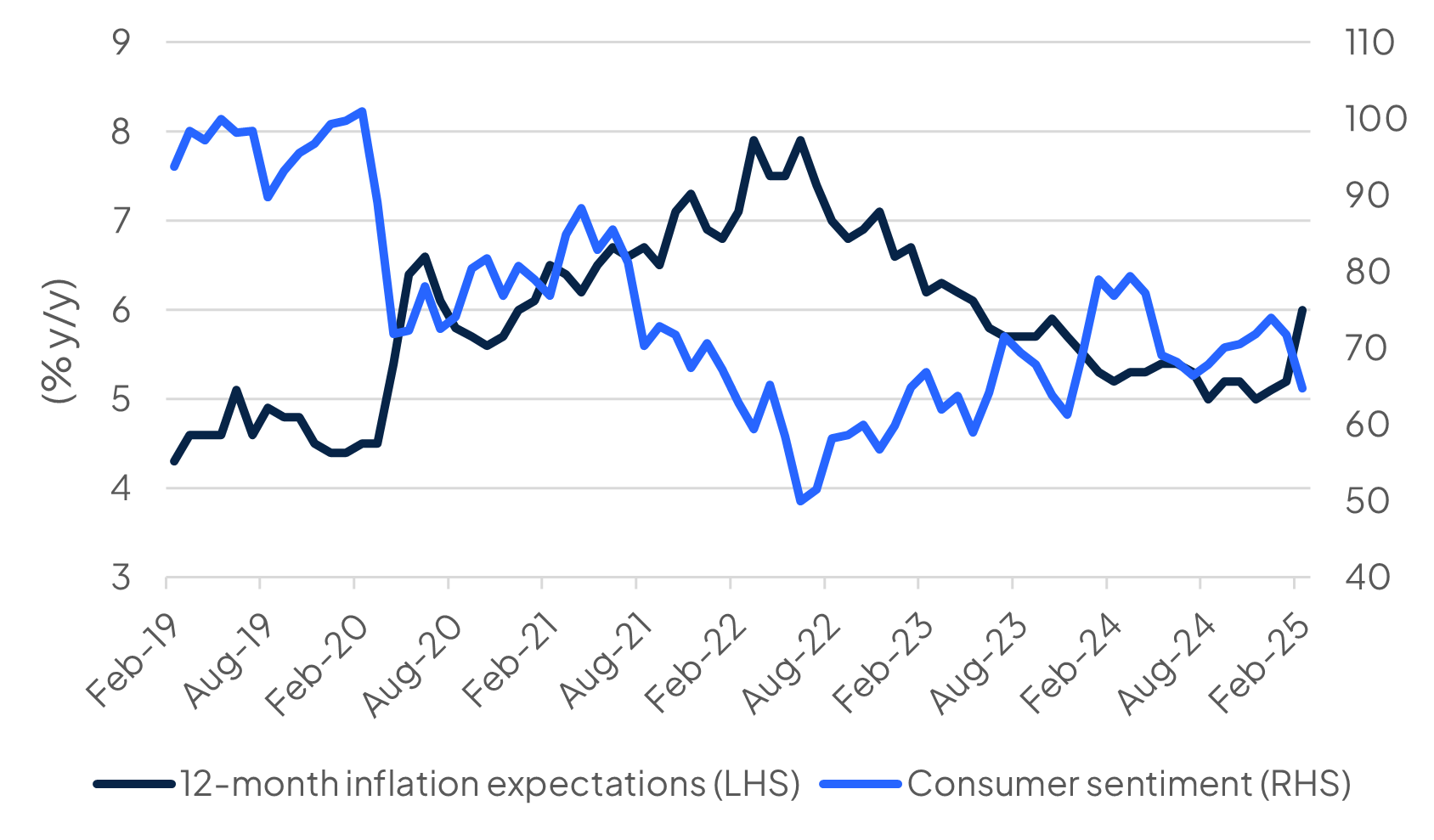

After an initial post-election bounce consumer sentiment has started to weaken. The University of Michigan’s consuerment sentiment survey dropped to 64.7 for February, its lowest level since November 2023. At the same time inflation expectations have reversed their downward pull as consumers fear a rise in the cost of goods.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

The consistency of the Trump administration’s policy is also a major challenge for the Fed to have to navigate. Tariffs of 25% were enacted on March 4 on goods from Mexico and Canada only to be watered down on March 6 to goods falling outside the conditions of the USMCA—a free trade deal signed between the three North American economies during President Trump’s first administration.

