Recent Search

Popular Searches

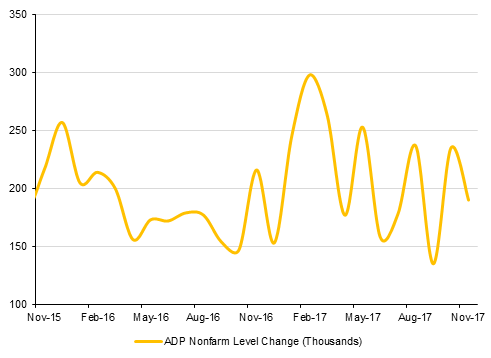

The private sector in the US gained 190k jobs in November, according to the latest ADP assessment. This was a slowdown from growth of 235k jobs in October but sets the market up for a strong non-farms payroll print out later this week. Manufacturing jobs rose by 40k, a strong indicator of sustainable jobs growth across sectors while the impact of hurricanes earlier in Q3 now looks to have been firmly worked out the data. However, unit labour costs measured by the Labor department fell by 0.2% in Q3, suggesting there is still some slack available in the US jobs market.

The Bank of Canada kept interest rates on hold but did caution that more rate hikes could be coming next year even as the outlook for the economy is uncertain. The BoC raised rates in July and September this year and overall the Canadian economy has been reporting decent data, with strong job growth in November moving the unemployment rate to 5.9%, its lowest level since February 2008.

India also held interest rates unchanged yesterday as the Reserve Bank of India holds to a neutral stance. Inflation has accelerated in recent months, hitting 3.6% in October while the economy is still grappling with the introduction of a nation-wide sales tax in July. So far the RBI has resisted pressure to lower rates to help provide support following the introduction of the tax. Inflation remains below the RBI’s target level of 4% but the gains in oil prices and other commodities in recent months may remove some of the rationale for keeping rates at low levels.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Uncertainty created by President Trump’s surprising recognition of Jerusalem as Israel’s capital fueled the safe haven bid that lifted treasuries higher. Yield on 2yr and 10yr USTs declined by a bp each to 1.81% and 2.34% respectively. Yields on 10yr Bund and Gilts also closed lower at 0.29% (-2bps) and 1.23% (-3bps) respectively while credit spreads widened marginally with CDS levels on US IG and Euro Main closing at 53bps (+0.5bp) and 49bps (+1bp) respectively.

Local bond market was subdued as oil prices dwindled a bit in the face of higher US oil inventory data. Credit spreads widened a bp to 132 bps for the Barclays GCC bond index even though average yield on the index was down to 3.53% (-1bp) as a result of benchmark yield narrowing.

In the primary market, Qatar International Islamic Bank is believed to have mandated banks for a USD sukuk to be raised in January next year. Al Ahli Bank of Kuwait is also in the queue for benchmark sized bond sale in early 2018.

CAD was yesterday’s underperformer following the rate decision by the Bank of Canada. While the central bank left interest rates unchanged at 1.00%, they signalled that they remained “cautious” about future rate hikes. Over the course of the day USDCAD rose 0.77% to close at 1.2789, having hit highs of 1.2807 during the US session. Currently trading at 1.2800, while we see daily closes above 1.2723, risks remain for further upside with a climb towards the 200 day moving average of 1.2957 being a realistic scenario.

AUD is posed for a second daily decline after softer than expected trade data. The nation’s trade surplus narrowed to AUD 105 mn in October compared to AUD 1604 mn in September. As we go to print AUDUSD trades 0.17% lower at 0.75506. As yesterday, we expect support to be found at 0.7529 (the 38.2% one year Fibonacci retracement). A break of this level exposes the cross to further declines towards the 23.6% one year Fibonacci retracement of 0.7388.

Profit taking ahead of the year end continued to depress equity bourses in the developed world. S&P 500 closed marginally down and Dow Jones lost -0.16% yesterday. Asia has opened mixed this morning with Nikkie trailing up by 1.24% and Hang Seng in the red at -0.04% in early morning trades.

Barring equities in the UAE, most GCC bourses continued their slide downward. Abu Dhabi exchange closed higher by 1.11% followed by Dubai at +0.02% mainly attributed to noticeable jump in Drake & Skull shares on the back of some technical bid.

Tadawul closed down by -0.16% and Qatar’s main stock benchmark fell 1.45% in Doha, after a Gulf summit ended without a breakthrough to end the feud between the country and its neighbors as most of the region’s heads of states were absent. In another news about Qatar, MSCI is to continue using the local FX rates and will not switch to the offshore FX rates for the Qatari riyal in the MSCI Indexes until further notice.

Oil prices fell sharply yesterday as the EIA reported increases in inventories of refined products (gasoline up 6.8m bbl) and a decline in crude inventories. The decline in crude stocks was expected considering a major export pipeline from Canada had been shut following an oil spill but the builds in products stocks does send a worrying message about demand conditions moving into the final months of the year.

Brent futures lost 2.6% and WTI gave up nearly 2.9% on the data. Forward curves for both benchmarks loosened on the news with WTI back into contango at the front of the curve and Brent’s 1-2 month spread narrowing to USD 0.2/b. Dec spreads for Brent appear to have hit a ceiling of around USD 2.75/b in backwardation on the back of OPEC’s extension and have been steadily waning since then.