Recent Search

Popular Searches

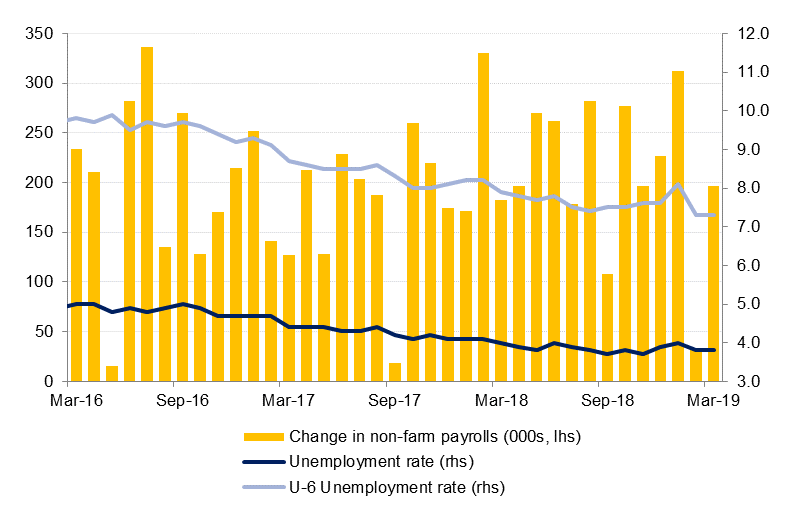

US jobs data was better than expected on Friday, with non-farm payrolls rising 196k in March against forecasts for a 177k rise. The February payrolls was revised up to 33k from 20k in the initial estimate. However, it was not all good news: labour force participation declined last month and manufacturing jobs fell -6k, the first drop in manufacturing employment since mid-2017. The gains in jobs were largely in education, health services, professional & business services and construction. There was also very little wage growth evident in the March data, with average hourly earnings up just 0.1% m/m (3.2% y/y) against the consensus forecast of 0.3% m/m (3.4% y/y). The 10y US treasury yield declined slightly, while US equities responded positively to the non-farm payrolls data.

The US-China trade talks are progressing, although a final deal is unlikely to be ready for several more weeks. Both President Trump and VP Xi were upbeat following their meeting on Friday. While no further formal talks are scheduled at this time, the two sides will remain in “continuous contact” to resolve outstanding issues, according to a White House statement.

Brexit uncertainty continues this week after talks between the Conservative government and the opposition Labour Party failed to reach agreement on a way forward. PM May has formally requested another extention to the end of June, but is hopeful that MPs will agree on a deal well before then so that the UK can avoid participating in European parliamentary elections on 23 May. The PM will address other EU leaders on Wednesday at the emergency summit.

Besides Brexit, the key events this week will be the release of the minutes from the Fed’s March meeting, and the ECB meeting on Wednesday. German industrial production data, released on Friday, was not as weak as had been feared, but nevertheless points to further deterioration in the manufacturing sector, even as services growth in the Eurozone holds up well.

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Fixed Income

Treasuries ended the week lower as economic data turned mixed. The non-farm payrolls data showed that 196,000 new jobs were added in March with unemployment rate at 3.8%. However, weak average hourly earnings diluted the impact. Overall, 2y UST, 5y UST and 10y UST yields ended the week at 2.33% (+7 bps w-o-w), 2.30% (+7 bps w-o-w) and 2.49% (+9 bps w-o-w) respectively.

Regional bonds continued their positive run. The YTW on Bloomberg Barclays GCC Credit and High Yield index dropped -4 bps w-o-w to 4.03% while credit spreads tightened 12 bps w-o-w to 163 bps.

The primary market continues to remain active. RAK Bank raised USD 500 mn through a 5-year paper which was priced 185bps over mid swaps. First Abu Dhabi Bank raised USD 1.1bn through a floating paper which has a coupon of 95bps over quarterly US LIBOR.

FX

A minor loss of 0.02% means that for a third week, EURUSD finished lower, closing at 1.1216. Most importantly, the price has closed below the 200-week moving average (1.1341) for a fifth week, which is bearish for the price, especially when combined with the fact it is trading below the 50-month moving average (1.1313).Should the price fall below the 2019 low of 1.1177 in the week ahead, it could trigger a more substantial decline towards the 1.10 handle last seen in May 2017.

A 0.77% rise took USDJPY to 111.71 in a second week of gains. This movement in price is technically significant for a number of reasons. Firstly, the price has broken back above the formerly resistive 200-day moving average (111.49) which now appears to be acting as a support level. However, more importantly, analysis of the weekly candle chart shows that the 100-week moving average (110.81) has been breached for a second week, and now appears to be providing support. While the price remains above the 50-week moving average (111.12), we expect a retest of the 112 handle, not far from the 200-week moving average (112.09). A break of this level may result in further gains towards the 50% five-year Fibonacci retracement (112.44).

GBPUSD was mostly unchanged last week, gaining 0.03% to close at 1.3039, following two previous weeks of declines. Of note is that for a second week, the price has closed below the 50-week moving average (1.3057) which leads us to believe that further declines towards the 200-day moving average (1.2974) which has acted as a support level since February 19th 2019.

Equities

It was largely a positive day of trading for regional equities. The DFM index added +0.2% and the KWSE PM index gained +1.4%. The earnings season in the region got off to a neutral start. Almarai reported Q1 2019 sales of SAR 3.35bn and net profit of SAR 336mn. The company attributed the y/y decline in profit to general weakness in fresh dairy and juice market. The stock ended the day marginally lower.

Commodities

Oil markets closed at 2019 highs to end the week as a healthy US jobs report and improving data from Germany helped to allay demand concerns. Brent closed the week at USD 70.34/b, up 2.8%, while WTI gained nearly 5% over the week to close at USD 63.08/b. In the US oil and gas explorers added 15 rigs last week after six consecutive weeks of decline. Meanwhile speculative positioning in futures and options rose last week as investors are counting on a further tightening of crude markets.

Aditya Pugalia

Aditya Pugalia