The Fed is currently in its black-out period ahead of the March FOMC meeting but commentary ahead of the event suggested there was still a bias to easing, if at much slower pace. Christopher Waller, a Fed governor, said on March 6 he still saw the chance of two or three rate cuts this year though ruled out a move at the March FOMC. Waller also was more sanguine about the effect tariffs would have on inflation and that if the “labor market, everything, seems to be holding, then you can just keep an eye on inflation.”

In comments after the February employment report Fed Chair Jerome Powell said that the US economy was “in good shape” but reiterated that the Fed wasn’t in a “hurry” to cut rates.

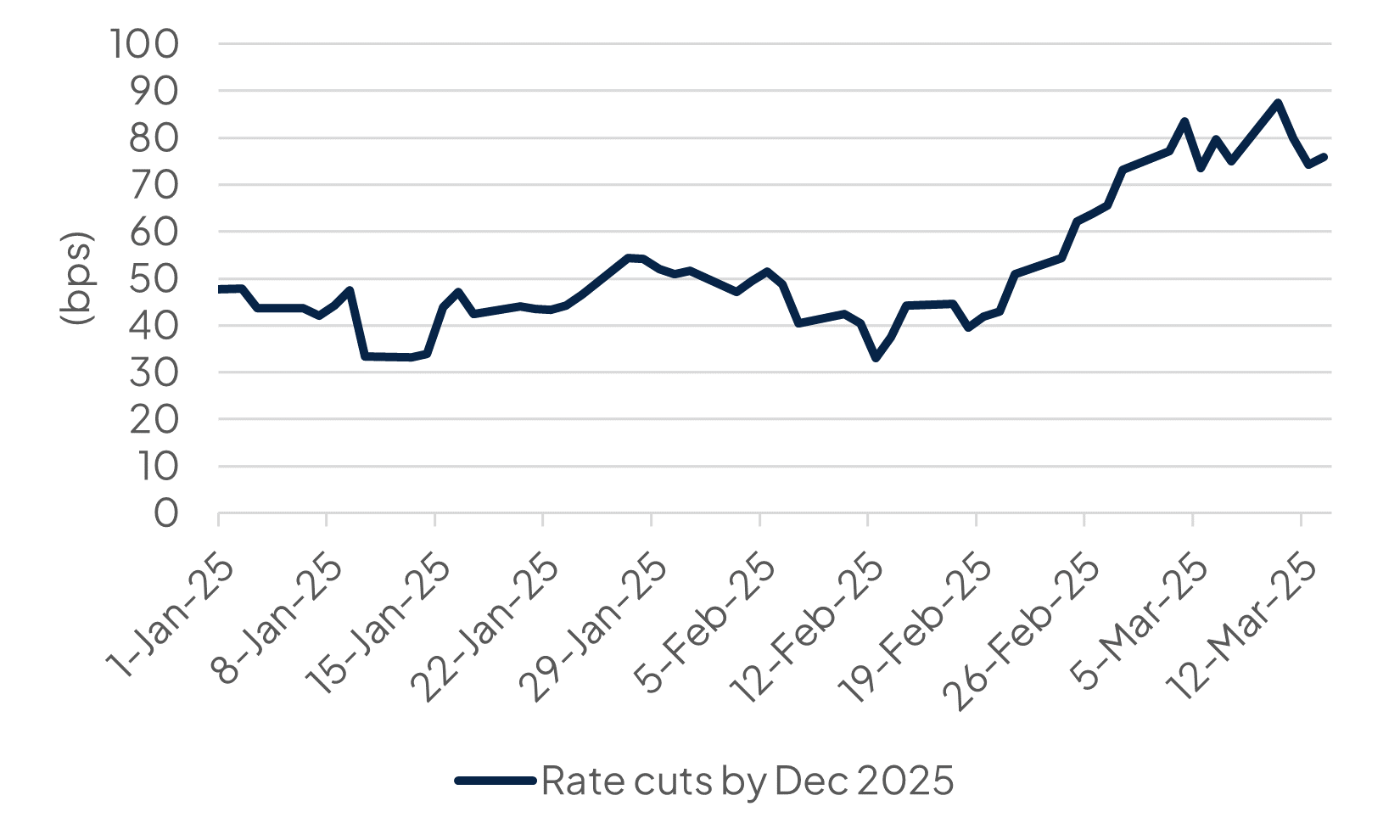

Markets have grown much more downbeat on the outlook for the US economy in recent days, abetted by President Trump not ruling out a potential recession. Rate expectations have shifted to 75bps of easing by the end of the year as of March 13 from a low of just 33bps—barely more than one 25bps cut—as recently as mid-February.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

