Recent Search

Popular Searches

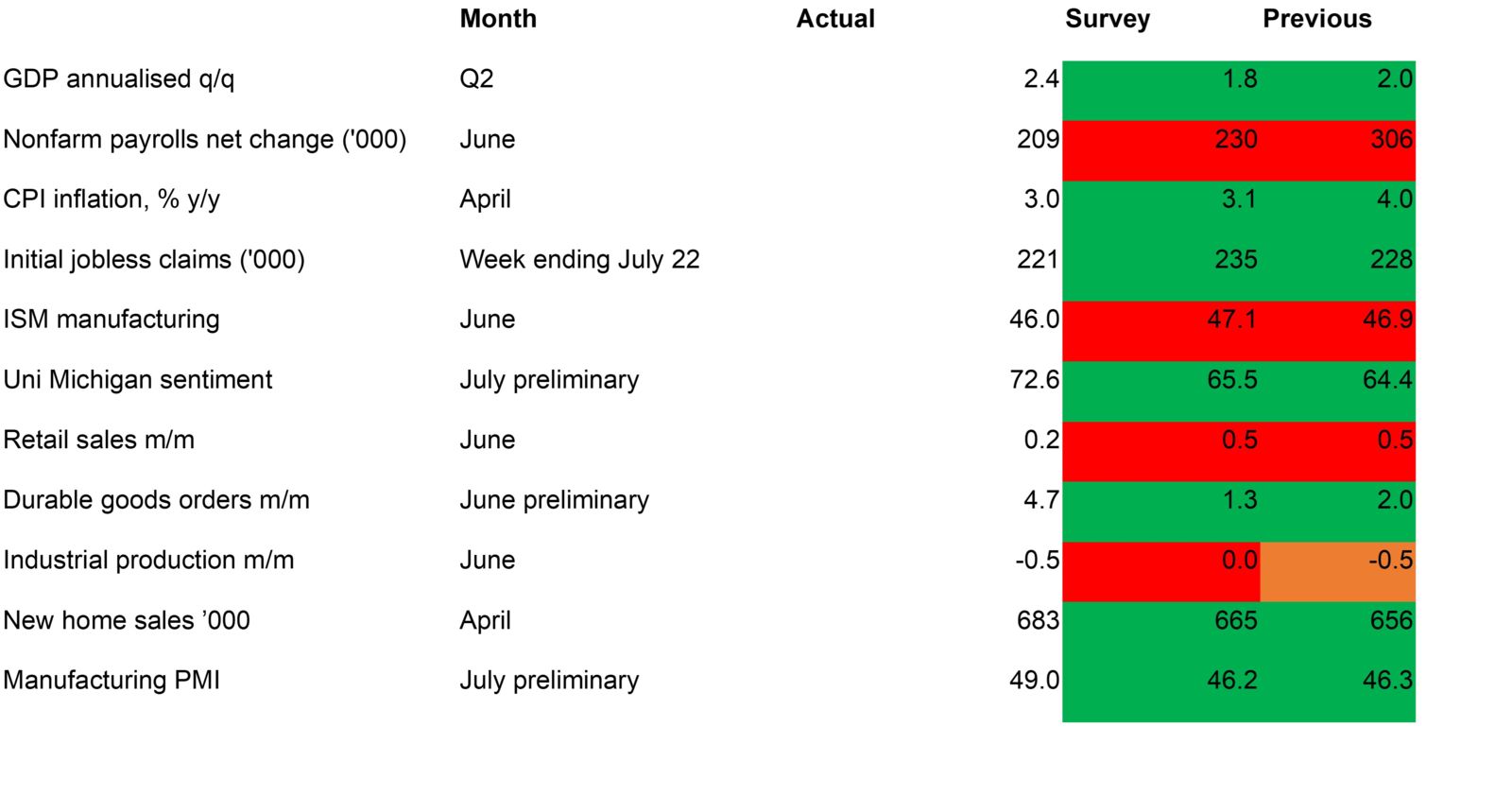

Macroeconomic data releases for the US over the past month have for the most part come in stronger than both expectations and compared with the previous month, as illustrated on our scorecard above where there is more green than red. Key among these releases was the GDP print for the second quarter, which came in strong at 2.4% q/q annualised, compared with expectations of a 1.8% expansion. The data came out the day after the FOMC’s July 26 meeting, where Fed chair Jerome Powell said that the central bank was no longer anticipating a recession in 2023, and the generally strong data has raised the prospect that the Federal Reserve will be able to engineer a soft landing this year, despite an aggressive 11 hikes to the Fed Funds rate since this tightening cycle began.

The robust economic growth could make the Fed’s task of clamping down on inflation more difficult. Jerome Powell warned in his post-decision press conference that while the fact that disinflation had been achieved without crashing the labour market was a ‘good thing’, ‘stronger growth could lead over time to higher inflation.’ Nevertheless, most recent price indicators have been moving in the right direction, with headline CPI inflation falling to 3.0% y/y in June, marking the slowest pace of annual price growth since March 2021.

Much of the disinflation was driven by lower energy prices compared with the spike seen in the middle of last year, and core inflation remained significantly higher at 4.8%. All the same, this was lower than the predicted 5.0% and was the slowest since last October. The Fed’s preferred gauge of inflation, the PCE deflator, also slowed to 3.0% in June, from 3.8% in May, while core PCE fell to 4.1%, from 4.6% a month earlier. We hold to our view that the Fed’s hiking cycle has now been completed barring a major upside surprise in inflation over the next two prints before the September meeting, although we do not expect any cuts to rates to start until the end of Q1 2024 at the earliest. We are also cognizant of upside inflation risks in the second half of this year, with energy prices expected to rebound sharply by year-end.

