Recent Search

Popular Searches

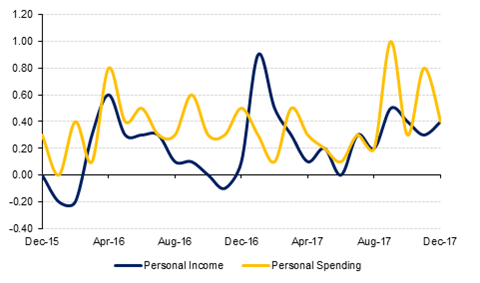

Yesterday’s US personal spending and income data were stronger than expected in December both rising by 0.4%, and with real personal income up by 0.3%. The data continues to highlight the strength of Q4 consumption, as demonstrated by the GDP report released at the end of last week which showed personal consumption rising by 3.8% over the quarter. However, the savings rate fell to 2.4%, its lowest rate since 2005, which might be a signal that consumption is unlikely to remain as firm going forward.

The next two days will see significant US events with Donald Trump’s first State of the Union address to be made tomorrow morning, followed by the outcome of the FOMC meeting later in the day. The markets will look to the Fed to provide signals about a March rate hike, while President Trump will likely emphasize the strong economy and his plans for infrastructure spending and immigration reform in his set piece speech. Comments on trade may also be

Eurozone GDP data will likely be the highlight of today’s session with another strong growth reading of 0.6% q/q expected in Q4. This may not induce much change in Eurozone markets for the time being, however, with the EUR showing some signs of fatigue after its broad gains last week. This was despite calls from ECB Governing Council member Klaus Knot for QE to end as soon as possible. The lack of positive reaction to his remarks demonstrates that the single currency may in fact be becoming technically overbought and even at risk of a correction as we highlighted in our FX Week publication at the start of the week. A more cautionary message was heard from ECB Chief Economist Peter Praet yesterday who suggested that the Eurozone was still ‘some distance’ away from sustained inflation, with Praet going on to say that the ECB still needs ‘patience and persistence in steering’ monetary policy. This is in line with our view that September may not be the end of QE bond buying and that Eurozone interest rates will not rise until well into 2019.

US Treasuries closed off the lows of the session but still lower following personal income and spending data. It appears investors are cautious ahead of the Federal Reserve meeting later this week. Yields on the 2y USTs, 5y USTs and 10y USTs closed at 2.11% (flat), 2.49% (+2 bps) and 2.69% (+4 bps).

Regional bond market continue to drift lower following rise in benchmark yields and plenty of supply in the primary market. The YTW on the Bloomberg Barclays GCC Credit and High Yield index rose 2 bps to 3.89% and credit spreads widened by 1 bp to 145 bps.

Emirate of Sharjah appointed banks for a 2b yuan 3y Panda bond issue. The bank is expected to price the same later this week.

NZD outperforms this morning after stronger than expected trade data. Compared with market expectations for a trade deficit of NZD 125mn, reports from Statistics New Zealand showed a trade surplus of NZD 604mn in December, a reversal of the NZD 1233mn deficit posted in November. As we go to print, NZDUSD trades 0.19% higher at 0.73367. We expect initial resistance to further gains at the 76.4% one year Fibonacci retracement of 0.7375.

Despite an increase in the unemployment rate from 2.7% in November to 2.8% in December and a reduction in household spending from 1.7% y/y to -0.1% y/y for the same period, JPY is trading firmer in the Asia session. The JPY has found support after better than expected retail sales data which has showing that sales accelerated to 3.6% y/y growth in December from 2.1% the previous month, beating market expectations for 2.2% growth. As we go to print, USDJPY trades 0.16% lower at 108.78. We expect initial support at 108, the baseline that has held since September 2012.

Developed market equities closed lower as rising yields weighed on dividend stocks. Weak earnings from Apple also weighed on investor sentiment. The S&P 500 index and the Euro Stoxx 600 index lost -0.7% and -0.2% respectively.

Regional markets continue to see dividend plays. While the Tadawul added +0.4%, the DFM index dropped -0.3%. FAB reported strong set of earnings after the market closed with a dividend payout of AED 0.70 per share. Bank Muscat announced a cash dividend of OMR 0.03 per share and 1 bonus share for every 20 held.

Oil prices started the week on a weak note amid a rebound in the USD and speculation that US crude inventories may expand for the first time in 11 weeks. Brent prices dropped -1.5% to USD 69.46/bbl and WTI lost -0.9% to USD 65.56/bbl.