Recent Search

Popular Searches

Source: Bloomberg, Emirates NBD Research

Source: Bloomberg, Emirates NBD Research

Our macroeconomic scorecard for the US is somewhat more evenly spread between green and red than it was the previous month, seeming to confirm that the economy is indeed starting to slow down a little this year after its remarkable resilience in 2023. Growth last year was 2.5%, far in excess of the predictions set at the start of the year, while for 2024 the expansion is forecast at 2.0%, with risks arguably to the downside. That being said, there is still nothing in the data suggesting that a recession is imminent, nor anything that would prompt the FOMC to rapidly cut rates in order to support the labour market . Our view remains that the Fed’s first rate cut will not come until June, with a total of three 25bps cuts projected over 2024 as a whole, and the market-implied projections have moved closer to our view in recent weeks.

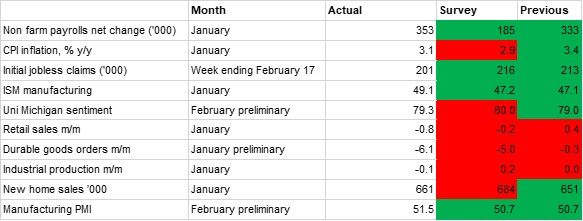

This has largely been prompted by two data points in particular released over the past month, namely the significant upside surprise on the NFP report for January, and the hotter-than-anticipated inflation print for the same month. The net gain in jobs according to the NFP report was 353,000, far in excess of the predicted 185,000, and while there may be some seasonality issues around reporting, the December figure also saw a sizeable upwards revision to 333,000, from the initial estimate of 216,000. The gains were fairly broad based across sectors. Further, average hourly earnings also rose sharply in January, rising 0.6% m/m and 4.5% y/y, which would likely give the Fed pause about cutting rates too soon.

On the inflation front, headline CPI growth did slow to 3.1% y/y in January, from 3.4% in December, but this was still above the median forecast of 2.9%.. On a monthly basis, prices were up 0.3%, compared with a predicted 0.2%. Moreover, core inflation also came in higher than anticipated at 3.9% y/y (predicted 3.7%) and at 0.4% m/m was at the strongest level in eight months. Services and shelter both continued to post strong growth, which will prolong concerns about inflation entrenching.

Looking at the demand side of the economy, there was a general underperformance in the US economic indicators over the past month. Retail sales declined -0.8% m/m, the largest fall in a year, and far weaker than the predicted -0.2% contraction. Even stripping out automotives and gasoline the fall was -0.5%, compared with predicted 0.2% growth. The fall in demand was broad based, with nine of the 13 separate categories seeing a decline in sales, suggesting that the US consumer’s resilience, which has underpinned growth over the past 12 months, may be starting to wane. The University of Michigan consumer sentiment index did tick up in January but was lower than predictions, while February’s Conference Board survey fell unexpectedly. Concerns around inflation are easing, but those around the economy, the labour market, and the political environment have risen.

Business demand is also coming in softer than had been anticipated as firms are seemingly becoming more cautious around boosting capital expenditure in a slower growth environment, especially while interest rates remain high. Durable goods orders declined -6.1% m/m in January, even weaker than the predicted -5.0% fall, and while much of this was down to lower aerospace orders, excluding transport the fall was still -0.3%, missing a projected 0.2% rise.

Daniel Richards

Daniel Richards