Recent Search

Popular Searches

.jpg?la=en&h=668&w=1000&hash=B61F59DF5F2AF03FE42ED9EF0C508EB1)

The Coronavirus has been dominating headlines, with concerns over its potential effect on global demand contributing to a fall in oil prices and other commodities, luxury brands, and equity markets more generally, especially in Asia. Chinese authorities have put travel restrictions in place, and have extended the New Year holidays; financial markets are likely to remain closed for the time being. Aside from the human cost, the outbreak will likely weigh on Chinese real GDP growth this year, which was already expected to come in under 6.0% for the first time in decades. This will also weigh on the global growth outlook.

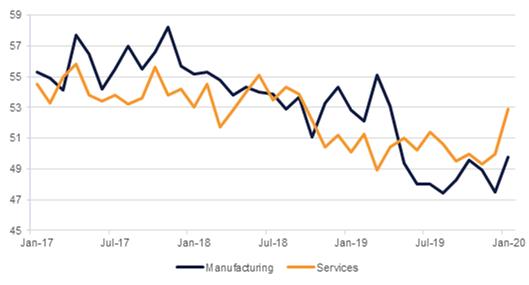

The UK posted stronger-than-expected PMI numbers on Friday, significantly diminishing the likelihood of a rate cut by the Bank of England when its MPC convenes later this week. Although the manufacturing PMI was still in contractionary sub-50.0 territory, its 49.8 was the strongest reading since April 2019, and exceeded consensus expectations of 48.8. Services also exceeded expectations at 52.9 compared to 51.1, contributing to a composite reading of 52.4 – the strongest expansion since September 2018. The market-implied probability of a rate cut this week has fallen to just 46.4%, compared to over 70% a week ago.

By contrast to the UK, the Eurozone composite PMI (also released Friday) undershot expectations, at 50.9 compared to 51.2. However, while the manufacturing component remained negative, its 47.8 was markedly stronger than the consensus projection of 46.8, or indeed December’s reading of 46.3. Services on the other hand missed expectations, though at 52.2 remained in expansionary territory. The unexpected uptick in the manufacturing index came in the wake of the ECB’s meeting on Thursday, and give credence to the more upbeat statement by President Christine Lagarde that the ‘risks surrounding the euro area growth outlook… have become less pronounced.’ This is moderately stronger language than seen in December, when the risks were judged ‘somewhat less pronounced.’ The deposit facility rate was left unchanged at -0.5%.

Source:Bloomberg, NBD Research

Source:Bloomberg, NBD Research

Treasuries closed higher last week as risk-off trade gathered pace. The current bout of uncertainty stems from concerns over global growth following the outbreak of the Coronavirus. The longer maturity debt dominated the flows which in turn flattened the yield curve. Yields on the 2y UST and 10y UST ended the week at 1.49% (-6 bps w-o-w) and 1.68% (-14 bps w-o-w) respectively.

The move past week has allowed USTs to build onto their 6.9% gain in 2019. The Bloomberg Barclays US Treasury index has gained +1.2% so far in 2020.

The expectation of a rate cut from the Bank of England at this week’s meeting pared back last week following strong economic data. Traders are currently pricing in a 46% probability of a rate cut, down from 73% at the beginning of last week. Yields on the 10y Gilts ended the week at 0.56% (-7 bps w-o-w).

Regional bonds continued to drift higher. However, the gain was marginal compared to sharp moves in benchmark yields. The YTW on Bloomberg Barclays GCC Credit and High Yield index dropped -1 bp w-o-w to 3.10% and credit spreads widened 11 bps w-o-w to 148 bps.

With the Bank of England decision this week hanging in the balance, GBP is on a knife-edge, strengthening or weakening as the likelihood of a cut ebbs and flows. As we go to print, the market is currently pricing in a 54.8% chance of a 25bps rate cut from the MPC.

After strengthening to 1.3162 in intraday trading in the wake of the PMI data on Friday (see macro), it has fallen back to 1.3058 in early trading Monday. A cut by the BoE would take the price back below 1.3000. The present level sits at the 50-day moving average (1.3058), which has thus far provided support. Should this level falter, a retest of the 61.8% one-year Fibonacci retracement of 1.2920 cannot be ruled out. On the other hand, should the Bank of England decide to keep interest rates on hold, we could see a relief rally for GBPUSD back to the towards 1.32.

Regional equities closed lower following weak global cues over the weekend. The DFM index and the KWSE PM index dropped -0.6% and -0.5% respectively. Banking sector stocks, which led the rally last week, saw profit booking. Dubai Islamic Bank and First Abu Dhabi Bank lost -1.4% and -0.6% respectively.

Oil prices continued their steady drift lower last week as demand concerns increase on fears the coronavirus outbreak will threaten China’s economy, particularly affecting segments that would boost demand for jet and gasoline. Brent futures closed 6.4% lower on the week at USD 60.69/b while WTI gave up 7.4% to settle at USD 54.19/b. Brent has now lost more than 8% year-to-date while WTI is down nearly 11% before even the end of January. For reference our forecasts for average prices in Q1 is Brent at USD 58/b and WTI at USD 55/b. While average prices so far are still above our targets, they are converging consistently as weaker fundamentals drag prices lower.

Daniel Richards

Daniel Richards