Recent Search

Popular Searches

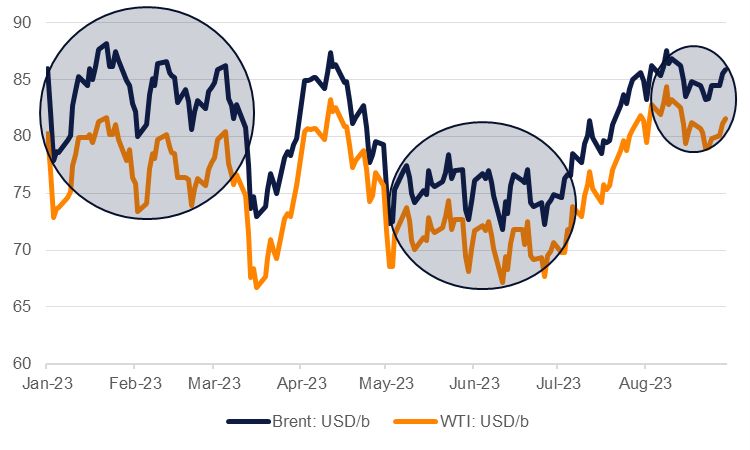

Oil markets look to have entered a new trading band, the third time they have been stuck in a range so far this year. Brent futures gained strongly in July, up 14% month/month and their strongest monthly gain since January 2022, as markets came around to understanding that OPEC+ and Saudi Arabia in particular were committed to setting a floor under prices. Since then prices have generally traded sideways: Brent futures hit a peak on August 10 of USD 88/b then pulled lower over the next few weeks to a monthly low of USD 82.33/b on August 23.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

The pattern looks roughly similar to what markets experienced in January to mid-March when Brent was stuck between USD 80-88/b and from May until June when prices hovered either side of USD 75/b. On the bullish side, factors keeping a floor under prices appear to be a strong pull lower in visible inventories—US commercial crude stocks have dropped by almost 48m bbl from a year-to-date peak in March—along with OPEC+ extending and deepening their production cuts, amplified by large voluntary cuts from Saudi Arabia.

The barriers to prices pushing higher are a little more imprecise but nevertheless powerful. China’s oil market fundamentals have sent strong signals so far this year—we estimate apparent demand was 21% higher in July compared with the same month in 2022—but the slow-motion unravelling of China’s property sector and potential risks to financial stability that could arise are fueling substantial negative sentiment toward the country. Sluggish or outright contracting industry data—the official manufacturing PMI has been below 50 since April 2023—are compounding the fear that a property crisis could derail China’s near-term economic outlook.

Beyond China, market uncertainty on the trajectory for developed market central bank policy will also lurch risk assets—including commodities—back and forth. We expect the Federal Reserve in the US has brought its hiking cycle to an end and the European Central Bank and Bank of England are not far off either. But with inflation still running hot in some economies and data showing an orderly slowdown in the US, markets will remain on edge that rates could potentially tilt even higher.

In the oil market specifically, Iran expects to increase its oil production to 3.4m b/d by the “end of summer” according to press reports quoting oil minister Javad Owji. Iran is not participating in OPEC+ production targets though US sanctions on Iranian oil exports have kept output levels below Iran’s JPCOA-era levels and its capacity of around 3.8m b/d. Iranian oil production had risen to 3.04m b/d as of July, according to IEA estimates, up from 2.66m b/d in December 2022 and less than 2.5m b/d a year earlier.

Source: Bloomberg, Emirates NBD Research. Note: managed money net length.

Source: Bloomberg, Emirates NBD Research. Note: managed money net length.

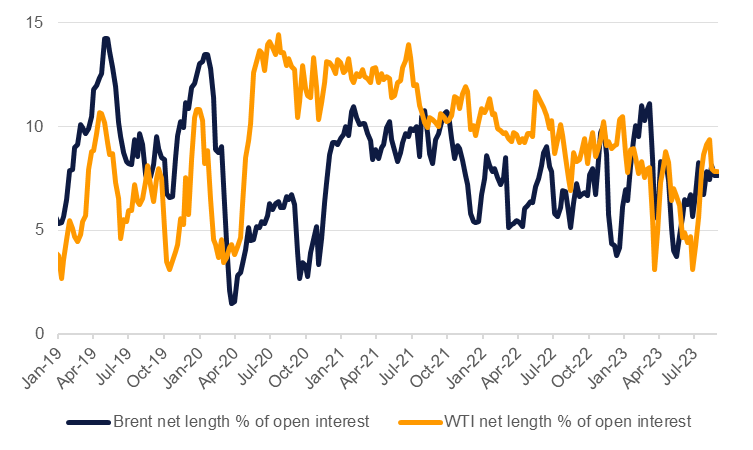

Options markets pricing in both Brent and WTI is also signalling a neutral outlook for spot prices. Risk reversals in both contracts have faded some of the downside risk that they showed during April and are far off the bullish skew displayed at the end of Q1 2022 when Russia began its invasion of Ukraine. Investors seem split on their outlook for Brent vs WTI with net length in Brent futures and options expanding so far in August by 21k contracts as of August 22 while WTI net length has fallen by 30k contracts over the same period. A recent pull higher in US oil production while OPEC+ holds back on output may be behind the split positioning.

Edward Bell

Edward Bell