Recent Search

Popular Searches

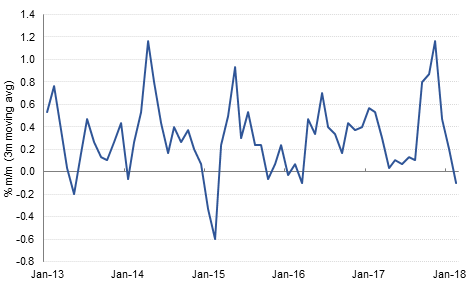

Economic data in Europe and the US were disappointing yesterday. In the Eurozone, industrial production fell by more than expected m/m in January, bringing the annual growth in IP down to 2.7% from 5.2% y/y in December and against expectations for a 4.4% y/y rise.

At a speech in Frankfurt yesterday, ECB President Mario Draghi said that not all of the recent strength in the euro was justified by economic fundamentals and that if the euro continued to strengthen, this could weigh on inflation in the future. Although the euro weakened after his comments, it has firmed again slightly overnight. Draghi also highlighted the risks to the economic outlook from US trade policy changes.

Meanwhile in the US, retail sales declined -0.1% m/m for the third consecutive month, although this was partly due to lower auto sales. Excluding autos, retail sales rose 0.2% m/m in February, still lower than had been forecast. Economist and TV commentator Larry Kudlow was appointed as White House economic advisor, replacing Gary Cohn who resigned last week.

Q4 2017 GDP growth data were released in New Zealand this morning, coming in lower than forecast at 0.6% q/q and 2.9% y/y. The calendar for today is relatively thin, with the Swiss Central Bank meeting the main event. However, there is a raft of economic data due to be released tomorrow, including Eurozone inflation, US housing starts and building permits as well as US industrial production and the JOLTS job openings survey.

US treasuries closed higher across the curve following a rather weak retail sales data and comments from Larry Kudlow, the new economic adviser to Donald Trump, on the USD and trade policies. Yields on the 2y UST, 5y UST and 10y UST closing at 2.25% (flat), 2.60% (-1 bps) and 2.81% (-3 bps).

Regional bonds continue to trade in a tight range with the YTW on the Bloomberg Barclays GCC Credit and High Yield index closing flat at 4.19% and credit spreads widening 1 bp to 161bps.

Dar Al Arkan raised USD 500mn in a 5-year sukuk which was priced to yield 7.125%.

NZD has declined against the other major currencies following softer than expected economic data. Reports from Statistics New Zealand showed that GDP disappointed expectations for 0.8% q/q and 3.1% y/y expansion in Q4 2017, instead showing growth of 0.6% q/q and 2.9% y/y respectively. As we go to print, NZDUSD is trading 0.05% lower at 0.73281. Support is likely to start at the 50 day moving average of 0.7292.

Elsewhere JPY is outperforming in the Asia session against the other major currencies as concerns over trade protectionism and softer than expected US retail data have triggered safe haven bids. This morning, USDJPY is trading 0.28% lower at 106.02 and looks likely to re-test the 2018 lows of 105.25.

Developed market equities closed lower following comments from the incoming economic adviser Larry Kudlow’s comments on trade policies and the USD. The S&P 500 index and the Euro Stoxx 600 index dropped -0.6% and -0.2% respectively.

Regional markets closed lower with the exception of the KWSE index (+0.3%). The Tadawul and the DFM index closed flat as investors locked in some gains from the recent rally. El Sewedy continues to see investor interest with gains of +9.6%. The stocks has the potential to be included in the MSCI index later this year.

Oil prices closed marginally higher with Brent and WTI adding +0.4% each. The prices were helped by data from EIA which showed that US gasoline demand hit record for this time of the year which helped inventories to drop. The total stockpile of crude and products including strategic reserve fell by 4.526mn barrel last week.