Recent Search

Popular Searches

Source: Bloomberg, Emirates NBD Research

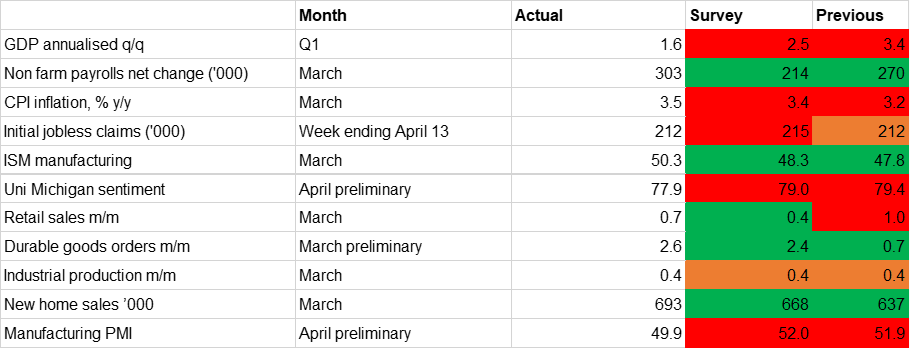

Source: Bloomberg, Emirates NBD ResearchUS GDP came in at 1.6% annualised q/q in Q1, down from 3.4% the previous month and well short of the predicted 2.5% expansion. The slowdown was due in large part to imports, which weighed the most on growth since 2022, while personal consumption grew at 2.5%, down from 3.3% previously and lower than the predicted 3.0%. Personal spending was largely on services, especially health care and financial services. If inventories, government spending, and trade are stripped out, then inflation-adjusted sales to domestic purchases expanded at a healthy 3.1%. Of interest to the Fed, the core PCE price index rose 3.7%, from 2.0% previously and higher than the predicted 3.4%, which reaffirms our recent adjustment to our rates forecast that the FOMC is unlikely to cut rates until September at the earliest. Services-sector inflation was even higher at 5.1%, and markets will now be watching for the PCE inflation data due later today.

The GDP figures to an extent confirm the timelier data of the past month featured in our scorecard. These have shown that while the pace of growth this year is unlikely to exceed that of 2024 – the consensus forecast is for real GDP growth of 2.4%, compared with the 2.5% realised last year – this is still not an economy that looks in need of support from the Fed even with this Q1 headline miss. While the FOMC’s growth forecast is still more bearish than consensus at 2.1%, this was revised up in March from 1.4% previously.

Some monthly indicators are showing signs that the ongoing tight monetary policy stance is weighing on activity. Durable goods orders were up 2.6% m/m in March, but this was driven by a sharp rise in new orders at Boeing. Stripping out the volatile transportation component of the measure, growth was just 0.2% – in line with expectations but still evidence of some reticence by businesses to invest with interest rates elevated and some political uncertainty related to the upcoming elections later this year. New home sales picked up to a six-month high of 693,000 in March, from 637,000 the previous month, but this remained below the five-year average (719,250) and was supported by incentives from housebuilders. Existing home sales declined to 4.2mn, from 4.4mn in February, with high mortgage rates discouraging sellers from moving away from their existing low-rate deals.

However, on the output side, the data was broadly positive. Industrial production expanded 0.4% m/m in March, in line with the previous month and predictions, and the ISM manufacturing survey turned expansionary at 50.3, the first reading above the neutral line since September 2022. The S&P Global manufacturing PMI fell back into contractionary territory, but only just at 49.9. Demand also held up, as retail sales grew 0.7% in March, down from 1.0% in February but still higher than the predicted 0.4% growth.

The labour market continues to outperform expectations, with a net gain of 303,000 jobs on the NFP report for March, compared with the predicted 214,000 and up from the previous month’s 270,000. Indeed, the headline U-3 unemployment rate declined in March, to 3.8% from 3.9% previously even as the participation rate rose to 62.7% from 62.5%. In its summary of economic projections released at the March meeting, the FOMC revised down its unemployment projections for December modestly, from 4.1% to 4.0%. The job creation in March was relatively broad based, with healthcare, government, leisure and hospitality, and construction driving the gains.

On the wage inflation front, average hourly earnings in March were up 4.1% y/y, down from 4.3% y/y in February but the 0.3% m/m marked an acceleration from February’s 0.2%. Other inflation data has also come in hotter than the Fed might have liked it to, with headline CPI back up at 3.5% y/y in March, up from 3.2% in February and the highest rate since September last year. Core inflation and super-core inflation also came in hotter than predicted. The prices paid component of the ISM manufacturing survey showed a sharp rise in March, which could be passed on to consumers in the coming months. These inflation and labour market points, coupled with hawkish messaging from Fed officials in recent weeks (and the FOMC made a modest upward revision to its core PCE inflation forecast in March to 2.6% at year-end from 2.4% previously), led us to revise our outlook for rate cuts this year, with our prediction now for two cuts in 2024 (from three previously) and not starting until September (previously June).

Daniel Richards

Daniel Richards