Recent Search

Popular Searches

.jpg?la=en&h=600&w=800&hash=C0F5CEE5D0E3E10A8570451CAC8EBFD4)

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

The past month has been a stronger one for US data releases compared with the previous set of figures, and while there is evidence of a slowdown in some areas, in general the economy continues to display the same level of resilience to the higher rates environment that it displayed last year. Indeed, consensus estimates have real GDP growth this year at 2.3%, down marginally on 2023’s 2.5%, while the Federal Reserve maintained its forecast at 2.1% at its recent revision of its summary of economic projections.

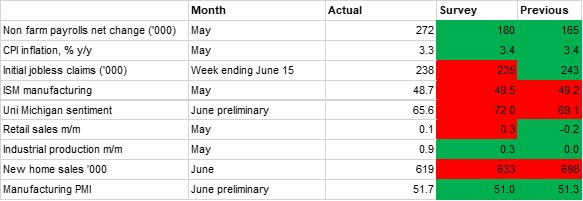

The Fed also left its unemployment forecast unchanged at 4.0%, and the labour market data of the past month has continued to outperform. Nonfarm payrolls figures for May saw a net gain of 272,000, up from 165,000 the previous month and much higher than the expected 180,000, with gains led by the private sector. Crucially, average hourly earnings accelerated to 0.4% m/m, up from 0.2% the previous month, and while headline CPI inflation did slow modestly to 3.3% y/y in May, down from 3.4% in April, the Fed nevertheless adjusted its price growth expectations upwards at its June meeting. The PCE inflation forecast for 2024 was nudged up from 2.4% to 2.6%, likely contributing to the change in the dot plot to a prediction of just one rate cut this year from three previously. We retain our forecast of two rate cuts this year, but recognize that the risk is skewed towards less easing, if inflation doesn’t continue to slow (see Central banks make their differences clear in June).

On the production front, data continues to be mixed, and while the prints have been coming in stronger this year than last, manufacturing generally has continued to underperform. The ISM manufacturing survey fell to 48.7 in May, down from 49.2 the previous month and undershooting predictions that it would rise to 49.5. March this year was the only month that the reading has been in positive territory since late-2022. The S&P Global manufacturing PMI remains stronger, however, and it printed better than the previous month and expectations, while there was a 0.9% m/m surge in industrial production as hotter weather boosted utilities output.

The demand side still has a somewhat mixed outlook also. The University of Michigan sentiment index unexpectedly fell to a seven-month low in June, well below the previous month and predictions, with both current conditions and expectations deteriorating. Concerns around high prices were cited by both lower- and middle-income households. This is contributing to weak retail demand also, with sales up just 0.1% m/m in May after April’s 0.2% contraction. Notably, online sales contributed meaningfully to the little growth there was, suggesting rising discernment amongst shoppers as spending power is crimped.

Daniel Richards

Daniel Richards