Recent Search

Popular Searches

Donald Trump raised the ante on China again at the end of last week, threatening tariffs on a further USD267bn of Chinese imports after saying that a package of tariffs was already close to being imposed on USD200bn worth of Chinese goods. This news is likely to continue to pressure markets in the coming week after falls across the board last week. Furthermore the strength of the US jobs report pushed the dollar and Treasury yields higher as the perception of two more Fed rate hikes this year was maintained. Non-farm payrolls rose 201k in August, with the unemployment rate steady at 3.9%, but average hourly earnings rose by 0.4% m/m taking the y/y rate up to 2.9% the strongest since 2009.

Markets will remain sensitive to all of these factors in coming days, with central bank meetings also occurring in the Eurozone, the UK and Turkey. The biggest uncertainty will be what the Turkish central bank will decide following the recent increase in inflation and the ongoing pressure on the lira. The ECB and the BOE by contrast are unlikely to result in any changes. In the US CPI inflation data and retail sales will be the highlights, while Brexit negotiations will also return as central for GBP. EM will continue in the spotlight in view of the strength of the USD and expectation of higher US rates, with 96% chance of a September Fed move priced in and 67% chance of a second one in December.

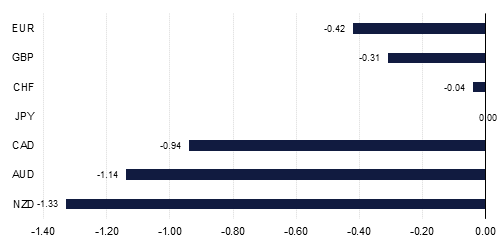

Source: Emirates NBD Research

Source: Emirates NBD Research