Recent Search

Popular Searches

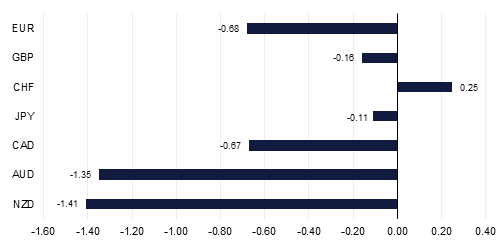

On Friday the USD managed to recoup some of the losses it experienced during the early part of last week, even though stock markets remain fragile and bond yields are still soft. At the forefront of USD strength remains GBPUSD, which continues to be weighed on by Brexit and the possibility of a no-deal outcome. Despite its relative weakness, and the EU and the UK having reached an agreement today at their extraordinary summit in Brussels, we doubt if the markets have fully discounted the possibility that it won’t be passed through Parliament in December. As this more important deadline approaches the likelihood is that GBP will lose further ground, with the risk of greater capitulation once the outcome is actually known.

Geopolitics will dominate in other respects this week as well, with the G20 meeting at the end of it being the main focal point. We would not be surprised if a trade agreement of sorts is agreed in principle between the US and China, giving some heart to markets, but the detail may not be as positive as the headlines suggest and any euphoria may well be short lived. Once again, sentiment may receive a short term boost, but whether it can be sustained will be the more meaningful question and test.

Attention on oil markets will also be prominent given the heavy losses experienced last week. President Trump may think he is succeeding in manipulating the price lower, but the real test will come with the OPEC meeting in early December, as OPEC interests are broader and not necessarily as aligned as the US President might think. Rather than delivering a consistently lower oil price, President Trump may actually be paving the way for greater volatility.

Markets may also be looking for silver linings in Fed statements over the course of the week, hoping for hints of a more dovish tone ahead of the December FOMC meeting. Both Fed Chair Jerome Powell and Vice Chair Richard Clarida are due to speak this week, but they are unlikely to give much away regarding the Fed’s intentions. Again the markets may see what they want to believe in the short term, but reality is only likely to come into view in December, a bit like with Brexit, with oil and over trade.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg