Recent Search

Popular Searches

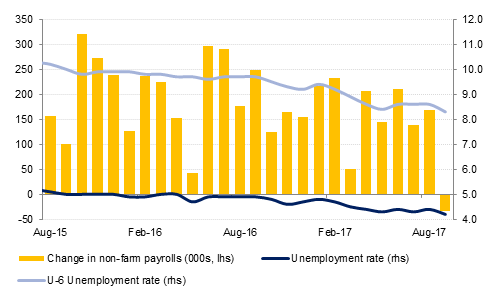

The US Labour Department said nonfarm payrolls in the US dropped by 33,000 last month. The decline was the first in almost seven years and driven largely by Hurricanes Harvey and Irma that have displaced workers temporarily unemployed and delayed hiring. However the headline figure masked a host of other positive labour market indicators, with unemployment falling down to a 16 1/2 year lows, and wage growth picking up by 0.5% m/m. lifting the annual growth rate to a nine month high of 2.9% y/y. The data came on the back of surprisingly strong manufacturing and non-manufacturing activity for the month, with the accumulated effect of the week’s news being to catapult expectations for a December rate hike to in excess of 90%, up from 70% previously.

Saudi Arabia and Russia have signed a number of landmark investment deals during King’s Salman visit to Russia. Saudi Aramco along with the Saudi Public Investment Fund and the Russian Direct Investment Fund, signed an MOU for investment in energy services and manufacturing. Aramco also signed deals with Gazprom in upstream gas development, a unit of a Swiss based marketing arm of Lukoil. Two other agreements Aramco signed were with Gazprom Neft for technology and R&D, and with the Russian Direct Investment Fund and SIBUR for the strategic marketing of petrochemicals. Other deals included a USD 100mn investment in Russian infrastructure by Saudi Arabia, and purchases of Russian defence hardware by the kingdom. The deals come as Saudi and Russia interests in oil markets converge in face of competition from non-traditional producers of shale oil.

Separately, the IMF released its latest Article IV report at the end of last week. While the Fund expects almost no growth this year, they anticipate an improvement in growth prospects over the medium term as progress is made with structural reform. Some Board members also noted that the authorities may have room to adjust the speed of reform implementation in order to make the transition easier.

Source: Emirates NBD Research

Source: Emirates NBD Research

UST yield curve continued to ascend during the week with yields on 2yr and 10yr closing up at 1.50% (+2bps) and 2.36% (+3bps) respectively as futures implied probability of a rate hike in December increased to 78% on the back of strongest YoY wage growth (2.9%) since 2010. However safe haven bid ensuing from news about North Korea planning another nuclear test helped contain the fall in sovereign bond prices in the developed world.

Regionally, GCC credit markets had mixed performance with mild softening in bond prices on the back of widening benchmark yield curve. CDS spreads on GCC sovereigns held ground well amid improvements in government budget deficits and deepening capital markets. However, cash bonds, particularly the high grade sovereign in the AA category and shorter dated bonds suffered from steepening UST curve. Barclays GCC bond index closed with yield higher by a bp to 3.40% even though credit spreads narrowed by 4bps to 130 bps during the week.

KSA curve was range-bound after S&P affirmed Saudi Arabia’s rating at A- citing expectations of government taking steps to consolidate public finances and maintaining liquid assets close to 100% of GDP over the next two years. KSA also benefited from IMF’s report which expects KSA reforms to boost its budget by $90 billion by 2020 from new taxes and planned cuts in subsidies. Yield on KSA 27s sukuk closed down by a bp to 3.36% compared to a 2bps widening in KSA 26s bond to 3.41% - reflecting support of sharia investors for sukuk securities.

Last week the Dollar Index gained 0.77% to close at 93.800, rising for a fourth consecutive week. Technical analysis of this move reveals several key considerations. Firstly, the break of the resistive trend line of the daily downtrend that had been in effect since April 2017 has been sustained (see chart). In addition, the index has now closed above the 200 week moving average (92.879) for a second consecutive week. These observations further support the case that USD may be in the process of trend reversal and may appreciate over the remainder of the year. Indeed, the last week saw the index trade as high as 94.267 on Friday before finding resistance and closing below the 23.6% one year Fibonacci retracement (94.034). Should the index achieve a daily close above this level, it would pave the way for further advances towards the 100 day moving average (94.545).

It was a mixed day of trading for regional equities with the Tadawul losing -0.9% and the DFM index adding +0.6%. Drake & Scull continued its positive run from last week after the company completed its capital restructuring. The stock ended with gains of +4.7%. Elsewhere, National Agriculture Development Co gained +3.8% after the company signed a MoU with Al Safi Danone Co. to examine the possibility of an acquisition. Almarai, which could be impacted by a possible merger, declined -2.0%.

Oil markets moved off headlines from an industry conference in Russia last week and ultimately closed the week lower. WTI futures fell 4.6% over the week and Brent closed 3.3% lower. Initial hopes from a statement by Vladimir Putin that Russia would endorse an extension of the current production cuts were dashed on Friday as Russian officials clarified that an extension was just one possible outcome. Saudi Arabia’s energy minister also said the country was ‘flexible’ about extending the cut. Absent a clear message with firm targets and dates the market has likely already priced in an extension of the status quo, hence why the price response last week may have disappointed OPEC figures.

The market structures continued to weaken at the end of the week with Brent’s 1-2 month backwardation at USD 0.26/b, less than half its level a week earlier. WTI’s contango steepened over the course of the week, ending at USD 0.36/b. the spread between WTI and Brent also widened to over USD 6/b as WTI outpaced Brent on the downside. US oil markets may get a positive boost from the impact of Hurricane Nate which has plowed through the Gulf of Mexico, hitting three quarters of regional production.

Click here to Download Full article