Recent Search

Popular Searches

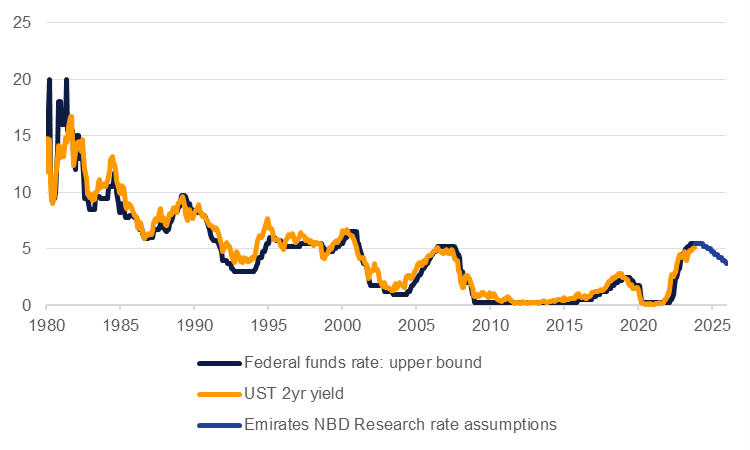

US inflation eased to 3.2% y/y in October, its lowest pace since Q1 2021 when the economy was still emerging out of the Covid-19 pandemic. From a peak of more than 9% in June 2022, inflation has trended steadily lower as goods prices have started to fall and services inflation is easing considerably. The downward pull in inflation will no doubt be welcomed by the Federal Reserve and we maintain that they have finished their rate hiking cycle and will turn to rate cuts by the end of H1 2024.

The October CPI print sparked a massive rally in US Treasury markets. Yields on the rate sensitive 2yr US Treasury dropped almost 20bps to 4.836%, their largest single day decline since markets were rocked by the collapse of several US lenders in March this year. If the Fed does indeed hold rates steady from here and begin to cut rates from mid-way through 2024 then it would follow that US Treasuries should rally given the strong link between the 2yr UST and the Fed funds rate.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

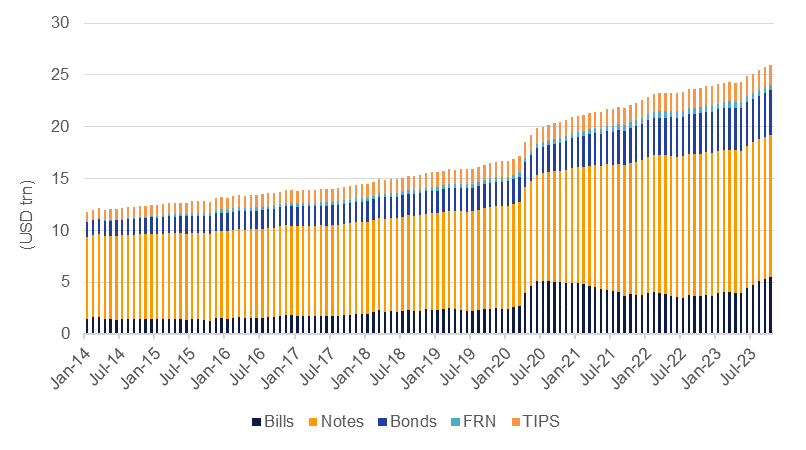

However, a stumbling block for any pending rally in USTs may be the scale of US public debt. Since the pandemic, the level of marketable public debt in the US has spiked as the government financed relief programmes and has now set out more considerable public spending via the Inflation Reduction Act. Total marketable debt has increased by over USD 9trn since the end of 2019, roughly the same amount as adding the nominal GDP of Germany, India and Saudi Arabia to the US debt stock.

The composition of the marketable debt stock has also shifted with shorter-tenor bills (less than 1 year) now accounting for about 21% of the total compared with historic levels of around 15%. Notes, the belly of the UST curve, account for more than half of the marketable debt while longer term bonds (20 and 30yr USTs) along with floating rate notes (FRNs) and TIPS make up the rest.

Source: Bloomberg, US Treasury, Emirates NBD Research.

Source: Bloomberg, US Treasury, Emirates NBD Research.

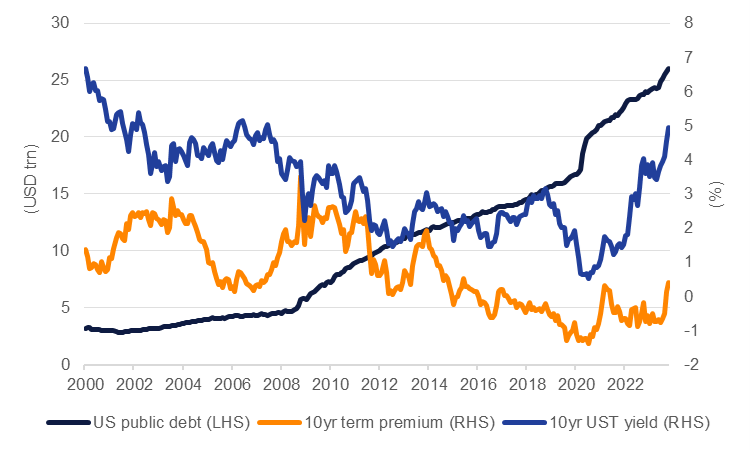

The scale of public debt the US now faces—estimated by the Office of Management and Budget in the White House at 124% of GDP for 2023—along with the cost of the debt may act as a drag on US Treasuries trending higher. The 10yr UST yield has risen more than 290bps since the start of 2022 when the Federal Reserve began its hiking cycle and the level of longer-dated expensive debt will grow even more in 2024 according to Treasury’s latest quarterly refunding statement.

Term premiums for US debt—the additional amount of yield beyond inflation and policy embedded in the yield of a Treasury—have increased in 2023 to about 0.4%. The outlook for inflation and rates still seem to be the dominant factors in the value of US Treasuries at the moment but market attention on the scale of public debt will probably mean that term premiums move steadily higher.

Source: Bloomberg, Emirates NBD Research.

Source: Bloomberg, Emirates NBD Research.

Edward Bell

Edward Bell