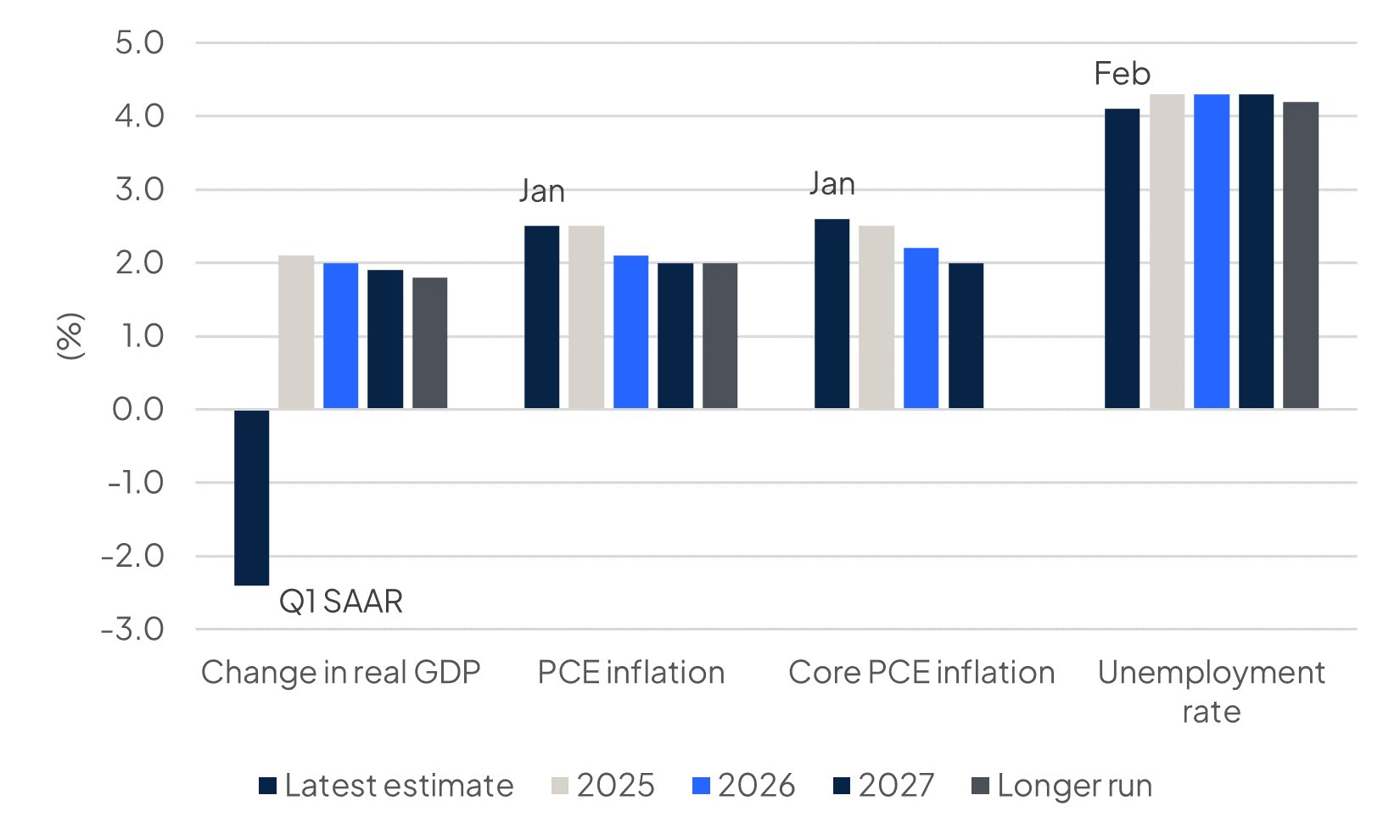

The Fed will release its summary of economic projections at the March FOMC and any sign of a more downbeat stance on growth is likely to be seized upon by markets that are already captivated by a recession risk for the US economy.

Source: FOMC, Atlanta Fed, Emirates NBD Research

Source: FOMC, Atlanta Fed, Emirates NBD Research

Our expectation is that the Fed will continue to be driven by the data rather than anticipate the outcome of unclear policies. By the June FOMC meeting the Fed will have three more CPI and PCE data points to digest to assess the impact tariffs, if they are indeed maintained, are having on inflation and employment. We are shifting our view to a first 25bps rate cut from the Fed this year to the June meeting and then following with one per quarter in Q3 and Q4 2025.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.Click here to download the full report

Edward Bell

Edward Bell