On the other side of the Fed’s dual mandate, the net gain in nonfarm payrolls slowed to 209,000 in June, markedly below the downwardly revised 306,000 the previous month, and lower than the predicted 230,000. This marks one of the few patches of red on this month’s scorecard, but the result is arguably a win for the Fed as it indicates that the remarkable resilience of the jobs market so far this year could be starting to wane, which should alleviate upwards wage pressure from tight labour conditions. This was still somewhat noticeable in the June data as average hourly earnings rose 0.4% m/m, the same pace as in May after an upwards revision from 0.3%. Initial jobless claims have also remained relatively low to date, dipping compared to the previous week in the week ending July 22. The NFP report for July is due at the close of this week, where a further slowdown to 200,000 net gain is predicted.

Breaking down the US GDP figures, consumer spending rose 1.6% q/q, higher than the predicted 1.2% but down from the 4.2% surge recorded in Q1. The US consumer has provided the backbone of the upside growth surprise so far this year, with households continuing to spend despite high inflation and rising interest rates. The services PMI has continued to outperform, and retail sales have largely held up, although the pace of growth in June slowed to 0.2% m/m, missing the predicted 0.5% which would have matched the previous month. On a quarterly annualised basis control group sales rose just 2.1% in Q2, down from 5.1% in Q1, potentially signaling the start of a deceleration in spending by US consumers. Nevertheless, the University of Michigan sentiment index came in at 72.6 in July, well above June’s 64.4 reading.

As has been the trend through the year so far, the manufacturing data has been somewhat weaker than consumption. Industrial production contracted 0.5% m/m in June, and while the manufacturing PMI did pick up in July, at 49.0 it remained below the neutral 50.0 level. Encouragingly, however, businesses continue to invest, as evidenced by the GDP data and durable goods orders. Non-residential fixed investment expanded 7.1% q/q annualised in Q2 and this business strength appears to have continued through the end of the quarter, with durable goods data for June showing a m/m expansion of 4.7%, the fastest pace in nearly three years. Stripping out transportation and defence, the core measure registered a slower pace of 0.2% growth, however, suggesting that investment (the figures are not inflation-adjusted) is slowing.

Daniel Richards

Daniel Richards