Recent Search

Popular Searches

Despite the reimposition of lockdown restrictions in the fourth quarter of 2020, real GDP growth in developed markets largely exceeded expectations, indicating that economies are getting better with coping with the stresses induced by the Covid-19 pandemic crisis. This improving resilience could soften its impact on the current quarter also, although with Q1 lockdowns deeper and longer, the likelihood remains that the period will be quite weak. Looking ahead, the speed with which governments implement vaccination programmes will be a principal determinant of the pace of growth, with the UK and the US leading in this regard among the major economies. More generally, the seven-day moving average of new Covid-19 case numbers globally has fallen to 364,000, compared to the November peak of 806,000, offering hope for a post-pandemic normalisation.

.jpg) Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

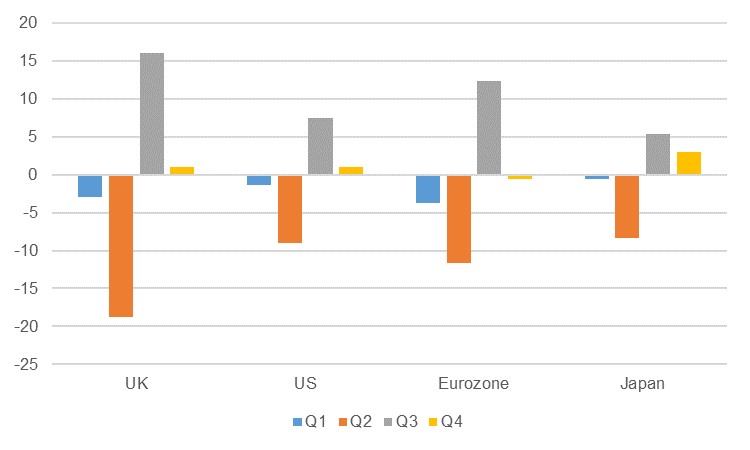

With DM growth figures for the fourth quarter now in, the results were largely better than had been anticipated, even as governments put in place new restrictions on movement in the period in order to curb second waves of the virus. In Japan, q/q growth came in at 3.0%, compared to projections of 2.4%, while the economy contracted by -4.8% in 2020 as a whole, beating the IMF’s October projection of -5.3%. The UK managed to avoid a double-dip recession with an expansion of 1.0% q/q. This beat consensus projections of 0.5%, but the 2020 -9.9% contraction was the largest since 1709. Meanwhile the Eurozone did contract -0.6% q/q, but this was a shallower contraction than the predicted -1.0%. The one outlier was the US, which with an annualised q/q growth rate of 4.0% came in a little shy of the anticipated 4.2%. For a more direct comparison, the US saw non-annualised q/q growth of 1.0% in Q4.

These results compare favourably to the double-digit contractions recorded in Q2 2020, as the pandemic crisis really started to impact economies around the world. While the restrictions imposed in Q4 were in large part not quite so onerous as those earlier in the year, this is mitigated to an extent by the fact that the number of new daily cases was much higher, which leads to a degree of self-imposed restrictions. The stronger-than-expected performances likely also stems from the fact that economies have gotten better at coping with the restrictions, with the infrastructure for effective homeworking now firmly in place for many businesses, and supply chains reinforced.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

The economic resilience demonstrated in Q4 bodes well for the current quarter, although diminished economic output is likely to be the norm across most of DM barring the US once more. With less severe restrictions in place than its counterparts, and rapidly falling case numbers, the US is likely to be the outperformer in Q1, a view reinforced by timely data for the period so far. While labour market data has remained weak, with only a net increase of 49,000 in non-farm payrolls in January and weekly initial jobless claims still some four times the pre-pandemic norm, other indicators have been robust. Both the services and manufacturing PMIs remained firmly in expansion territory in February at 58.9 and 58.5 respectively, industrial production rose 1.0% m/m in January, and retail sales grew 5.3% in January, far exceeding predictions of 1.1%.

Source: Bloomberg, Emirates NBD Research

In Europe, where the Q1 lockdowns have been more severe, the outlook for the period is less positive. In the UK, retail sales shrank -8.8% m/m in January, in sharp contrast to the expansion in the US. The February PMI surveys showed an expansionary manufacturing sector (54.9) but services, the bulk of the UK economy, remained contractionary at 49.7, albeit an improvement from the January reading of 39.5. Likewise in the Eurozone, manufacturing managed to expand comparatively strongly (57.7), while services (44.7) floundered. Japan’s lockdowns are generally far looser than those seen elsewhere – bars and restaurants are still open, but must shut by 8pm – but the services PMI still fell to a six-month low of 45.8 in February.

This disparity between services and manufacturing will remain until restrictions begin to be eased, but with differing levels of success on vaccination rollouts, there could be a two-speed recovery in Western Europe over the coming months. In the UK, the rollout has been one of the swiftest in the world, which combined with the lockdown have led daily case numbers to drop below 10,000 for the first time since October and for the government to start laying out a timetable for a gradual normalisation from mid-March onwards. Bank of England Chief Economist Andy Haldane has said that UK households have amassed some GBP 250bn in ‘accidental savings’, making the economy a ‘coiled spring’ waiting to burst. By contrast, the Eurozone’s vaccination rollout has been beset by difficulties, and with cases rising once again in the bloc’s powerhouse of Germany and elsewhere, any normalisation will likely be a longer time coming. As the summer approaches this will be especially concerning for those southern European countries reliant on tourism.

The US has already been a comparative outperformer in terms of growth so far, despite the hit to the labour market and the very high Covid-19 caseload, and both of these pressures are likely to ease in the coming months, providing a further fillip to growth. While the jobs data has remained weak, the apparent determination by President Joe Biden to push through increased stimulus to the tune of USD 1.9tn should support household spending. Meanwhile, new case numbers have fallen to under 50,000 each day, compared to over 200,000 a day at their peak, enabling total utilisation to climb to 75.6%, the highest level since February. Consensus forecast is for 4.9% growth in 2021, but with the president’s spending plans the risk to this is to the upside. With the far shallower contraction in 2020 also (-3.5%), the headline impact to the US economy has been far less than seen elsewhere.

Daniel Richards

Daniel Richards