Recent Search

Popular Searches

.jpg?la=en&h=600&w=800&hash=C0F5CEE5D0E3E10A8570451CAC8EBFD4)

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

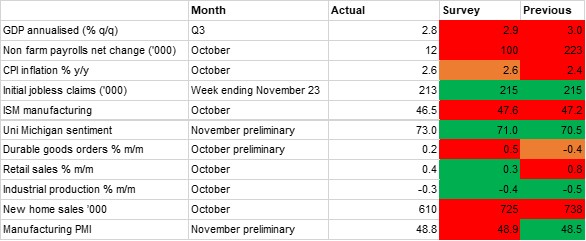

Our monthly scorecard for October is fairly evenly balanced between red and green indicators, a result which chimes with the Fed’s preference for further interest rate cuts, but at a gradual pace, as laid out at the minutes from the November FOMC meeting published at the end of November. While some of our tracked indicators signalled a deterioration over the past month, or came in under expectations, or both, in some cases the signal was clouded by the effects of hurricanes and strikes. With this in mind, we do not expect any further front-loading of rates by the Fed and hold to our expectation that cuts will come in 25bps increments, with the next due in December.

Although GDP growth did slow to 2.8% q/q annualised in Q3, down from 3.0% in Q2 and just under the predicted 2.9%, this is still a robust growth print when considering the restrictive monetary policy that has been in place. Personal consumption has been powering the expansion, and this was up 3.5% q/q (down modestly from 3.7% on the initial print). The fourth quarter has started on the front foot with the University of Michigan consumer sentiment index up for the fourth month straight in November and retail sales up 0.4% m/m in October, beating the predicted 0.3%. The gain when stripping out automobiles was a more modest 0.1%, but it should be noted that eight out of the 13 categories reported growth, with electronics and appliances registering the greatest rise. This is a positive momentum signal heading into the holiday season.

Preparations for the busy holiday period have apparently been supportive of the labour market in recent weeks, with the weekly initial jobless claims figure at 213,000 on the latest reading for the week ended November 23, below the predicted 215,000. There is some volatility around the date of Thanksgiving, however, while the monthly nonfarm payroll report for October was also clouded, in this case by adverse weather conditions. The net gain in jobs was just 12,000, but this was heavily affected by the two hurricanes that hit the southeast over the month, and by strikes in the manufacturing sector. Looking through the noise it is apparent that the labour market is slowing: continuing claims are at their highest level since late 2021 and job losses are anticipated in the manufacturing and autos sectors through the close of the year. As the FOMC minutes noted, though, there has been ‘no sign of rapid deterioration in labor market conditions…’, and nothing that would prompt a reacceleration in rate cutting.

On the other side of the dual mandate, disinflation has stalled, and headline CPI inflation ticked up to 2.6% y/y in October, from 2.4% the previous month. This was in line with expectations, with higher housing costs driving the increase as core goods price growth slowed. The PCE price index, the Fed’s preferred inflation gauge, was up 2.3% y/y in October, from 2.1% a month earlier.

Aside from the impact on the labour market, there were other indicators which were affected by the two hurricanes that hit the country, especially in the housing sector. New home sales fell to 610,000 in October, down from 738,000 the previous month. Residential investment was down 5.0% q/q in the Q3 GDP print, and the indication is that it will remain a drag in the final quarter. Production indicators were also impacted by the weather, with the ISM manufacturing index at 46.5 in October, the seventh straight month of sub-50 contraction. Uncertainty ahead of the November election also weighed on the index.

Daniel Richards

Daniel Richards