Recent Search

Popular Searches

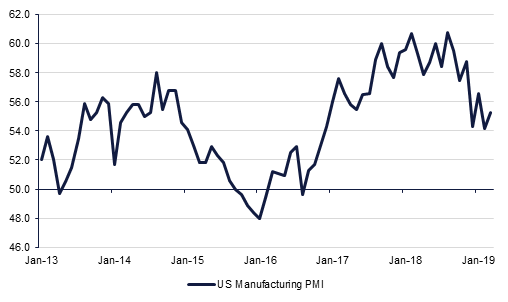

Following China’s better than expected PMI activity data over the weekend the US ISM manufacturing activity index was also firmer overnight rising to 55.3 in March, up from 54.2 in February. The data should help to allay some fears of an imminent recession in the US, which we felt was overdone, and should contribute further to the better tone in global markets at the start of the quarteer.

The Eurozone’s manufacturing PMI, however, continued to be weak in March, posting the second negative reading of the year so far. The index registered just 47.5, significantly weaker than the 49.3 recorded in February, and missing already-weak expectations of 47.6. Germany saw its manufacturing PMI fall to its lowest reading since 2012 at just 44.1, as concerns over trade wars and Brexit uncertainty weighed on sentiment already negatively affected by a troubled autos sector.

Meanwhile despite Brexit the UK March manufacturing PMI rose to 55.1, a 13-month high and a strong rebound from February's 52.1 reading. The surprisingly strong rise in activity reflected manufacturers efforts to build up inventories ahead of Brexit, which ultimately will have to be worked through and may curb activity in the future. On ther subject of Brexit there was another series of indicative votes in the UK parliament yesterday but none of them was able to establish a common position, leaving the clock ticking with just 11 days to go before the next deadline for the UK to leave the EU.

Deposits at UAE banks grew 0.8% m/m and 9.1% y/y in February, the fastest annual deposit growth in four years. The main driver was a 0.6% m/m (45.8% y/y) rise in government deposits, although private sector deposits also grew 1.7% m/m and 2.7% y/y. Gross credit grew 0.6% m/m and 4.7% y/y. However, private sector credit growth slowed to 3.5% y/y, while loans to government and GREs increased on an annual basis. Banks’ holdings of CDs rose 5.1% m/m and 14.2% y/y in February.

Source: Emirates NBD Research, Bloomberg

Source: Emirates NBD Research, Bloomberg

Treasuries closed sharply lower amid continued risk appetite. Better than expected manufacturing data from China and factory orders from the US and UK helped investor sentiment. Yields on the 2y UST, 5y UST and 10y UST closed at 2.33%, 2.32% and 2.50% in what was the largest single day moves since the start of the year.

Regional bonds were largely unchanged. The YTW on Bloomberg Barclays GCC Credit and High Yield index remained at 4.07% while credit spreads hovered around 168 bps.

The focus in regional markets was on the Aramco numbers after the company launched its bonds offering to fund its acquisition of PIF’s stake in Sabic. The company made USD 111.1bn in net profit last year as it produced about 10% of the world’s crude.

Sterling slipped again overnight following more votes in the UK parliament that failed to resolve the Brexit issue. The weakness of the JPY was the main feature yesterday as risk appetite improved on the back of positive PMI data in China and overnight in the U.S. Meanwhile the RBA left interest rates unchanged at 1.50% this morning with the Central Bank saying that it will continue to set policy for sustainable growth, with the AUD little affected by the news.

Of note is the EURUSD cross which is currently trading at 1.1202, following eight days of consecutive declines. Should support fail to be found at the 2019 low of 1.1177, further declines towards the 1.10 level cannot be ruled out.

Notwithstanding mixed economic data from the US, equities made a positive start to the second quarter. Investor sentiment was helped by better than expected data from China. The S&P 500 index and the Euro Stoxx 50 index added +1.2% and +1.0% respectively.

Regional equities were more mixed. The DFM index outperformed its regional peers with gains of +2.4%. Market heavyweights Emaar Properties and Emirates NBD led the rally with gains of +4.0% and +4.5% respectively. Elsewhere, El Sewedy Electric rose +4.1% after one of its consortium won a USD 550mn contract in Sharjah.

Brent crude closed up 0.9% to USD 69.01/b overnight, continuing the strong rally seen over the first quarter, the strongest Q1 performance in years. OPEC production curbs continue to be implemented, as Saudi Arabia cut production to a four-year low of 9.82mn b/d in March, contributing to an overall reduction of 295,000 b/d by OPEC members.