Recent Search

Popular Searches

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

All eyes will be watching Fed Chair Jerome Powell’s speech at the annual Jackson Hole Symposium on August 25 for any indication he might give as to US monetary policy going forward. The expectation is that he will stick to the script of the FOMC being data-dependent and market expectations and our view is that the higher-for-longer narrative remains firmly in play. Powell and other Fed officials will have been parsing the latest data releases from the US and indeed, there is little in the way of the most followed indicators in our macro scorecard that suggest that the economy is under undue strain and in need of a corrective movement, or on the other hand that further hikes are required.

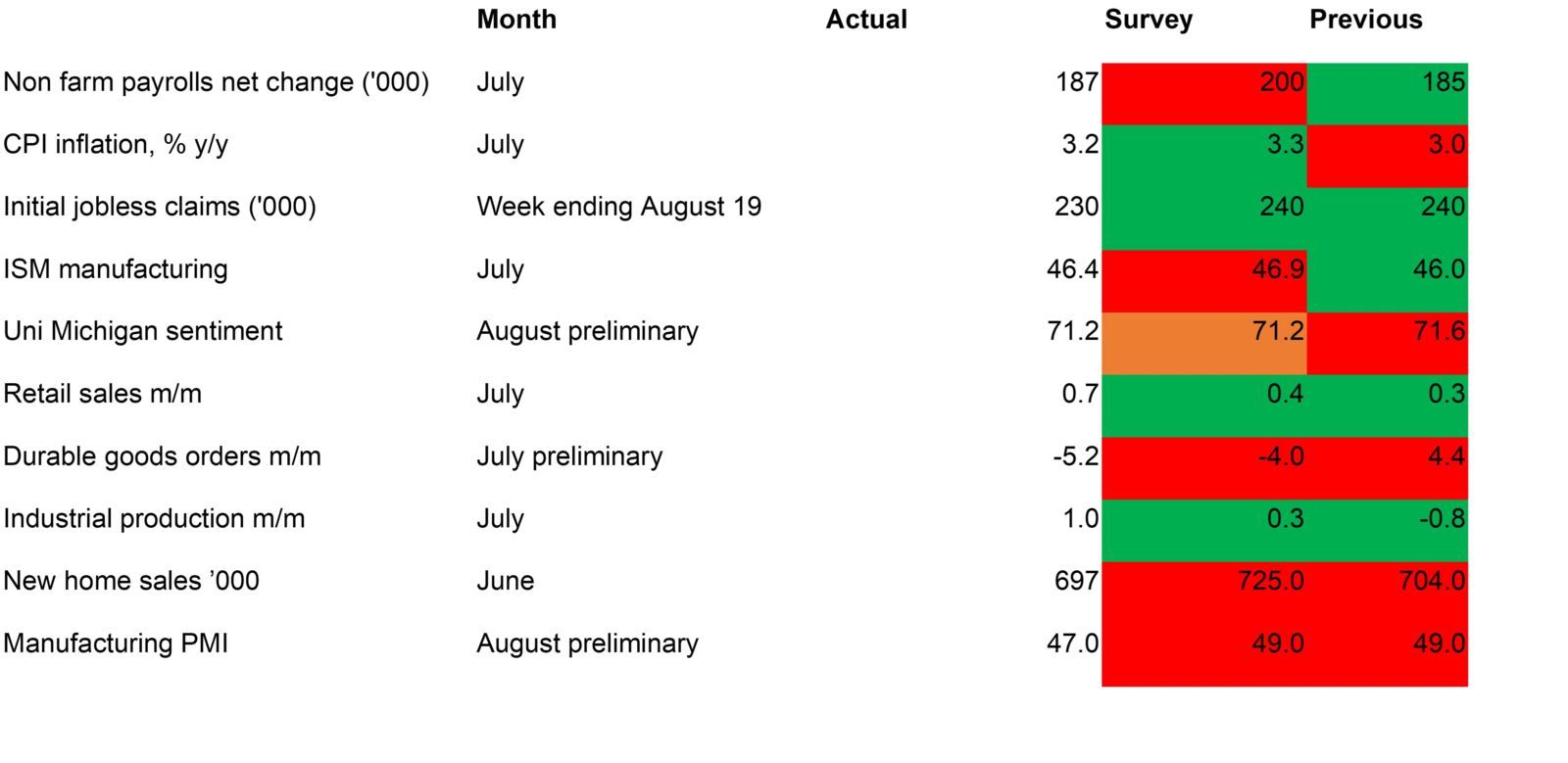

On the inflation front, annual CPI inflation rose in July, picking up to 3.2% y/y from 3.0% previously. This was still lower than the projected 3.3% however, and core inflation continued to moderate as it came in at 4.7%, from 4.8% in June. Looking at price growth on a monthly basis, the 0.2% was the same pace as in June, which if annualised would be not far off the Fed’s 2.0% target. The move on the PCE deflator, the Fed’s preferred inflation target, was even more favourable as it fell to 3.0% y/y, from 3.8% a month earlier, with core PCE dropping to 4.1%, from 4.6% previously. There is one more inflation print due before the September Fed meeting, but barring a sizeable upside surprise a hold on rates is anticipated.

On the other side of the Fed’s dual mandate, the NFP report for July also came out well for the Fed as the net gain in jobs was just 187,000, lower than the predicted 200,000. With the June figure revised down to 185,000, these were the lowest numbers reported since the drop of 268,000 in December 2020 when the US saw a surge in Covid-19 cases. The data suggests that the remarkably resilient labour market of the past two years is starting to slow which should ease upwards pressure on wages – wage growth was still fairly high in July as average hourly earnings increased by 0.4% m/m, and 4.4% y/y.

Other data was somewhat mixed, but a key takeaway is that manufacturing surveys remain weak, with both the S&P Global (47.0) and the ISM (46.5) surveys coming in well below the neutral 50.0 level. Both surveys missed expectations for the month, but there was some positive data on industrial production which registered a 1.0% gain. Durable goods orders slipped sharply as they dropped 5.2% m/m but this was a product of an outsized aircraft order in June – stripping out transport orders, orders registered a 0.5% gain. On the consumption side, retail sales improved in July as they expanded 0.7% m/m, but sentiment remained weak and a drop in new home sales suggests that the series of aggressive rate hikes by the Fed is starting to bite.

Daniel Richards

Daniel Richards