Recent Search

Popular Searches

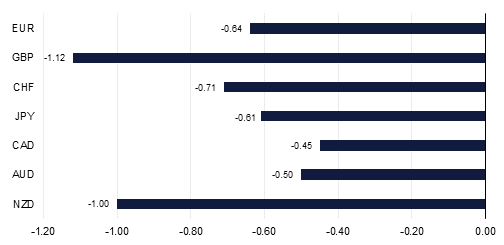

Markets are approaching the end of the year with considerable anxiety amidst ongoing trade tensions, Brexit uncertainties, slowing Chinese growth, and political volatility in the US and in Europe. The dollar is firmer than a week ago reflecting the larger uncertainties elsewhere, while Wall Street and bond yields in the US remain heavy and the Trump White House faces its own problems, with the risk of partial government shutdown at the end of the year. Thinning liquidity is also a potential issue that could see outsized responses to headlines, fanning the risk of end-year volatility.

Into all of this will step the Fed on Wednesday, with the FOMC meeting expected to deliver a 25bps rate hike with a dovish twist. Other central bank meetings this week include the BoE and the BOJ, but the dovish tone was set by the ECB last week. Net asset purchases will end, but the ECB is in no rush to hike rates or reduce the balance sheet, all of which brought an end to the EUR’s brief rally above 1.14. Apart from raising rates, the Fed’s message will be delivered through some tweaks in forward guidance, a downshift in the dots, and in the tone of Chairman Powell's press conference. This may not be as dovish as the markets are expecting, however, with some recent thought even being given to whether the Fed will tighten at all. Strength in retail sales and upward revisions to Q4 GDP forecasts have put paid to these, and may also make the Fed’s message more balanced than many expect. This could in turn help to keep the USD underpinned, especially with other currencies continuing to languish.

Chief amongst these is GBP which unwound most of the gains it made in the wake of Theresa May winning the vote of confidence within her Conservative party. With her subsequent talks in Brussels failing to get any concessions over the infamous ‘backstop’ arrangement in Ireland, the signs are increasing that her Withdrawal Agreement from the EU will fail to get support in the UK parliament, with the vote having now been postponed until the middle of January. With political activity likely to die down in coming weeks, there will be little news to provide a more positive narrative, which should ensure that the downside for GBP remains favoured. Needless to say the BoE meeting this week will be a relative non-event, but any weakness in UK inflation data may also compound the pound’s soft position.

The BOJ meeting which concludes on Thursday will also be something of a non-event. GDP contracted in Q3, and inflation at 1.0% remains well below the BOJ’s 2.0% target. Along with these are worries over spillover effects from China’s slowing, and downside risks to global growth, all of which will keep the BOJ sidelined for another year at least. However, unless US-Japan rate differentials widen on the back of the Fed’s rate hike this week, it may be difficult for USDJPY to gain ground, with external risks another factor that could keep the JPY underpinned.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg