Recent Search

Popular Searches

Saudi Arabia’s budget deficit widened sharply in Q2 to SAR 109.2bn as both oil and non-oil revenues declined. Oil revenue was down -45% y/y as both oil prices and the volume of production declined. Non-oil revenue fell -55% as a result of the impact of coronavirus restrictions on tax and fee income. The government cut spending -17% y/y in Q2, with capital spending bearing the brunt of the cuts. We expect the budget deficit to widen to -13.7% of GDP this year from -4.5% in 2019.

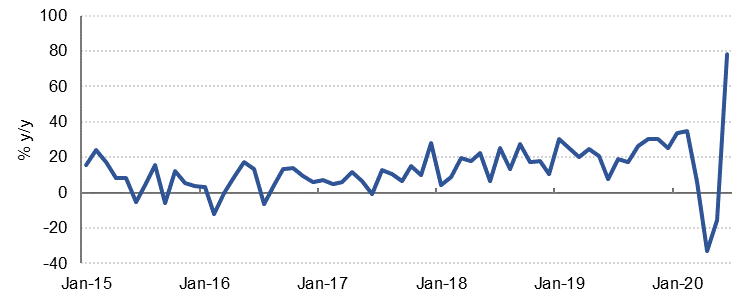

Data from SAMA showed money supply growth slowed to 9.0% y/y in June from 10.2% in May, while private sector credit growth accelerated to 13.2% y/y from 11.0% in May. Net foreign assets declined slightly to USD 443bn last month. Point of sale transactions surged 78.3% y/y in June as consumers likely brought forward purchases ahead of the increase in VAT from 1 July.

Negotiations between Republicans, Democrats and the White House failed to yield agreement on a new package of stimulus measures yesterday, and some Republican senators became increasingly vocal about their opposition to even the USD 1tn additional support proposed by their own party. A new deal is unlikely to be agreed before the current USD 600/week unemployment insurance expires this week. Meanwhile US consumer confidence fell by more than expected in July to 92.6 from 98.3 in June. The present situation component improved but the expectations index declined sharply to 91.5 from 106.1 in June. The survey suggests that consumption growth is likely to have slowed in recent weeks.

Separately the Fed extended its emergency lending programs by three months to the end of 2020 ahead of its two-day meeting which will conclude later today. The FOMC is not expected to make any significant changes to monetary policy, but may start to provide more clarity on its forward guidance, perhaps by linking interest rates more explicitly with economic variablies such as inflation or unemployment.

In the UAE, local press reports that property developer Nakheel has approached banks to refinance some outstanding debt. No further details on the amount of debt that might be restructured were provided.

Source: Haver Analytics, Emirates NBD Research

Source: Haver Analytics, Emirates NBD Research

Fixed Income

US treasuries rallied ahead of the Fed’s decision. Yields on the 2yr UST fell slightly more than 1bp to below 0.14% while yields on the 10yr UST sank almost 4bps to settle at 0.579%. Market focus will be on whether the Fed outlines a plan to link rate moves directly to economic targets—either inflation hitting the 2% target or unemployment hitting a set level—and whether the Fed is still interested in pursuing a yield cap strategy.

Bond markets generally were supported overnight with gains across corporate and high-yield markets too. EM bonds held roughly flat with most issuances taking place in local currencies.

FX

The dollar was largely unchanged on Tuesday. The DXY index remains around the 93.65-93.70 region, treading water ahead of the Fed’s announcements later tonight. USDJPY moved lower, falling below the 38.2% one-year Fibonacci retracement at 105.13, a loss of just over -0.20%. USDJPY continues to test the 105 level which has been a barrier in previous cycles where the yen has strengthened.

The euro lost some of its recent vigour but remains in a comfortable position above the 1.17 handle at 1.1730. Sterling continues to hover just below the 1.30 mark at 1.2930 range. The 76.4% one-year Fibonacci retracement of 1.3018 may offer some resistance for the currency. The AUD remains in positive form at 0.7168 whilst the NZD fell by over -0.40% to trade at 0.6655.

Equities

Equity indices in developed markets sold off moderately yesterday, as investors waited to see the outcome of the FOMC meeting and renewed stimulus in the US. The S&P 500 lost 0.7% and the Dow 0.8%, while in Europe the CAC closed down 0.2% and the DAX was flat. The UK somewhat bucked the trend, with the FTSE 100 gaining 0.4%, driven by homebuilders on the expectation that the government’s help to buy scheme will be extended.

Regional equities were positive yesterday, with the DFM closing up 0.2%, and the Tadawul gaining 0.5%..

Commodities

Oil prices are oscillating as the market awaits the outcome of negotiations over additional fiscal stimulus in the US and more clarity on rates policy from the Federal Reserve. Prices slipped overnight with Brent down by 0.4% and WTI off by 1.4% but both are holding steady in trading today with Brent futures at USD 43.33/b and WTI a little more than USD 41/b.

The API reported a 6.8m bbl draw in crude inventories last week while products rose. Markets may need to prepare for an unseasonal build in gasoline inventories as traditional holiday spots in the US appear to be the centres of the coronavirus resurgence that is underway.

Daniel Richards

Daniel Richards